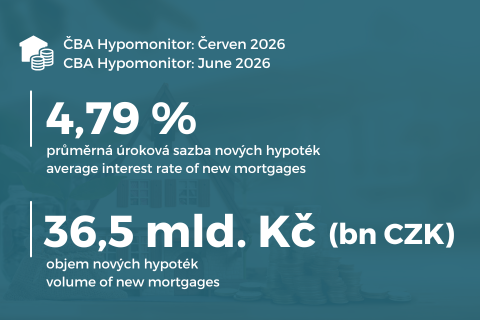

CBA Hypomonitor: Higher Rates and Regulations Slowed Mortgage Growth, but the Market Remained Strong in June

Prague, July 17, 2026 – Following a very strong spring, the mortgage market slowed significantly for the first time in June due to stricter regulations and higher market interest rates. Banks and building societies issued 36.5 billion crowns in new mortgages (excluding refinancing), a 4% decrease from the previous month. The June figures thus represent a correction rather than a weak month. Since the beginning of the year, the volume of new mortgages has reached 216 billion crowns, which is 66 billion more than last year. The average interest rate on new mortgages continued to rise to 4.79% from 4.67% in May, as the earlier, more pronounced increase in market interest rates was partially reflected in mortgage rates. The rise in rates was more pronounced for new purchase mortgages, while it was more moderate for refinancing.

The slowdown in June reflected the end of the previous rush to secure mortgages, during which some prospective borrowers had accelerated their decisions due to the expected impact of higher market rates and the CNB’s April tightening of conditions for so-called investment mortgages. The weaker momentum was also reflected in the average mortgage amount falling back below 4.7 million crowns, which reduced the illustrative monthly payment on a new average mortgage back below 26,000 crowns.

However, the overall picture of the market remains unchanged: both the volume and number of new mortgages remain near the strong levels seen in the second half of last year. The June data therefore tend to confirm a cooling-off period following exceptionally strong months rather than the onset of a weaker market phase. The CNB’s next meeting to set macroprudential mortgage policy will take place on September 10, and the current figures should keep the central bank in a wait-and-see mode. Mortgage regulations remained unchanged in June, but the Bank Board raised the countercyclical capital buffer by 0.25 percentage points to 1.5%, effective July 2027. For more details, see “CNB Tightens Banks’ Capital Buffer: Responding to Faster Loan Growth and New Risks.”

Table 1: Summary of Mortgage Volume and Average Interest Rates for June 2026

| monthly figures |

| ytd data | ||||

Volume | Number | Rate |

| Volume | Number | Rate | |

Total | 48,9 | 10 940 | 4,75 |

| 294,1 | 65 374 | 4,54 |

New loans | 36,5 | 7 793 | 4,79 |

| 215,9 | 45 520 | 4,56 |

of which: |

|

|

|

|

|

|

|

for the purchase | 25,9 | 5 559 | 4,81 |

| 155,4 | 32 840 | 4,56 |

for reconstruction | 6,5 | 1 389 | 4,70 |

| 35,7 | 7 577 | 4,51 |

other | 4,1 | 845 | 4,87 |

| 24,8 | 5 103 | 4,64 |

Refinanced from another institution | 10,6 | 2 722 | 4,61 |

| 66,2 | 16 927 | 4,46 |

Refinanced internally, increased | 1,7 | 425 | 4,74 |

| 12,0 | 2 927 | 4,51 |

Source: CBA Hypomonitor. Note: Seasonally unadjusted data

Jaromír Šindel, chief economist of the Czech Banking Association:“Stricter central bank regulations, rising mortgage rates due to higher market interest rates, and increasingly expensive real estate led to a slowdown in the June mortgage market, including a decline in the average mortgage amount. This followed very strong activity in previous months. Nevertheless, the mortgage market remained at the strong levels we observed in the second half of last year.”

Note: The outlook through the end of the year is based on current conditions—it is derived from the current trend, not from a model-based forecast. However, for the remainder of the year, it anticipates a 7% correction in the number of mortgages compared to the level seen in the second half of 2025.

Mortgage activity cooled off in June, but volumes and numbers remained strong compared to the second half of last year

Overall, banks and building societies reported new unconsolidated business in June in the form of new and refinanced mortgages totaling CZK 48.9 billion, which is 7% less than a month ago. Year-over-year, transactions were up 32%. Their total volume so far this year has reached CZK 294 billion, representing a 59% increase compared to the first half of last year.

In June, banks and building societies actually provided new mortgage loans (excluding refinancing) totaling CZK 36.5 billion. Compared to May, new mortgage activity declined by approximately 4% in volume, which is a weaker result than the usual 7% increase seen in June. This represents a correction following the strong months earlier this year, driven by the CNB’s stricter criteria and higher market interest rates. After seasonal adjustment, June’s new mortgage figures showed a 17% decline to CZK 29.4 billion compared to May’s CZK 35.4 billion. At the same time, it is below the average volume of the previous three months (CZK 37.3 billion), but remains close to the levels seen in the second half of last year. On a year-over-year basis, the growth in the volume of mortgages originated in June slowed further to 25% after an average year-over-year increase of 41% last year.

Martin Vašek, CEO and Chairman of the Board of Directors of ČSOB Hypoteční banka and ČSOB Stavební spořitelna:“People’s interest in homeownership is enormous, and the housing finance market remains strong. Real estate prices are at an all-time high, though in recent months we have seen a slight slowdown in the rate of price increases for apartments and houses. Mortgage interest rates continue to be significantly influenced by the geopolitical situation in the Middle East. To increase housing affordability, we are therefore developing additional possible solutions to the current situation, including support for and financing of cooperative housing.”

The number of new mortgages in June fell by 1% month-over-month to 7,793, though this is still 12% higher than a year ago. We estimate that, after seasonal adjustment, the number in June was around 6,414, approximately 17% below the average (7,765) for the previous three months. Since the beginning of the year, the number of new mortgages has reached 45,500 (+24% year-over-year). The growth trend in new mortgages over the last three months—that is, from April through June—implies that the total for this year will reach around 89,000. This would be below the average of around 92,000 recorded from 2016 to 2018, but still well below the 114,000 from 2021. However, following the CNB’s tightening of conditions in April, lower numbers of new mortgages can be expected. Assuming a 7% decline in the number of new mortgages compared to the second half of last year, this would bring the total for this year to around 82,000, which would be nearly 8% higher than last year.

Chart No. 2: Newly Granted Mortgages Excluding Refinancing

June brought a correction in selected metrics of new mortgage lending activity …

Source: Czech Banking Association, CNB, CZSO, Flat Zone

Chart 3: Average Mortgage Amount by Purpose

… thanks in part to the average mortgage amount falling back below March’s levels.

Source: CNB, CBA Hypomonitor

The volume of refinanced and increased loans (whether internally or from another institution) fell to 12.4 billion CZK in June. However, this is 75% more than the average of CZK 7.1 billion refinanced last year and three times more than the refinanced volumes in 2024. The share of refinanced loans in the total volume of mortgages granted then fell to 25.4%, but remains significantly above last year’s average of 21%. It is thus above the 17.2% share recorded in 2022–2023, though still below the nearly 29% share from 2020–2021, when households refinanced at a mortgage rate of 2.14%.

In June 2026, households refinanced at an interest rate of 4.63%, which is 0.12 percentage points higher than the 4.51% rate a year ago. However, the mortgage rate for refinancing in June was nearly two-tenths of a percentage point below the interest rate for truly new mortgages. Higher refinancing volumes reflect the convergence of expiring longer-term fixed-rate periods from the era of low interest rates and shorter-term fixed-rate periods from the recent period of higher interest rates. For more on the rising wave of mortgage rate resets, see CBA Focus: The wave of mortgage refinancing is gaining momentum, but the interest rate shock is subsiding. Higher inflation remains a risk.

Marek Richter, Head of Mortgages at Air Bank:“June is traditionally one of the stronger months in terms of the volume of new mortgages granted, and historically, May is usually followed by a month-over-month increase. This year, however, the volume of new mortgages fell by approximately 4% compared to May. This trend is primarily due to a cooling of demand for mortgages during the spring months, which was a reaction to rising interest rates. Banks passed on a significant portion of the increase in funding rates to their lending rates, which was subsequently reflected in the overall results of the mortgage market.”

The average mortgage rate rose to 4.79% in June, reflecting the previous sharp increase in market interest rates

The average interest rate on new mortgages rose further in June to 4.79% from 4.67% in May. The June rate is thus 0.23 percentage points higher than the 4.56% rate a year ago, which increases the illustrative average monthly payment on a new mortgage by 600 Kč, or approximately 0.6% of the applicant’s net income. By comparison, the average mortgage rate in 2025 reached 4.58%, compared to 5.07% in 2024.

At 4.79%, the June mortgage interest rate was 0.57 percentage points above average market swap rates. This is still just under half a percentage point below the long-term average since 2014 (1.04 p.p.), while in the previous three months this spread relative to market interest rates stood at 0.37 p.p. In our study , we highlighted structural factors—primarily the strength of demand in a competitive market—that influence how market interest rates affect mortgage rates.

Among the domestic factors that primarily influenced the development of interest rate swaps was persistently high core inflation, which in June prompted the Czech National Bank to raise its policy rate to 3.75%. This move, and especially the easing of tensions around the Strait of Hormuz, led to a partial correction of the previous rise in market interest rates. However, this trend reversed again in July due to the resumption of fighting in the Persian Gulf. For more on these factors, see the analyses in CBA Monitor: The CNB raised its interest rate to 3.75% and is likely to hold it there until the fall, The GDP revision showed improved productivity, but high savings and rising real estate prices persist, June sentiment indicated mild optimism regarding growth, but raised concerns about inflation and the labor market.

Czech longer-term market interest rates[1], which have a key impact on mortgage rates—where three-year fixed-rate loans predominate—remained at higher levels in July. Czech five-year interest rate swaps fell by 0.13 percentage points to 4.26% in June and closed the month at even lower levels after May’s 4.4%. However, the resumption of fighting in the Persian Gulf kept their July levels above April’s 4.2%. Over the past twelve months, Czech five-year swaps have fluctuated between monthly averages of 3.6% (in February 2026) and 4.39% (in May 2026). Compared with the average level of five-year swaps in 2025, June rates were 0.61 percentage points higher. U.S. five-year interest rate swaps rose to 4.2% in June from 4.13% in May and were 0.34 percentage points above their 2025 average. Euro-denominated five-year swaps fell to 2.83% in June from 2.9% in May, but remained half a percentage point above last year’s average of 2.34%.

[1]These are primarily long-term interest rate swaps (IRS), which reflect the cost of money over longer maturities—in recent years, typically around 3 to 5 years— but the entire 2- to 10-year curve remains relevant, even though 10-year maturities are less relevant due to higher central bank rates compared to the previous decade, as well as due to the costs incurred when prepaying mortgages.

Chart 4: Average Mortgage Interest Rate – New Loans

Mortgage interest rates in June continued to reflect the previous sharp rise in market rates

Source: CNB, CBA Hypomonitor

Chart 5: Renewed U.S. attacks on Iran are keeping market swap rates higher

… which in July returned once again to the higher levels seen in mid-2024

Source: LSEG, Macrobond (July 15, 2026), CBA

The average monthly new mortgage payment fell back below 26,000 CZK, and the median payment fell below 21,000

The combination of rising interest rates and higher average mortgage amounts in June 2026, compared with the average values from 2025, increased the average monthly payment on newly issued mortgages by 3,100 Kč. Table 2 illustrates scenarios for the development of monthly payments for various mortgage terms. The table suggests that a rise in mortgage rates of more than 0.2 percentage points from their average level of 4.58% in 2025 resulted, for an average mortgage size with a typical repayment term of approximately 26.9 years, an increase in the monthly payment of just under 600 CZK to approximately 25,800 CZK—that is, 0.6% of the applicant’s net income—compared to the average payment in the previous year.

However, the current average mortgage amount was 11% higher than its average amount in 2024, which contributes to an increase in the monthly payment of 2,600 Kč compared to last year’s average monthly payment—based on last year’s average mortgage amount but at the current interest rate.

Conversely, compared to the average 2.33% mortgage interest rate for new mortgages in 2021, the current mortgage rate for refinancing of 4.63% —when the loan term is shortened—increases the monthly payments on an average mortgage by more than 3,100 CZK, or about 6.1% of the current gross average wage. However, this wage has increased by 33% compared to the end of 2021. We discussed the impacts and circumstances in Fokus CBA: The wave of mortgage rate resets is gaining momentum, but the interest rate shock is subsiding. Higher inflation remains a risk.

Table 2: Illustration of Monthly Payments for Average and Median Mortgages Based on Loan Term and Interest Rate

Source: CBA (the table with values is available in an XLS file attached to this report)

The average size of newly issued mortgages fell back below 4.7 million CZK in June

The average size of newly issued mortgages actually fell to 4.68 million CZK in June, a decrease of nearly 3% month-over-month. This amount was 11% higher than the CZK 4.21 million recorded a year ago, though this represents a slowdown following April’s 20% year-over-year increase. The higher average mortgage size at the beginning of this year likely reflects the lingering effect of pre-stockpiling in so-called investment mortgages, where, starting in April, the CNB tightened the requirements (LTV to 70% and DTI to 7x). Another contributing factor is the gradual growth in real household wages (8.1% year-over-year in Q1-2026; see graph here).

Mortgage amounts are also linked to real estate price trends, which only slowed slightly in the first quarter to 10% year-over-year. Asking prices in the first quarter of 2025 accelerated slightly to 2.7% quarter-over-quarter, which still exceeds their long-term average increase of 1.8%, while actual apartment prices slowed to approximately 2.5% quarter-over-quarter in the first quarter, with significantly different growth rates between Prague and the rest of the country. According to data from Flat Zone, the average transaction price of apartments—both new and older—in the Czech Republic reached 98,000 CZK/m² in the first quarter of this year (see charts on CBA Monitor) following a 4.7% year-over-year increase.

Chart 6: Illustrative comparison of monthly payments for the current average newly issued mortgage versus the same period a year ago, depending on the interest rate, mortgage amount, and loan term in years

Year-over-year, the rise in mortgage rates led to a CZK 630 increase in the average monthly payment, while the rise in the average mortgage amount caused an increase of CZK 2,600. However, this increase was more moderate than in May, thus more than offsetting the impact of the higher interest rate.

Source: CBA.

Note: Amounts are rounded to the nearest ten crowns.

Statistical Appendix

Chart 7: Seasonality of New Mortgage Loans

Source: CBA Hypomonitor

Note: These are truly new mortgages (i.e., excluding refinancing and loan increases). The underlying data are available in an XLS file attached to the CBA Hypomonitor website. The outlook through the end of the year (fcst) is based on current conditions—it is derived from the current trend, not from a model-based forecast. However, for the remainder of the year, it anticipates a 7% adjustment in the number of mortgages relative to H2-2025.

Chart 8: Breakdown of New Mortgage Loans by Purpose

Source: CBA Hypomonitor

Note: The latest figure represents the average for the past 12 months. The interpretation of the “other” segment may be distorted by the inclusion of so-called “mortgages without real estate” arranged without a specific purpose. For more details, see the methodological note below.

The mortgage market in 2025 saw strong growth in volume—up 41%—and an increase of nearly a quarter in the number of loans

Throughout 2025, banks and building societies provided new mortgage loans totaling 321 billion CZK. This is 93 billion CZK more than the 228 billion CZK issued in 2024. This year-over-year jump corresponds to a 41% increase. In addition, mortgages totaling 85 billion CZK were refinanced, bringing the total mortgage market to 406 billion CZK in 2025, up from 275 billion in 2024. If we adjust the volumes for the rise in apartment prices of around 15–16% (according to various statistics), the volume of new mortgages increased by slightly less in real terms. This also corresponds to a more moderate increase in the number of new mortgages in 2025—by just under a quarter to more than 76,110—and a nearly 15% increase in the average amount of new mortgages granted to 4.21 million CZK.

New mortgages in 2025 were financed at an average interest rate of 4.58%, which was half a percentage point lower than in 2024, while the spread relative to the market swap yield curve reached just under one percentage point, which is slightly below the long-term average. The average monthly mortgage payment in 2025 reached just under 22,800 CZK, which is 8.6% more than in 2024, and likely slightly exceeded last year’s increase of more than 7% the average nominal wage. The average year-over-year increase in the monthly mortgage payment of approximately 1,800 korunas in 2025 primarily reflected a higher average mortgage amount, with an increase in the payment of nearly 2,900 korunas, while the lower mortgage interest rate reduced the average monthly payment by more than 1,200 CZK.

Chart 1: Annual Volume, Number, and Average Amount of Mortgages Granted from 2020 to 2025

ource: CBA Hypomonitor

The Czech Banking Association Publishes Aggregate Statistics for the Entire Banking Market

The Czech Banking Association, in cooperation with its member banks, publishes new summary statistics on the housing market. These primarily cover the volumes and numbers of newly issued and refinanced mortgages, as well as the corresponding interest rates. The CBA publishes these statistics in aggregated form for the entire banking sector on a regular basis, typically around the middle of each month. All domestic banks and building societies providing mortgages in the Czech Republic participate in the survey. The data is available starting in January 2020 in the attached file at www.cbaonline.cz, where the relevant statistics can also be found separately for banks and building societies. The figures listed above apply to the sector as a whole and can also be viewed in a simple graphical format on the website cbamonitor.cz.

CBA Hypomonitor Methodology

The CBA Hypomonitor classifies mortgage loans provided by banks and building societies to households into several categories to distinguish new loans from refinanced loans or internal rate adjustments. New loans are then reported in categories based on the purpose of the loan:

1. New Loans

These are loans whose entire amount enters the economy for the first time. Loan consolidation or refinancing does not fall into this category. They are divided into three categories:

Real estate purchase

Real estate construction —including real estate renovation

Other new agreements— only new loans that are in no way related to the purchase or construction of real estate (which does not apply in the case of so-called “mortgages without real estate” arranged without a specific purpose), i.e., for example, so-called “American mortgages,” settlement of joint marital property, reimbursement of the purchase price, settlement of an inheritance share, settlement of a cooperative share, etc.

2. Refinanced loans from another financial institution

These are loans created by refinancing one or more loans from a financial institution other than the reporting one. Regardless of the amount refinanced and regardless of the amount of any increase, the total amount of the newly created loan is reported in this category.

3. Increased or internally refinanced loans

These are loans that were already part of the reporting entity’s portfolio in the previous reporting period and for which one of the following changes occurred during the reporting period:

an increase in the agreed amount

changes occurred such that the original loan was refinanced or converted into a new loan within the reporting entity. This constitutes a truly new contract, not, for example, merely a new agreement as part of the refixing of an existing contract. Therefore, the volume of such loans in the CBA statistics is lower than that of “other new agreements” in the Czech National Bank’s statistics.

Data for the CBA Hypomonitor are provided by the following banks and building societies: Air Bank, Česká spořitelna, ČSOB, ČSOB Stavební spořitelna, Fio banka, ČSOB Hypoteční banka, Komerční banka, mBank, Modrá pyramida, MONETA Bank, Oberbank, Partners Banka, Raiffeisen stavební spořitelna, Raiffeisenbank, and UniCredit Bank.