The average nominal wage in the first quarter of 2026 accelerated its year-over-year growth rate to 8.1% from 6.7% in the previous quarter. It thus rose to 51.6 thousand CZK from 48.4 thousand a year ago. After seasonal adjustment, the average nominal wage reached 51 thousand CZK in the first quarter, and I estimate that it was 51.7 thousand CZK in the business sector and 49.6 thousand in the public sector. As consumer price inflation slowed to 1.6%, real wage growth in the first quarter accelerated to 6.4% year-over-year from 4.4% in the fourth quarter. The average wage in the first quarter of 2026, in prices from the same quarter of the previous year, was 49,400 CZK. Real wage growth in the first quarter of 2026 was thus above its long-term average growth rate of 2.8% for the years 1998–2019 and is above the average growth rate of 4.3% from the pre-pandemic period of 2015–2019. In 2015, the nominal average wage was 26,6 thousand CZK, and in 2019 it reached 34,6 thousand.

Wage Trends

CBA Monitor

You can hide a data set by clicking on the data set name in the chart legend.

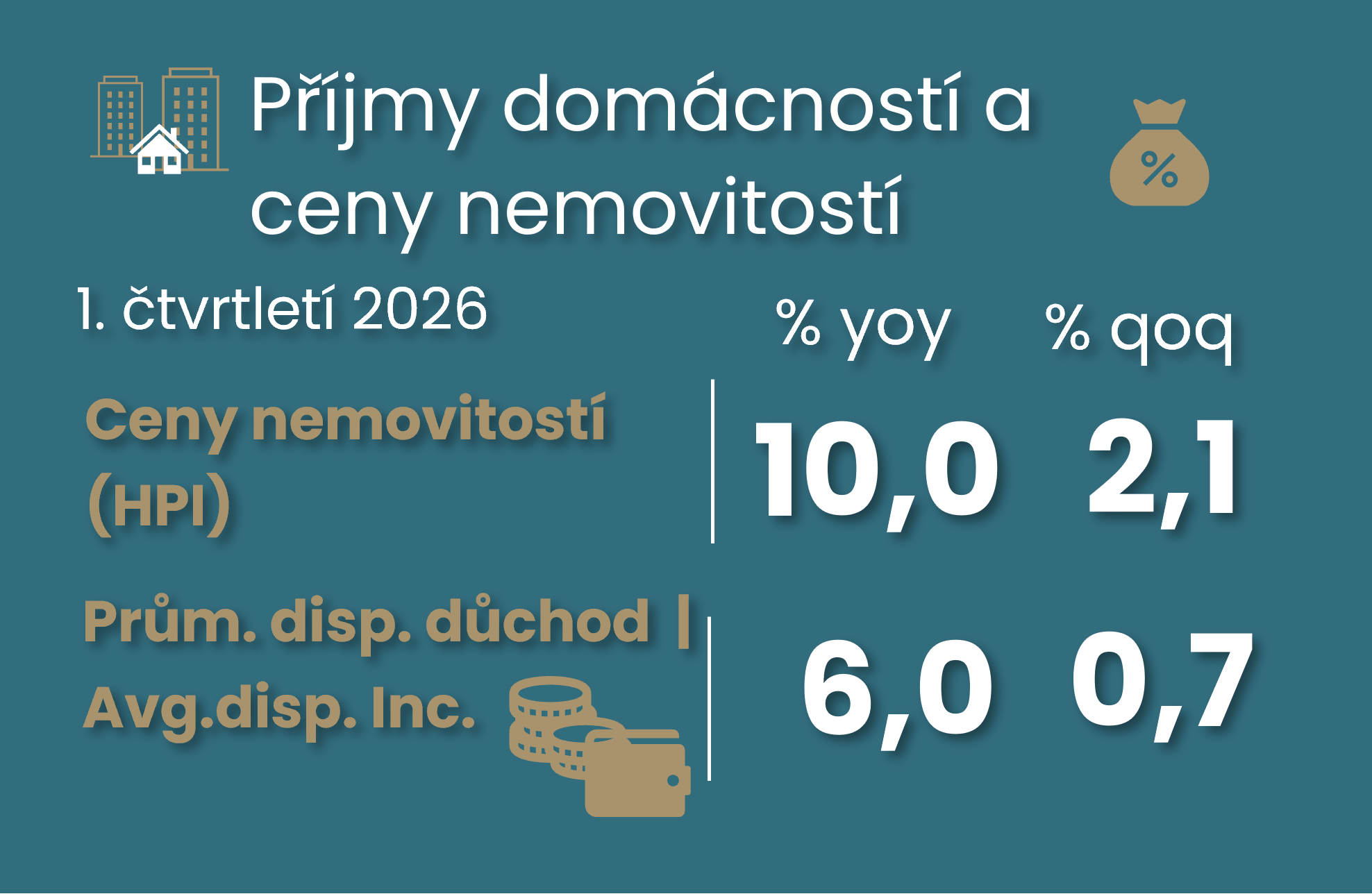

The Czech household savings rate remained at 20% in the first quarter of this year, still high even by international standards. Household disposable income slowed to 0.7% quarter on quarter, while property prices continued to rise by roughly 2%. The GDP revision showed weaker household consumption, but also a less negative productivity story thanks to stronger value added in industry. However, despite somewhat more moderate growth in the past, unit labour costs remain on a strong upward trend, which, together with high core inflation growth, is unlikely to bring a dovish turn at the CNB. That said, my interpretation of the new data from the Czech Statistical Office, especially for the first quarter, is significantly affected by the alignment of quarterly figures with the new annual data for 2025. The next quarterly release may therefore bring yet another story about the economy in the first quarter.

Jaromír Šindel

04. 06. 2026

Consumer price inflation slowed to 2.1% in May, surprising at a more moderate pace than the market had expected. However, some of the factors now dampening inflation may not be permanent. This is particularly true for food prices, which may be affected by rising global commodity prices in the months ahead. At the same time, strong wage growth of 8.1% year-on-year is divorced from labour productivity, creating pressures for higher core inflation. It is the contradiction between low headline inflation and persistent domestic inflationary pressures that poses a non-trivial economic and political dilemma for the CNB.

Jaromír Šindel

31. 03. 2026

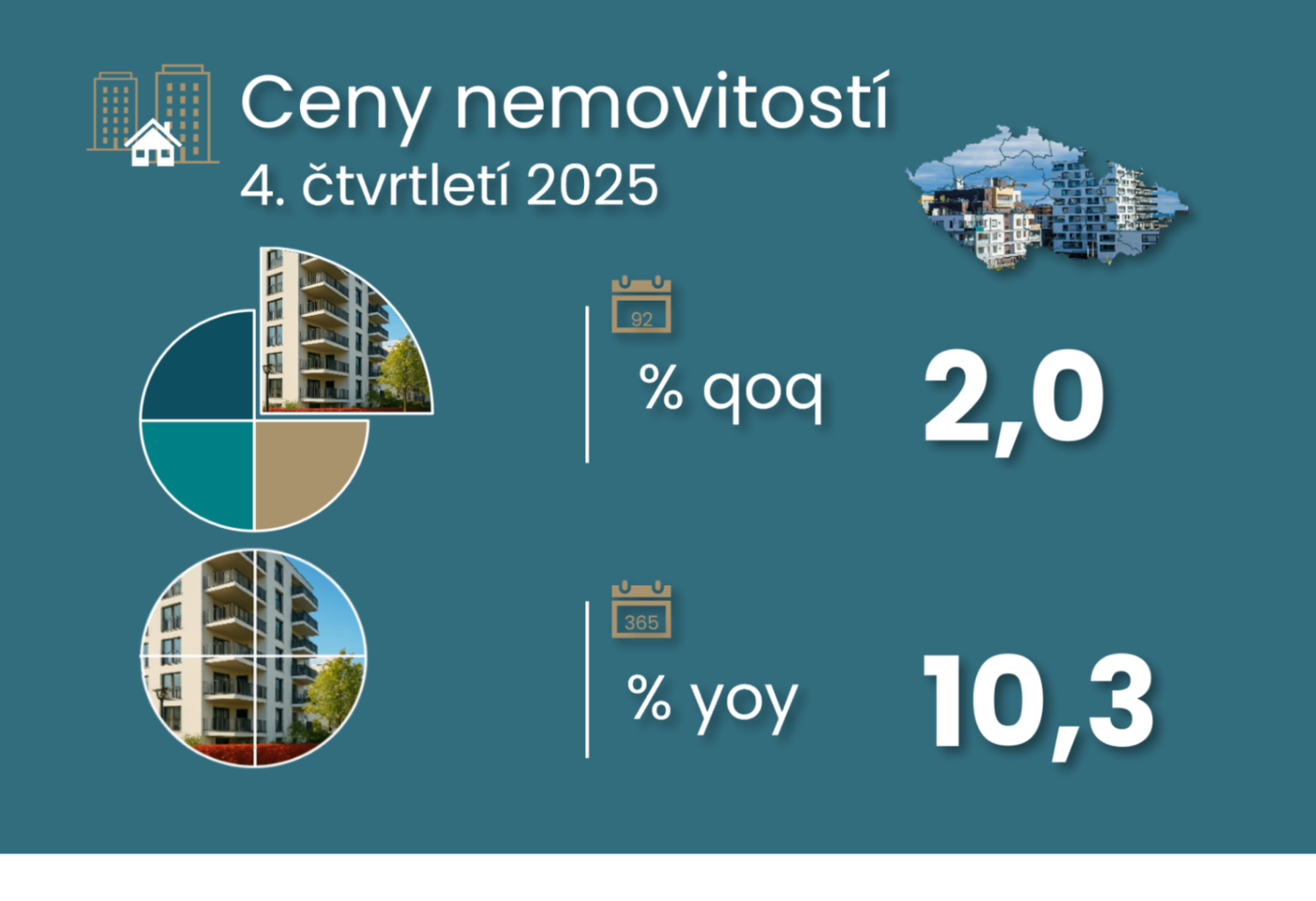

According to the CSO statistics, property prices, which include land and family houses, rose by 2% quarter-on-quarter in the final quarter of 2025. This slowed from the previous average 2.6% increase in the previous four quarters. Although the income side of demand is still lagging, real household incomes accelerated more sharply at 1.4% q-o-q (up nearly 3% in nominal terms) at the end of last year. And so did the household savings rate, which rose to 19.7%. Moreover, both figures were positively revised and there was a slight positive revision to GDP growth in the final quarter of 2025, albeit with more limited effects on the economic outlook.

Jaromír Šindel

06. 03. 2026

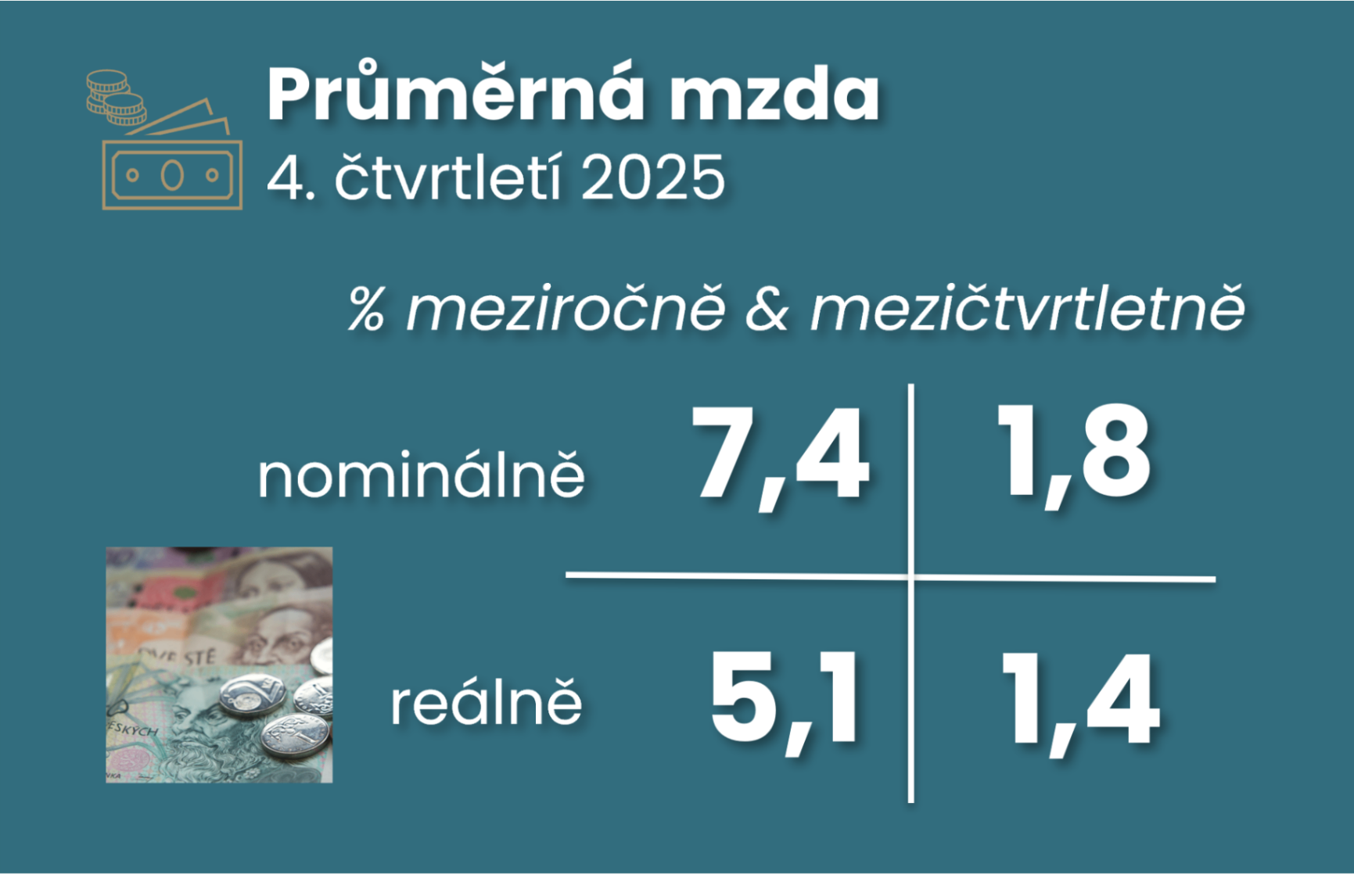

Wage growth remained strong at the end of 2025. Average wages rose by 7.4% year-on-year and added 7.2% for the year as a whole. Thanks to low inflation, this meant real wage growth of 4.7%, higher than forecast. While nominal growth should slow this year, real wages may continue to grow solidly. The average nominal wage reached CZK 49.2 thousand last year, surpassing CZK 50 thousand at the end of the year on a seasonally adjusted basis and reaching almost CZK 51 thousand in market sectors. The median wage of CZK 42 thousand was approximately 85% of the average wage.

29. 01. 2026

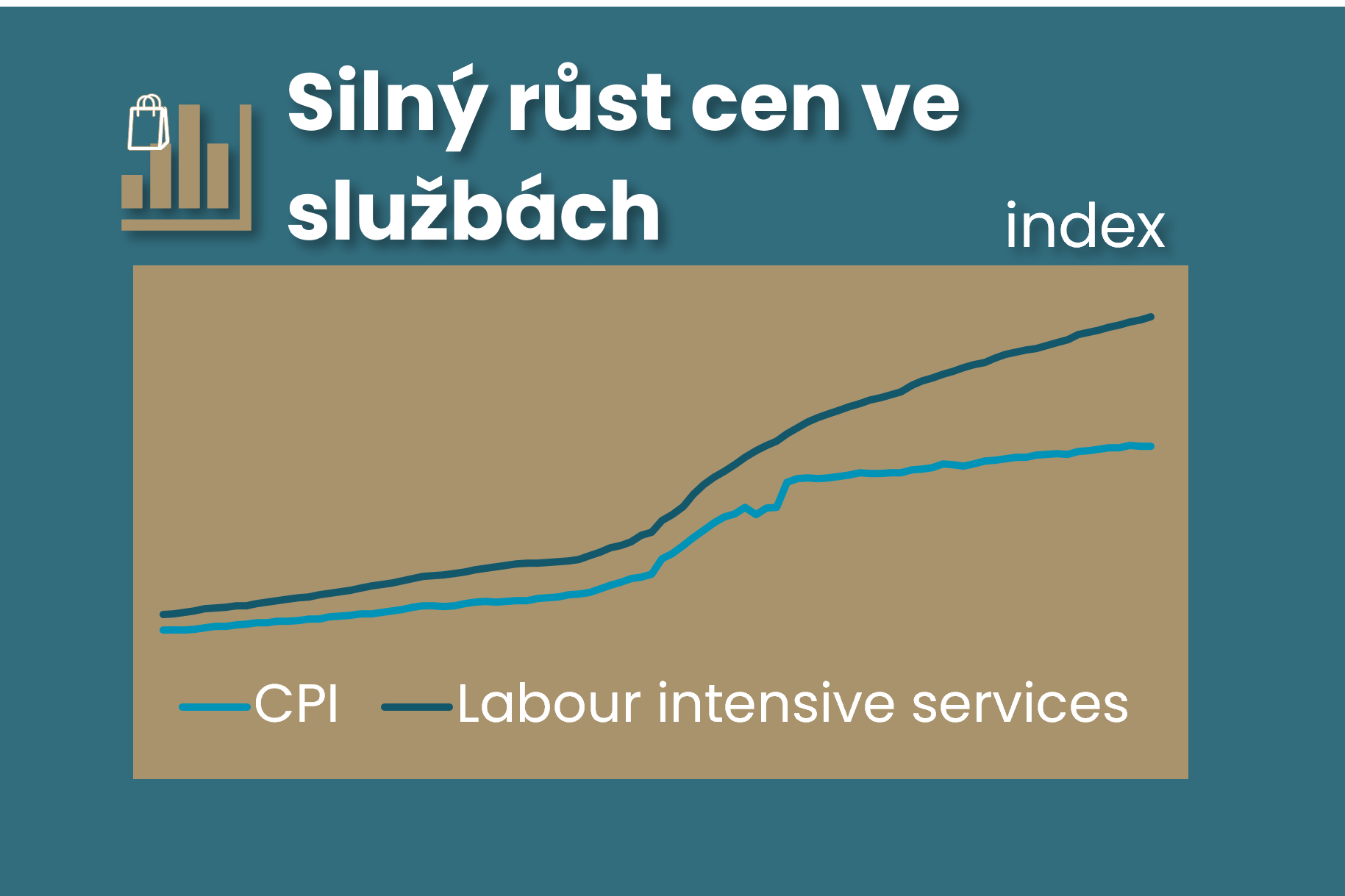

Comment by Jaromír Šindel, Chief Economist of the CBA: The analysis summarizes the government's regulatory steps that will further slow consumer price growth this year, probably well below 2%. What does this mean for the CBA, which seems to be starting to deflate the pigeon balloons, at least more than at the end of last year? Given its earlier communications, where inflation is headed in 2027 should be key, which will also indicate the direction of core inflation in the months ahead. And it is not just the case of still strongly rising services prices that are the focus of this analysis, the first part of the triptych ahead of the CNB's February board meeting.

04. 12. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: Consumer price growth slowed to 2.1% yoy in November. The main reason was a deeper decline in food prices, partly due to a slowdown in core inflation from the recent 2.8%. Thus, although inflation surprised positively, food price volatility and still strong rapid wage growth of 7.1% in Q3 will dampen the CNB's willingness to return to rate cuts. And the same reasons dampen the risks to the CBA's outlook for consumer inflation next year at around 2.2%. There remains a significant gap in the recovery in real gross wages between the market and non-market sectors.

08. 09. 2025

Economic commentary by Jaromír Šindel, Chief Economist of the CBA: Although the economy breathed a half-percent growth in the second quarter, the July figures were rather disappointing and suggest a cooling. However, the Czech economy is generating upside risks to inflation, which limits the room for manoeuvre of the CNB, which is likely to stick to the CNB's 3.5% terminal interest rate thesis. August's registered unemployment confirmed a worse trend, which, however, is not confirmed by other data.

27. 06. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

05. 06. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

12. 05. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

09. 04. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

07. 04. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

07. 03. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

03. 09. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

04. 06. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

05. 03. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA