Detailed information on the development of the domestic mortgage market based on the CBA data collection, which captures data from all domestic banks and building societies providing mortgage loans. The complete dataset is attached to the latest CBA Hypomonitor commentary, which can be found below.

Number and total amount of new mortgages granted, including refinancing and loan increases

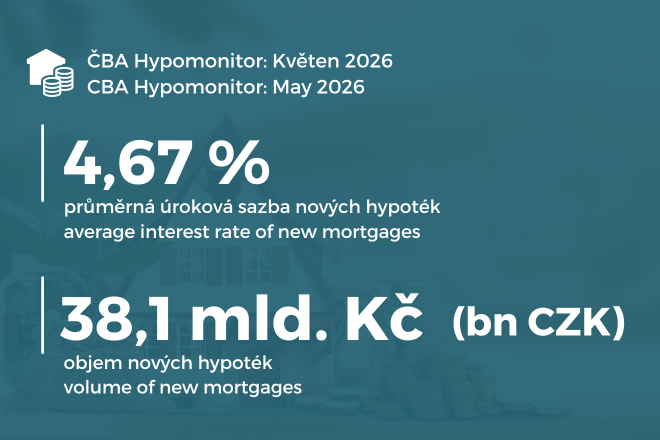

In May 2026, banks and building societies actually issued new mortgages (excluding refinancing) totaling CZK 38.1 billion.

Jaromír Šindel

18. 05. 2026

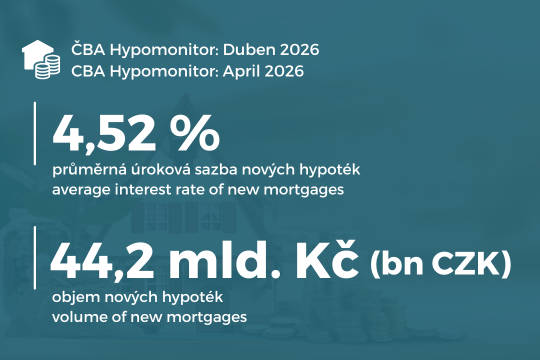

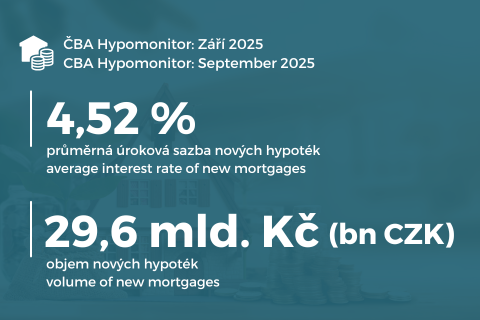

Average mortgage rate rises to 4.52%

Jaromír Šindel

13. 05. 2026

This year is bringing a strong wave of expiring mortgage rate fixations, while the shorter fixation periods agreed in recent years will further increase these volumes in the years ahead. Building on the central bank’s latest estimate that mortgage fixations worth an average of CZK 534 billion per year will expire between 2026 and 2028, we present alternative interest-rate shock scenarios depending on the path of mortgage rates. In 2027–2028, the negative interest-rate shock is expected to ease to 0.1–0.6 percentage points, down from 1.1–1.4 percentage points this year. However, we also outline a more adverse scenario involving a stronger interest-rate shock. This year, the negative interest-rate shock affecting expiring mortgage fixations from the low-rate period will amount to roughly 3.5% of the average household income of mortgage applicants, although across all households the average impact will be about half that level. In both cases, the expected real growth in wages and salaries should be sufficient to offset the shock.

Jaromír Šindel

16. 04. 2026

The average amount of a new mortgage exceeded CZK 4.8 million

Jaromír Šindel

15. 04. 2026

Comment by Jaromír Šindel, Chief Economist of the CBA: Mortgage rates are significantly determined by the movement of market interest rates. However, structural factors in the banking market are also important. The CNB's investigation of credit conditions in our analysis helps to explain what factors influence the difference between mortgage and market interest rates deviating from its normal level. The CBA analysis shows that a combination of stronger demand and competition among banks plays a key role. It is the latter that can lead to more favourable rates for clients without undermining market stability. The difference between mortgage rates and market rates that we have been monitoring is therefore mainly dampened by stronger demand, but in an environment of growing competition, which is key. Banks' profitability also plays a role, acting as a corrective mechanism to maintain competitive interest rate spreads but also market stability.

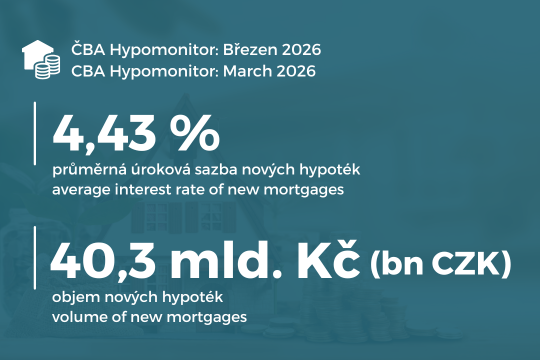

Jaromír Šindel

13. 03. 2026

February ranked among the five strongest mortgage months ever in terms of volume in billions of crowns, but also with a continued strong number of new mortgage originations.

16. 02. 2026

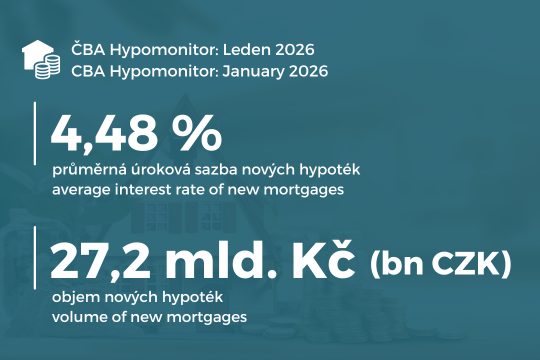

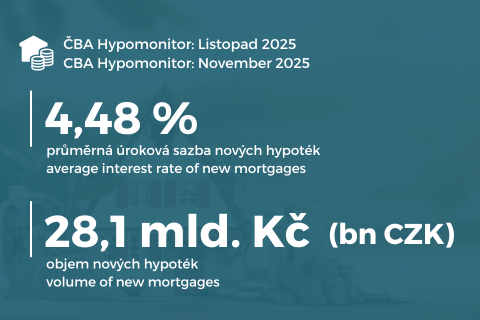

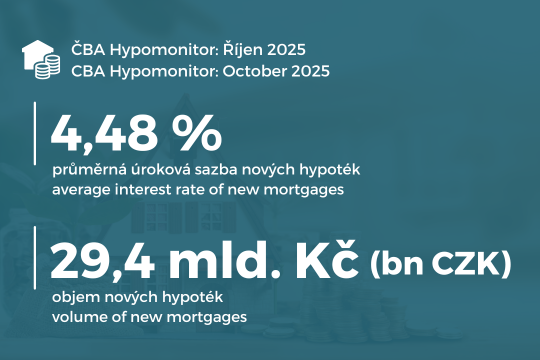

Average mortgage rate fell to 4.48%

16. 01. 2026

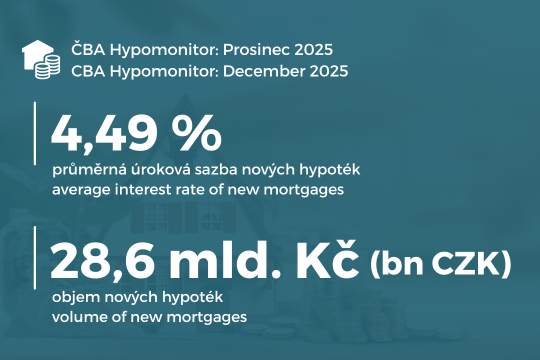

Average mortgage rate rises to 4.49%

15. 12. 2025

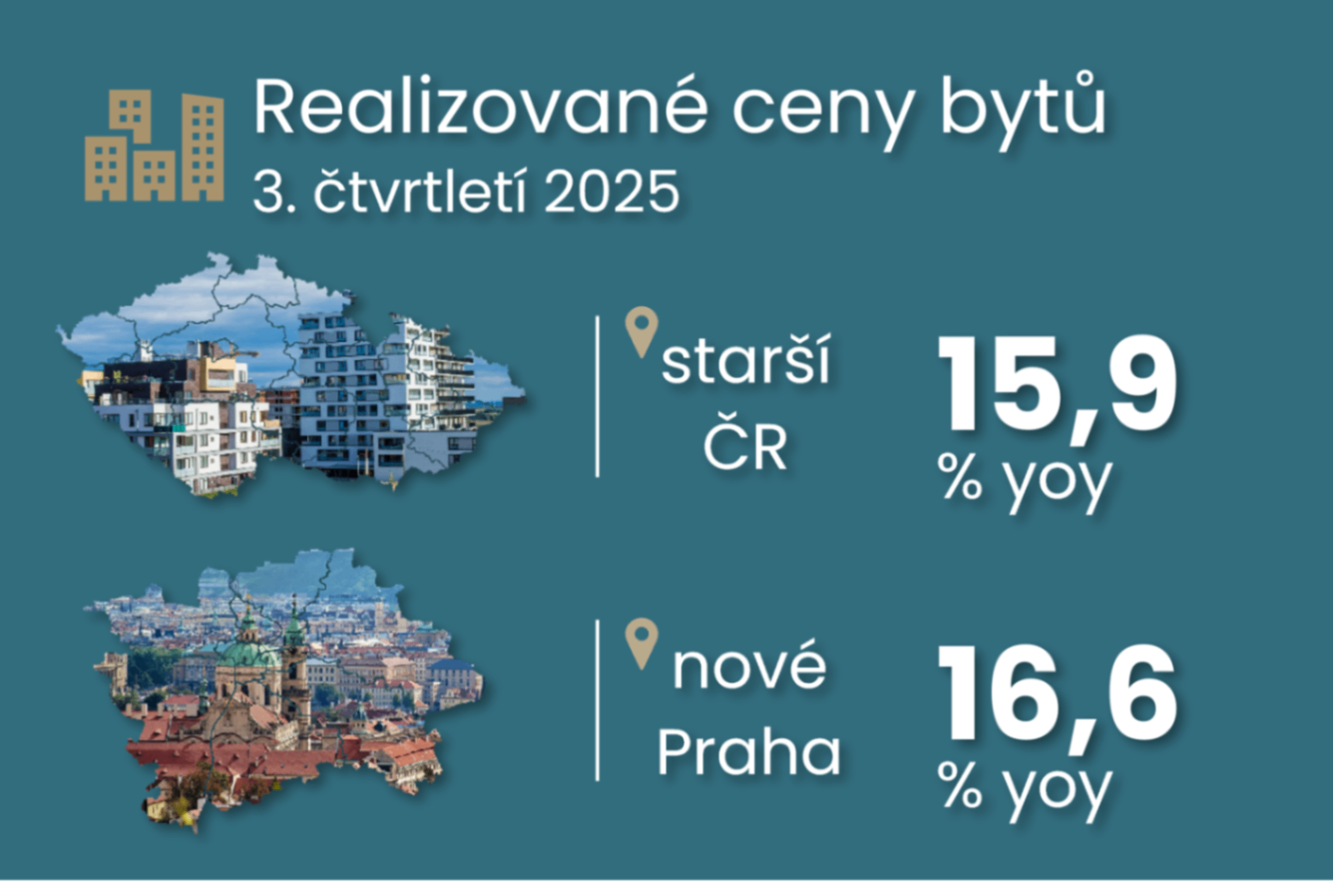

Comment by Jaromír Šindel, Chief Economist of the CBA: According to the Czech Statistical Office, realised prices of older flats in the Czech Republic rose by 3.7% quarter-on-quarter in the third quarter, which exceeds income growth for the seventh quarter already and maintains the too brisk annual pace of property prices at around 16%. Higher property prices are also making their way into the CNB's macroprudential capital policy settings, with discussion over the (arguably unscary) possible introduction of a sectoral systemic buffer, as well as less intuitive discussions over the role of investment activity by non-financial corporates in setting the countercyclical capital buffer.

12. 12. 2025

Since the beginning of the year, their volume has reached CZK 293 billion, i.e. CZK 84 billion more than a year ago.

27. 11. 2025

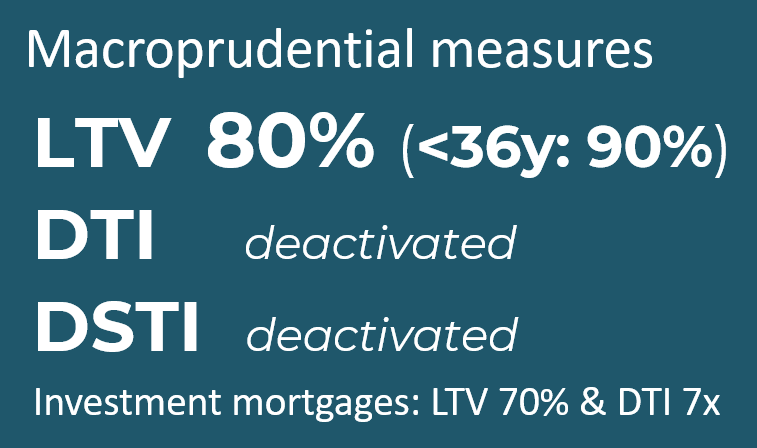

Comment by Jaromír Šindel, Chief Economist of the CBA: The Central Bank, through stricter requirements in the form of recommendations for investment mortgages, has decided to make a modest effort to correct mortgage demand on the real estate market, which remains very tight in terms of prices, mainly due to the supply side - see the drop in building permits.

14. 11. 2025

Since the beginning of the year, the volume of new mortgages has reached CZK 265 billion

14. 10. 2025

The volume of new mortgages has reached CZK 235 billion since the beginning of the year

15. 09. 2025

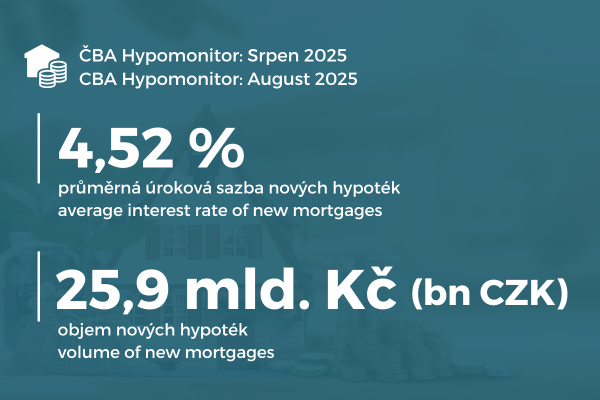

The rate fell slightly to 4.52%.

14. 08. 2025

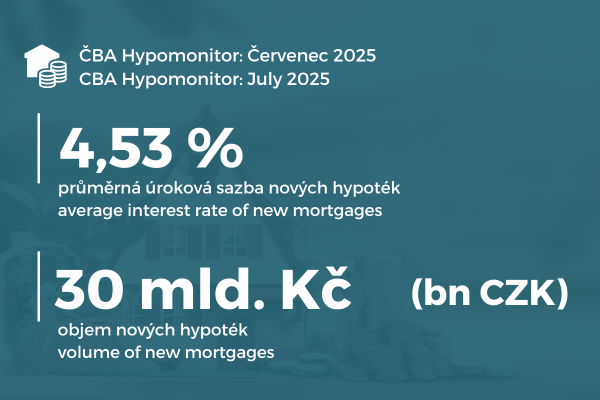

The rate fell slightly further to 4.53%.

15. 07. 2025

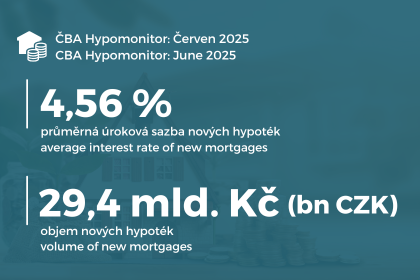

In June 2025, banks and building societies granted new mortgages worth CZK 29.4 billion.

13. 06. 2025

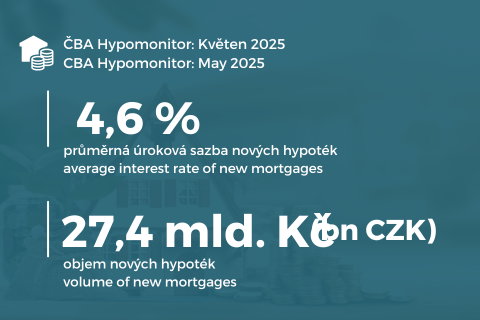

Average mortgage rate fell to 4.6%

16. 05. 2025

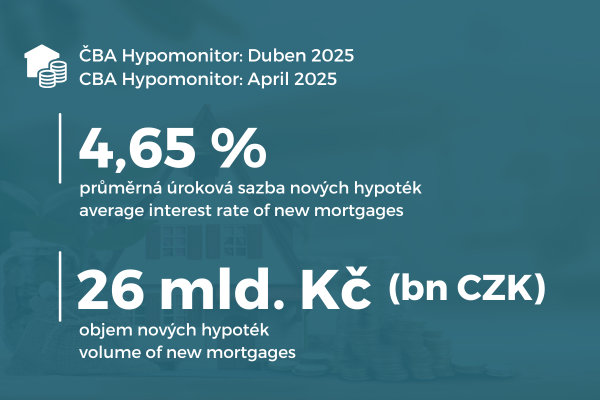

Despite the slight correction, April continued to see strong volumes of new mortgages supported by another slight decline in the average mortgage rate to 4.65%.

14. 04. 2025

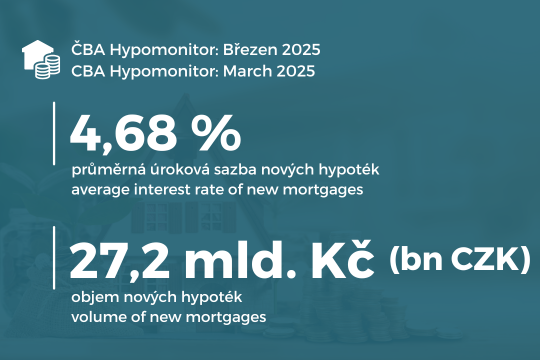

March continued to see strong new mortgage volumes supported by another slight fall in the average rate to 4.68%

14. 03. 2025

February still suggests continued strong volumes of new mortgages, thanks to a further decline in the average rate to 4.72%.

17. 02. 2025

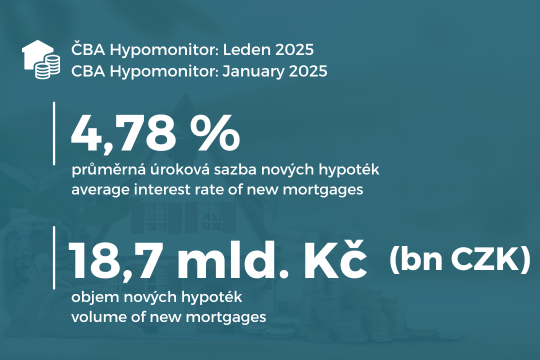

Average mortgage rate fell to 4.78 per cent

15. 01. 2025

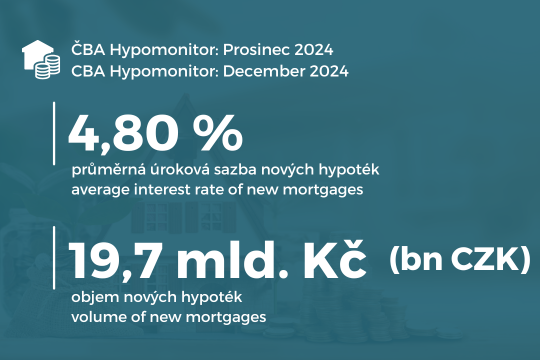

Average mortgage rate fell to 4.8 percent

13. 12. 2024

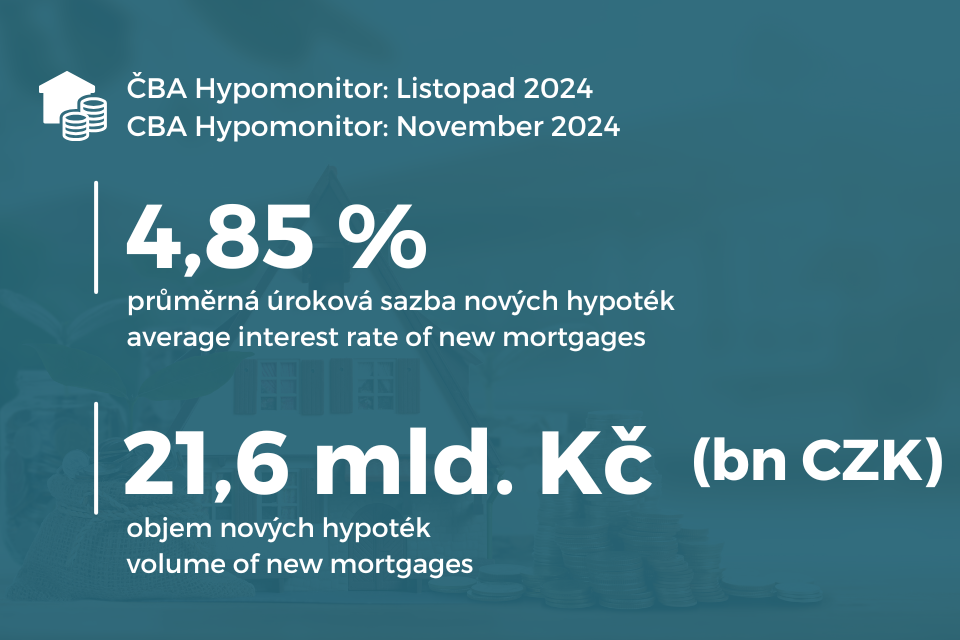

Average mortgage rate fell to 4.85 per cent

18. 11. 2024

Average mortgage rate fell to 4.9 per cent

11. 10. 2024

Average mortgage rate fell to 4.96 per cent

13. 09. 2024

The average mortgage rate fell to 4.98 percent, the lowest in two years

13. 08. 2024

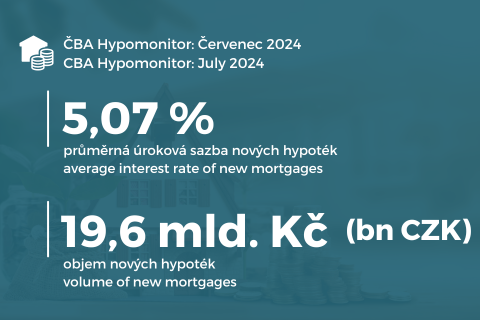

The average rate increased slightly to 5.07 percent

12. 07. 2024

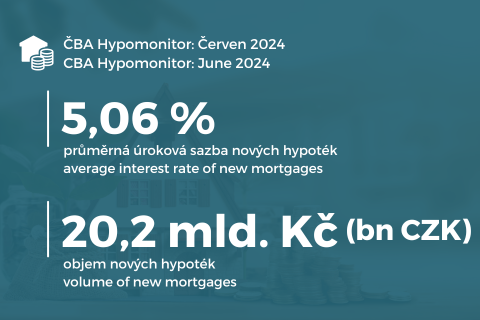

Average interest rate fell to 5.06%

13. 06. 2024

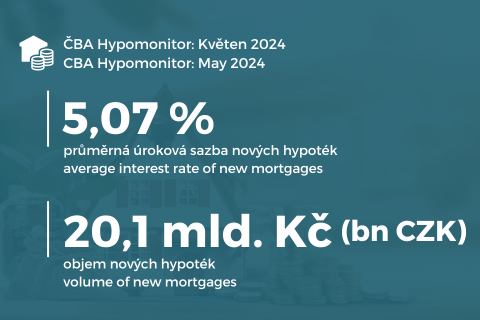

The average mortgage rate fell to 5.07% in May.

15. 05. 2024

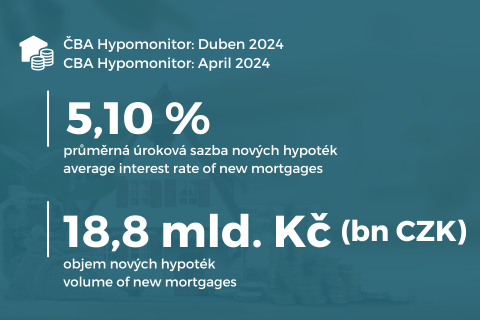

The average mortgage rate fell to 5.10%.

12. 04. 2024

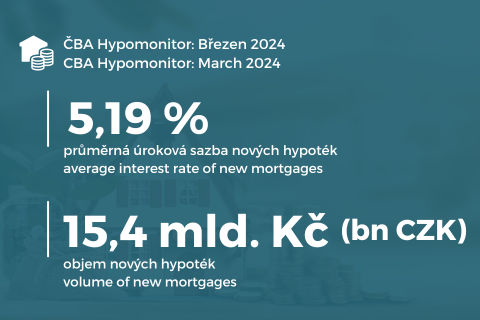

Average mortgage rate fell to 5.19%

14. 03. 2024

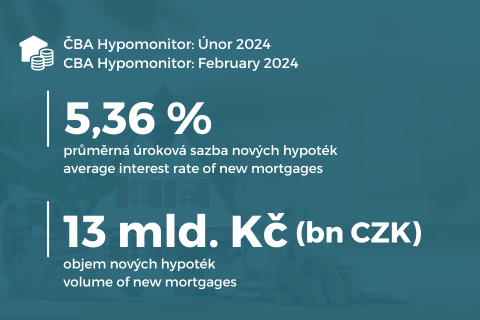

Average mortgage rate fell to 5.36% in February

14. 02. 2024

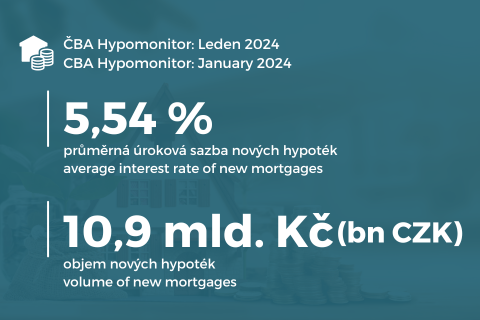

Interest in mortgages almost doubled year-on-year in January.

14. 02. 2024

Interview with Jakub Seidler, Chief Economist of the Czech Banking Association

18. 01. 2024

Interview with Jakub Seidler, Chief Economist of the Czech Banking Association

15. 01. 2024

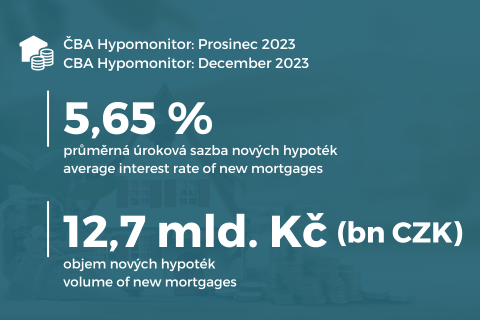

Mortgage market continues to revive, interest rate fell to 5.65% in December

14. 12. 2023

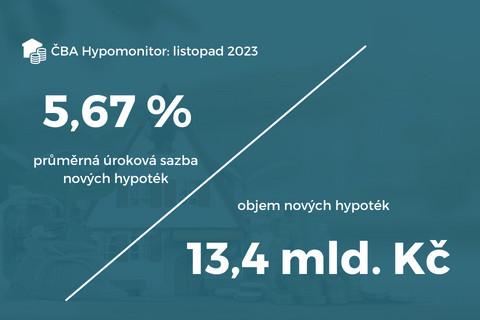

CBA Hypomonitor: Mortgage market held at October level in November, interest rate fell to 5.67 %