Higher house prices spark richer debate over central bank macroprudential policy than first appears

Comment by Jaromír Šindel, Chief Economist of the CBA: According to the Czech Statistical Office, realised prices of older flats in the Czech Republic rose by 3.7% quarter-on-quarter in the third quarter, which exceeds income growth for the seventh quarter already and maintains the too brisk annual pace of property prices at around 16%. Higher property prices are also making their way into the CNB's macroprudential capital policy settings, with discussion over the (arguably unscary) possible introduction of a sectoral systemic buffer, as well as less intuitive discussions over the role of investment activity by non-financial corporates in setting the countercyclical capital buffer.

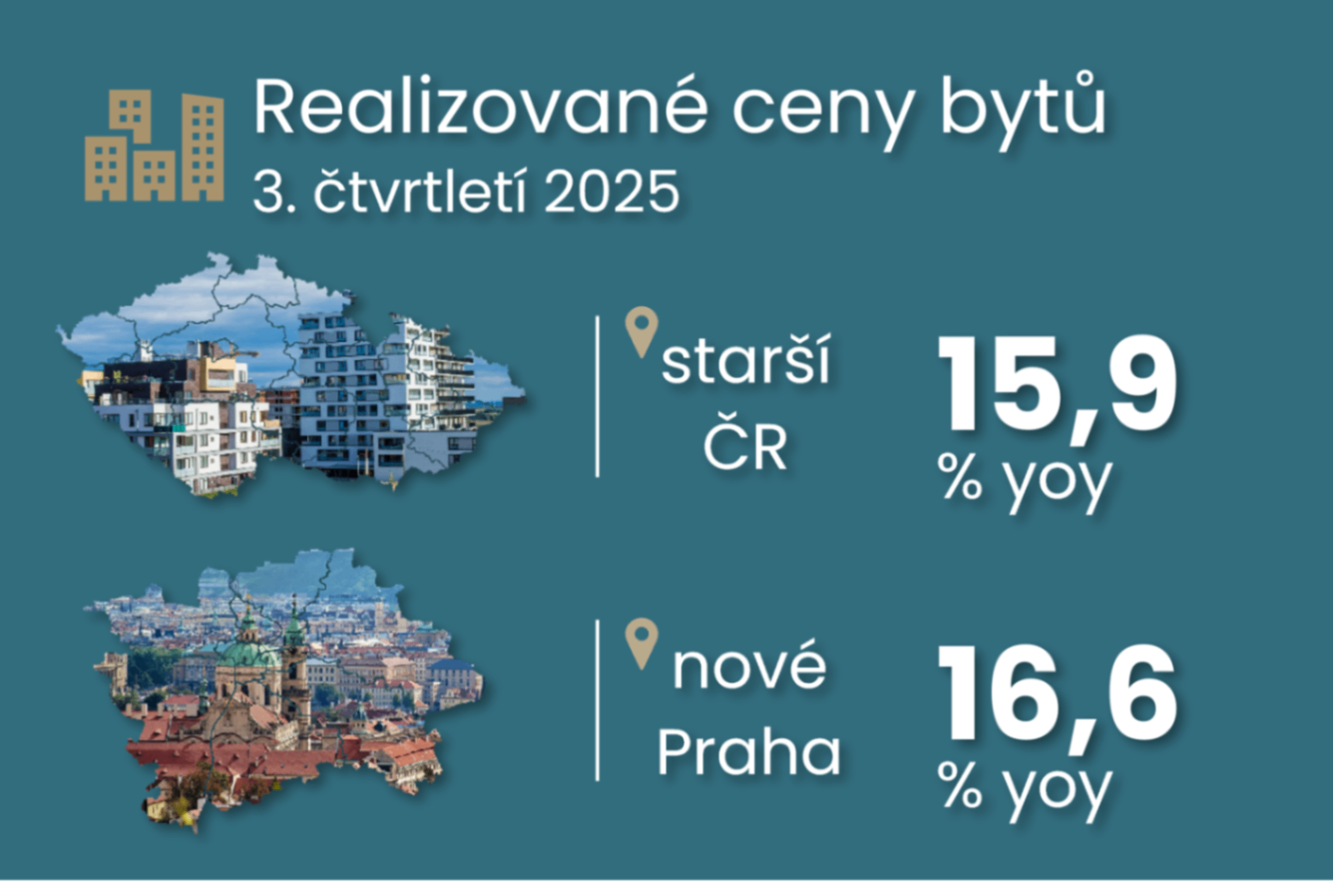

House prices continued to rise briskly in the third quarter, also in relation to purchasing power, for the seventh quarter in a row

Realised prices of older flats in the Czech Republic rose by 3.7% quarter-on-quarter in Q3, according to the CZSO, maintaining a very high year-on-year house price growth rate of around 16%. Although new realised prices of flats in Prague rose "only" by less than 2% quarter-on-quarter, this follows a more than 6.5% jump in the previous quarter. Their year-on-year pace thus reached almost 17%. Offered prices of flats in the Czech Republic reached almost 18% yoy. This is another stronger quarter-on-quarter rise in house prices compared to the already strong growth in incomes (see analysis of wage growth here and chart 2 below), The house price methodology is discussed here.

Flat Zone's continued strong growth is also evidenced by transaction prices, up nearly 14% year-over-year for the entire apartment segment in the third quarter, with nearly 19% growth for older apartments and about 11% for new and replacement apartments.

See the charts below for more numerical detail.

Unchanged countercyclical buffer at 1.25%, but counterintuitive forward guidance linked to corporate investment activity

The discussion in the CNB board over the countercyclical buffer did not change much according to the minutes, with VG Frait recalling the possibility of a debate on a higher CCyB rate (currently 1.25% vs. a recommendation for 1.45% due to the estimate of higher losses; see the last two charts) if the growth trend continues. However, the rest of the Board prefers the status quo while monitoring risks, also given that the current growth phase mainly reflects the real estate and mortgage market, where the impact of a higher CCyB is limited by the lower RWA weight. Thus, a higher CCyB would dampen corporate lending rather than mortgage lending.

However, the final paragraph states that the future setting of the CCyB will depend not only on the real estate and mortgage markets but also on the investment activity of non-financial corporations. This conclusion implies a less intuitive macroprudential policy response to the current biggest weakness of the Czech economy, which is the slow recovery of fixed investment in machinery and equipment (the inflationary effect arises because of the slow growth of the economy's more efficient production potential; analysis of Q3 numbers here).

Sectoral capital buffer as a solution to the lower countercyclical buffer efficiency in the current "mortgage" financial cycle? Probably not a quick fix.

In discussing the macro-prudential mortgage indicators (DTI, DSTI, LTV), two Board members - Eva Zamrazilová and Jan Kubíček - pointed to the possible use of the sectoral capital buffer (sSyRB) in the current phase of the higher financial cycle associated with house prices. According to the ESRB, the sectoral version of the systemic buffer is currently used by almost half of the countries, namely 10 out of 21 countries that apply the systemic buffer (SyRB). In the Czech Republic, it is set at 0.5% of risk-weighted assets. However, only eight of these countries use a sectoral variant focused on residential housing (the remaining one, France, applies it to subprime corporates and Italy to broader risks associated with domestic lending). However, according to the CNB minutes, this step would require detailed analysis.

Neither the minutes nor the Financial Stability Report provided additional information on the stricter recommendations on so-called. investment mortgages, which I analysed here CNB tightens conditions for investment mortgages: 9% impact or needed redistribution of demand?

The third quarter maintained an all-too brisk annual pace of property prices, around 16% according to the CSO, as evidenced by Flat Zone's transaction prices.

Another quarter with stronger house price growth compared to wage and salary growth

Comprehensive overview of real estate prices

Flat Zone says the third quarter brought a recovery in apartment price growth both in Prague and outside Prague

According to Flat Zone, the transaction prices of apartments are more than 20% higher than in 2023.

The average transaction price of flats in the Czech Republic reached CZK 95.6 thousand in the third quarter of 2025. CZK per sqm.

Transactions with both new and older flats revived in the third quarter

Prague apartment transaction price growth in the third quarter was driven by growth in the price of "older bricks" , but also by larger transactions in first-time sales

Older brick, but also panel, the main drivers of housing price growth in the Czech Republic

The estimated losses imply a slightly higher countercyclical buffer rate compared to its current rate of 1.25%

... primarily due to higher unexpected cyclical losses