Real estate prices

The latest indicators on the development of the domestic real estate market, both from official CSO data and Flat Zone data.

The latest indicators on the development of the domestic real estate market, both from official CSO data and Flat Zone data.

Apartments: CZK 1,000 per square meter; Single-family homes: CZK 100,000 per transaction

Q1 / 2026

Q1 2026

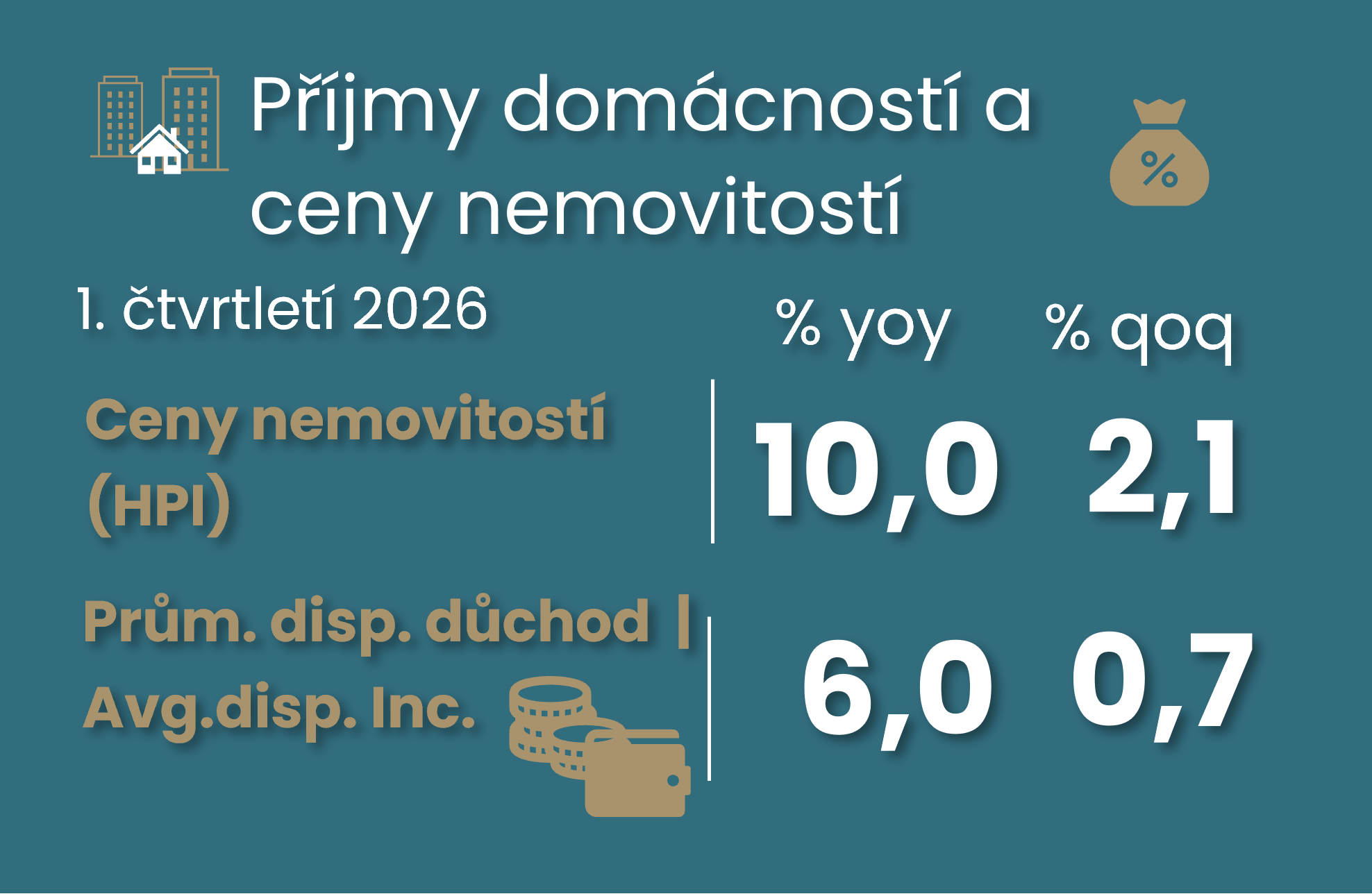

The Czech household savings rate remained at 20% in the first quarter of this year, still high even by international standards. Household disposable income slowed to 0.7% quarter on quarter, while property prices continued to rise by roughly 2%. The GDP revision showed weaker household consumption, but also a less negative productivity story thanks to stronger value added in industry. However, despite somewhat more moderate growth in the past, unit labour costs remain on a strong upward trend, which, together with high core inflation growth, is unlikely to bring a dovish turn at the CNB. That said, my interpretation of the new data from the Czech Statistical Office, especially for the first quarter, is significantly affected by the alignment of quarterly figures with the new annual data for 2025. The next quarterly release may therefore bring yet another story about the economy in the first quarter.

While the growth in actual apartment prices slowed to approximately 2.5% quarter-over-quarter in the first quarter, with significantly different trends between Prague and the rest of the country, However, even the current milder growth does not yet suggest a significant slowdown in year-over-year apartment price growth this year. Asking prices do not indicate this yet. This is especially true if there is a shift of pent-up demand for more expensive Prague apartments to the regions. Data from Flat Zone show an average transaction price of CZK 98,000 per square meter for apartments in the first quarter. Stricter criteria for so-called investment mortgages, as well as higher mortgage interest rates, may further cool the real estate market; however, higher wage growth keeps real mortgage interest rates negative.

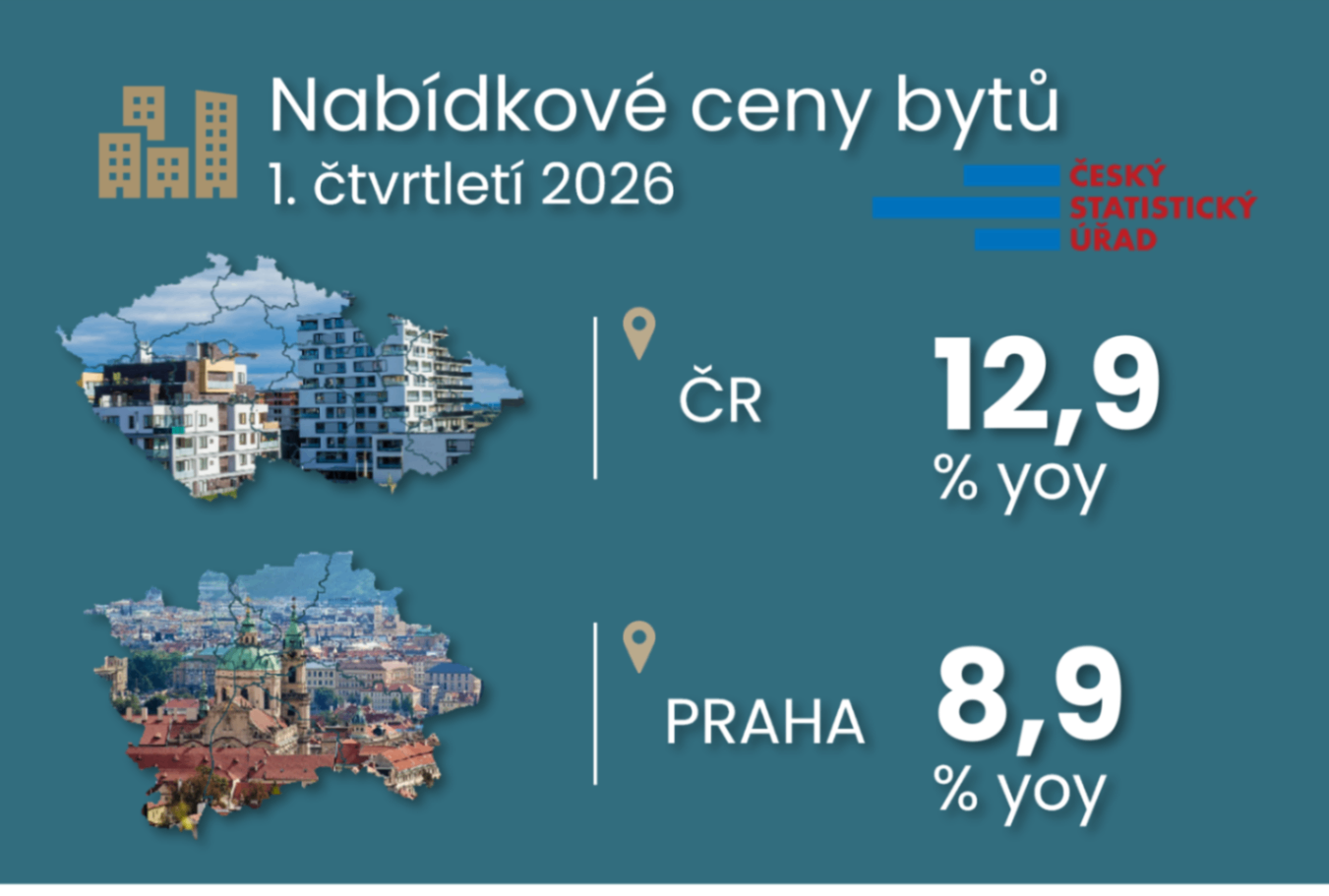

In Q1 2026, the offer prices of flats rose by 2.7% quarter-on-quarter. The housing market is slowing down slightly in terms of offer prices after last year's significant increase in prices, but price growth remains above average and is not sufficient to improve the ratio of housing prices to household incomes significantly. In the regions, prices continue to rise faster than in Prague and the year-on-year cooling is still evident in Prague. Overall annual growth in the supply side of house prices has slowed to 12.9% from the previous 16-18% during 2025. Higher supply side house prices have been heralded by continued growth in average mortgage rates.

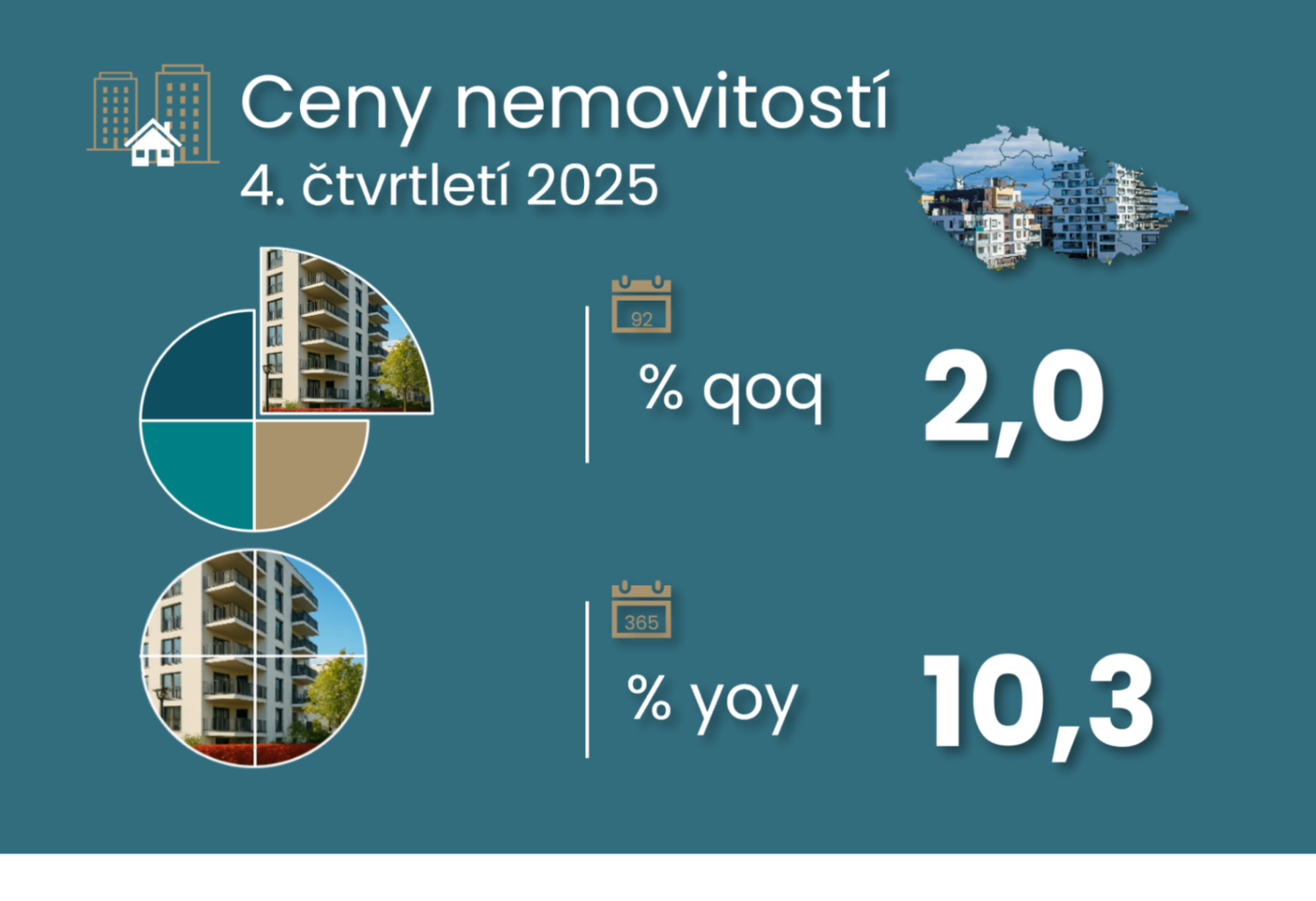

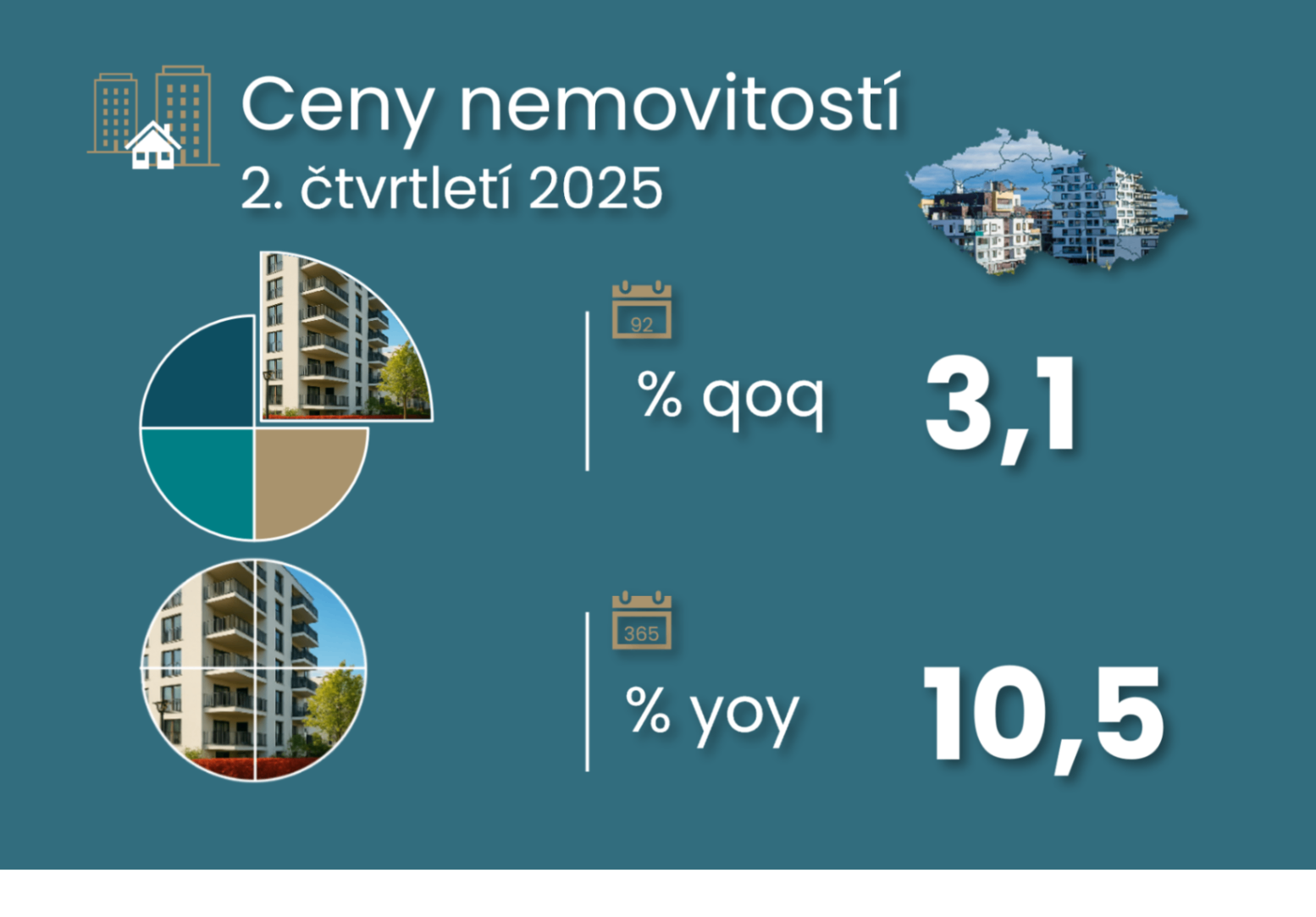

According to the CSO statistics, property prices, which include land and family houses, rose by 2% quarter-on-quarter in the final quarter of 2025. This slowed from the previous average 2.6% increase in the previous four quarters. Although the income side of demand is still lagging, real household incomes accelerated more sharply at 1.4% q-o-q (up nearly 3% in nominal terms) at the end of last year. And so did the household savings rate, which rose to 19.7%. Moreover, both figures were positively revised and there was a slight positive revision to GDP growth in the final quarter of 2025, albeit with more limited effects on the economic outlook.

This continues to boost activity, although not at the rapid pace seen in 2023-2024.

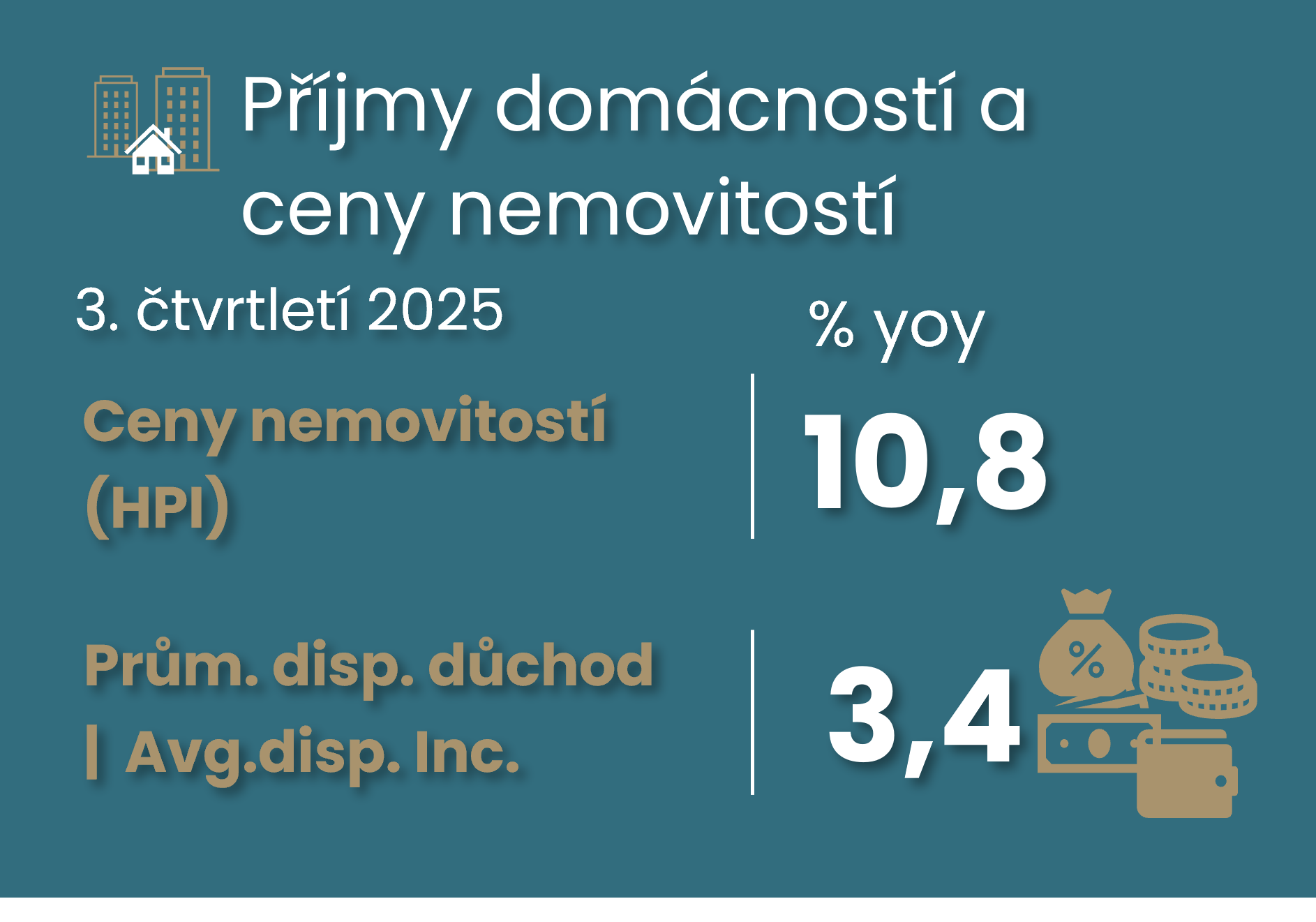

Comment by Jaromír Šindel, Chief Economist of the CBA: Even the third quarter of 2025 did not bring a significant recovery in household disposable income. Despite this, the household savings rate has been abnormally high for almost six years. In Q3, it was 18.4%. Weaker quarter-on-quarter growth in disposable income has not kept pace with house prices for six quarters in a row. On a year-over-year basis, we are comparing 3.4% growth in disposable income vs. a 10.8% increase in home purchase prices including land (HPI).

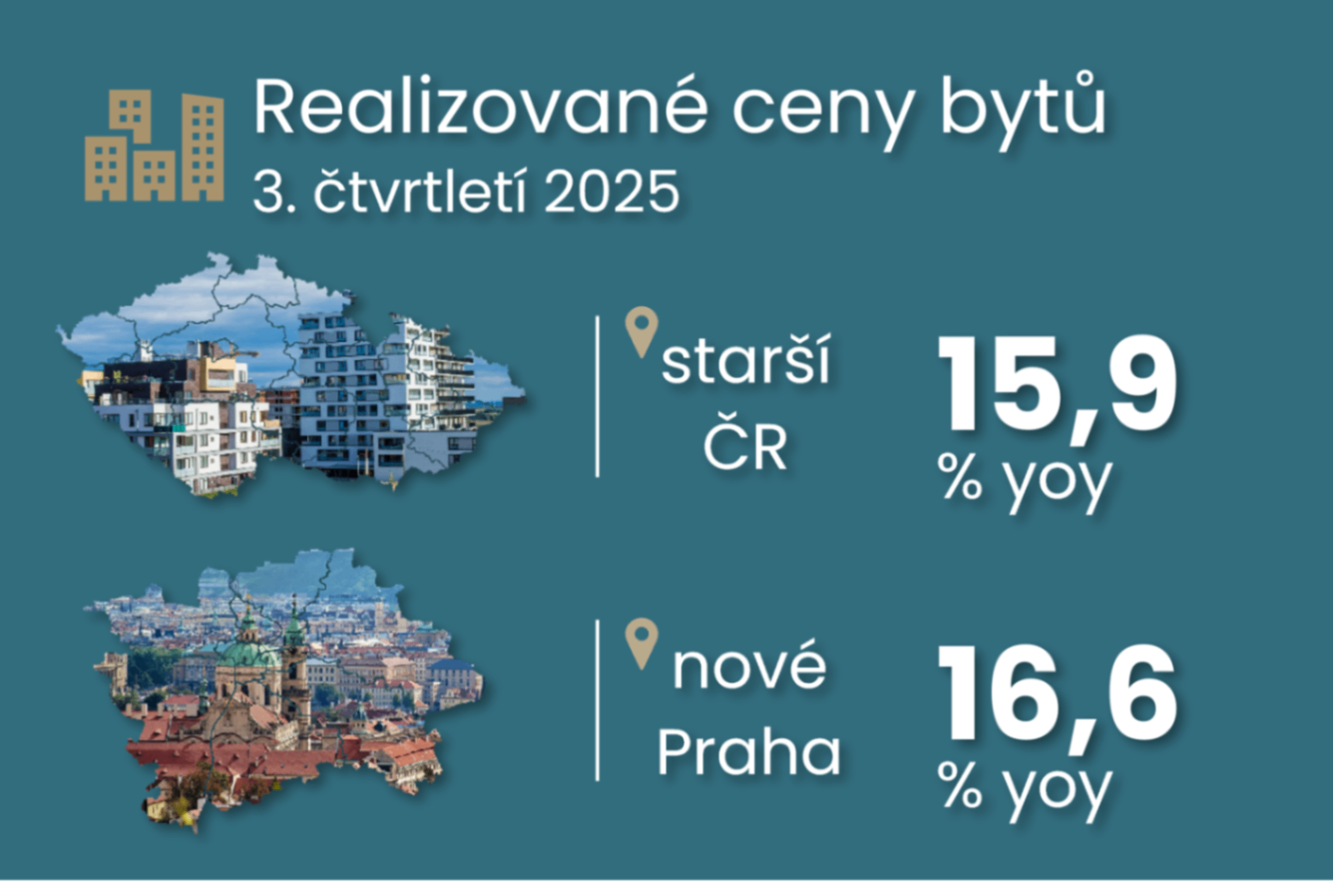

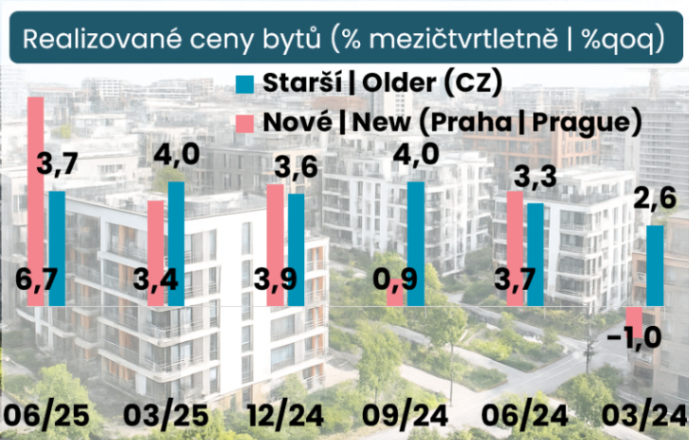

Comment by Jaromír Šindel, Chief Economist of the CBA: According to the Czech Statistical Office, realised prices of older flats in the Czech Republic rose by 3.7% quarter-on-quarter in the third quarter, which exceeds income growth for the seventh quarter already and maintains the too brisk annual pace of property prices at around 16%. Higher property prices are also making their way into the CNB's macroprudential capital policy settings, with discussion over the (arguably unscary) possible introduction of a sectoral systemic buffer, as well as less intuitive discussions over the role of investment activity by non-financial corporates in setting the countercyclical capital buffer.

Comment by Jaromír Šindel, Chief Economist of the CBA: The recovery in disposable income in Q2 was still dampened by fiscal policy, so it remained weaker compared to the increase in wages and property prices. Nevertheless, households managed to increase both consumption and their savings.

Economic commentary by Jaromír Šindel, Chief Economist of the CBA: I estimate overall growth in realised house prices of 4.2% quarter-on-quarter, which has outpaced wage growth for the sixth quarter in a row.

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

House prices up 10.7%

Sales of older and new homes increased by tens of percent during 2023