Slight recovery in disposable income was enough for stronger consumption and higher savings, but not for more expensive real estate

Comment by Jaromír Šindel, Chief Economist of the CBA: The recovery in disposable income in Q2 was still dampened by fiscal policy, so it remained weaker compared to the increase in wages and property prices. Nevertheless, households managed to increase both consumption and their savings.

Growth in real disposable income rose by 1.8% quarter-on-quarter in Q2, slower than the 2.3% rise in average employment income. As household consumption grew at a slower pace of 1% in the second quarter, the household savings rate rose to 18.4% (see Chart 2). However, nominal disposable income, with 2.1% growth, did not keep pace with house prices, which rose by 3.1% for the fifth consecutive quarter. The dynamics of the average mortgage amount suggest stabilisation rather than further acceleration of house prices (see Chart 6).

Fiscal policy, through higher net income taxes, is holding back a stronger recovery in disposable income - similar to the pre-recession period (see Chart 3). On the other hand, income from property has supported its growth, but not net interest (see Chart 4), which is consistent with the current phase of the central bank's monetary cycle and may also be related to a shift of savings from banking accounts to investment vehicles.

The half-percent quarter-on-quarter GDP growth in Q2 was supported by an acceleration in private consumption to 1%, despite a high household savings rate, which rose slightly to 18.4% from 17.8% in the previous quarter. Savings thus remain well above the pre-quarter average (almost 12%) but below last year's average of 20.3%.

Both stronger consumption and higher savings reflect rising employment income, which increased by 2.3% in real terms. Disposable income per person thus rose by 1.8% after a 1.4% fall at the start of the year. The slower growth in disposable income continues to be linked to rising net household taxes (fiscal consolidation effect) and a weaker contribution from net interest.

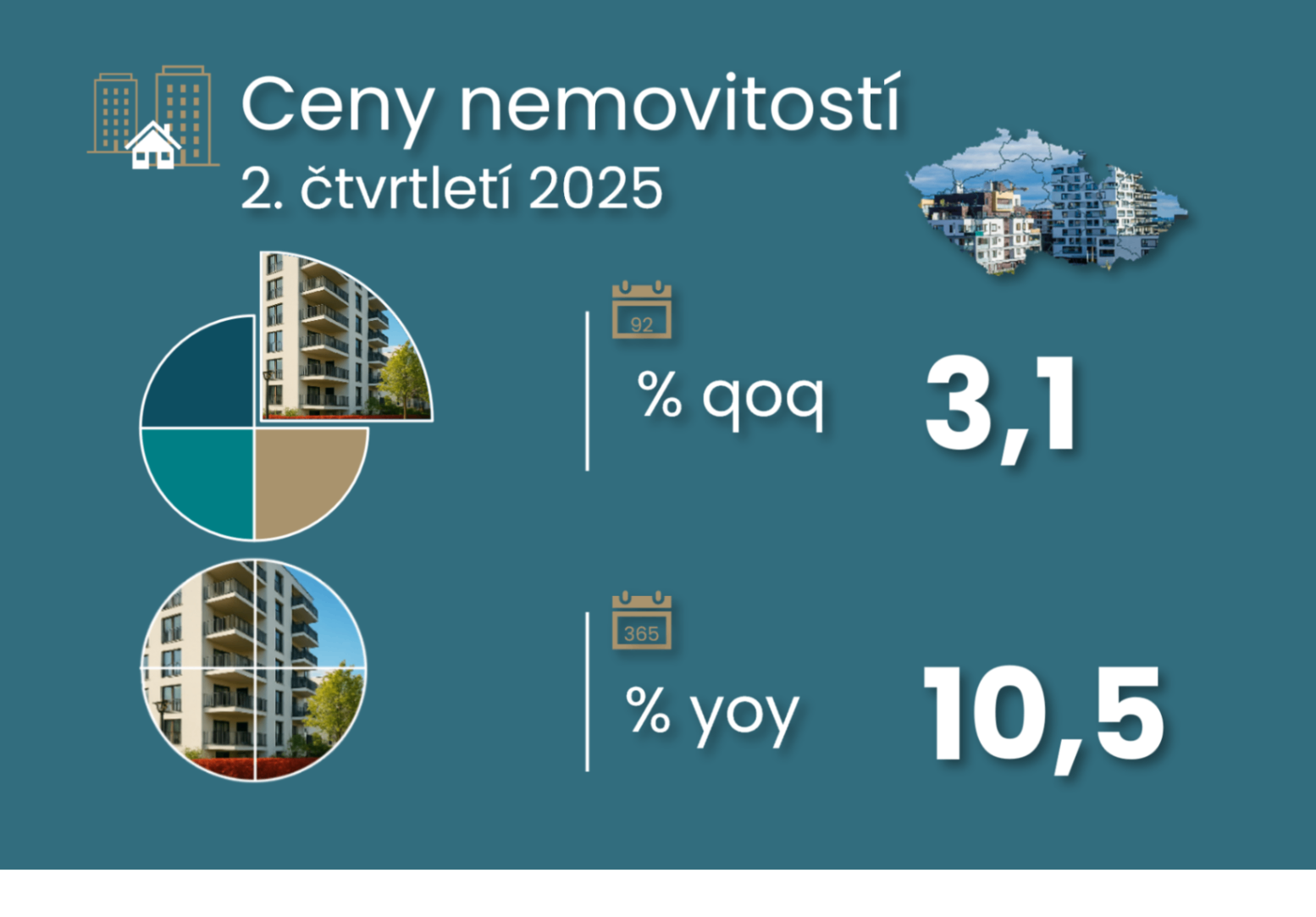

House prices (apartments, houses and land) accelerated to 3.1% in Q2 from 2.4% in the previous quarter (see Chart 5). Annual growth thus increased only slightly to 10.5% after a 10% rise in the first quarter. The house price index grew more slowly than house prices themselves (around 16% year-on-year and over 4% quarter-on-quarter). The costs associated with owner-occupied housing rose by around 5% y-o-y, half the rate of house prices, in line with long-term trends (see chart below).

Disposable income and household savings

Fiscal policy, through higher net income taxes, is holding back a stronger recovery in disposable income - as in the pre-covid period

Income from wealth has supported its growth, but not net interest, which is consistent with the current phase of the central bank's monetary cycle and may also be related to a shift of savings from current accounts to investment instruments.

Real estate prices

House prices (flats, detached houses and land) accelerated to 3.1% in Q2 from 2.4% in the previous quarter. Annual growth thus increased only slightly to 10.5% after 10% growth in the first quarter.

The dynamics of the average mortgage amount suggests stabilisation rather than further acceleration of property prices.

Costs associated with owner-occupied housing rose by around 5% year-on-year, half the rate of house prices, in line with long-term trends

Nominal disposable income, however, with 2.1% growth for the fifth consecutive quarter, has not kept pace with house prices