Loans and deposits

Key indicators on the development of loans and deposits in the domestic banking sector from official Czech National Bank statistics

Commentary by Miroslav Zámečník, Chief Advisor to the Czech Banking Association

The Bank Board raised the interest rate by a quarter of a percentage point to 3.75%. Unsurprisingly, the main reason was the continued high growth in demand-driven, or “core,” inflation, which reflects stronger wage growth. However, the decision also reflects stronger credit growth and rising real estate prices. I view today’s decision as an effort by the central bank to keep consumer inflation in line with its inflation target over the longer term, which is not possible with core inflation hovering around 3%. Today’s decision reduces the risk premium—or rather, the uncertainty regarding the credibility of achieving the inflation target and the central bank’s independence. Below, I discuss further possible steps and their implications for the economy and the banking sector. If energy prices remain lower, this will reduce the likelihood of the CNB reaching a 4% interest rate. However, core inflation must lose momentum for the CNB to avoid reaching that level.

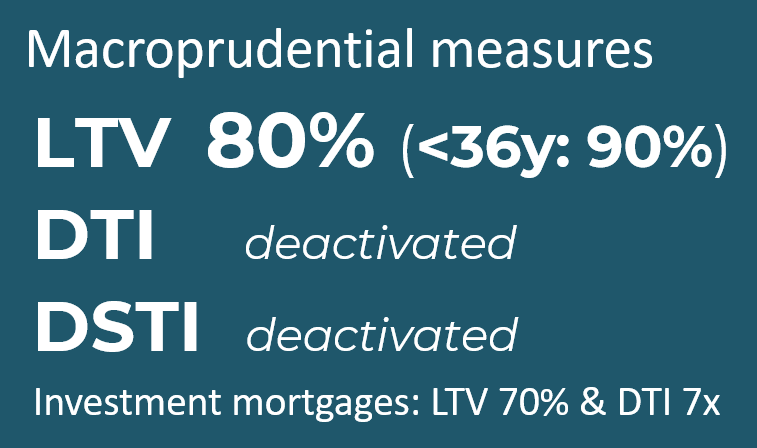

The countercyclical capital buffer should rise to 1.5% from July 2027, which will increase banks' total capital requirements to around 17% next year, in response to continued growth in lending to households and firms and lower perceived risks in the banking sector. Again, we are also seeing stronger wage growth outpacing productivity. In the case of rising investment credit, however, this is a dilemma for macroprudential policy. In addition to the financial cycle, the results of stress tests, including concerns about the interconnectedness of the banking and government sectors, are likely to have factored into the decision. It leaves mortgage rules unchanged.

This year is bringing a strong wave of expiring mortgage rate fixations, while the shorter fixation periods agreed in recent years will further increase these volumes in the years ahead. Building on the central bank’s latest estimate that mortgage fixations worth an average of CZK 534 billion per year will expire between 2026 and 2028, we present alternative interest-rate shock scenarios depending on the path of mortgage rates. In 2027–2028, the negative interest-rate shock is expected to ease to 0.1–0.6 percentage points, down from 1.1–1.4 percentage points this year. However, we also outline a more adverse scenario involving a stronger interest-rate shock. This year, the negative interest-rate shock affecting expiring mortgage fixations from the low-rate period will amount to roughly 3.5% of the average household income of mortgage applicants, although across all households the average impact will be about half that level. In both cases, the expected real growth in wages and salaries should be sufficient to offset the shock.

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Comment by Jaromír Šindel, Chief Economist of the CBA: Mortgage rates are significantly determined by the movement of market interest rates. However, structural factors in the banking market are also important. The CNB's investigation of credit conditions in our analysis helps to explain what factors influence the difference between mortgage and market interest rates deviating from its normal level. The CBA analysis shows that a combination of stronger demand and competition among banks plays a key role. It is the latter that can lead to more favourable rates for clients without undermining market stability. The difference between mortgage rates and market rates that we have been monitoring is therefore mainly dampened by stronger demand, but in an environment of growing competition, which is key. Banks' profitability also plays a role, acting as a corrective mechanism to maintain competitive interest rate spreads but also market stability.

Comment by Jaromír Šindel, Chief Economist of the CBA: The January slowdown in consumer price growth to 1.6% (mainly due to fiscal intervention in regulated energy prices) was accompanied by a discussion of a possible slight reduction in the CNB interest rate in order to fine-tune the recent interest rate cycle. However, persistently higher momentum in core inflation has left its interest rate unchanged, and risks associated with service prices and fiscal policy leave all options open for the central bank to move its interest rate. This is also true in light of the central bank's new forecast outlook, which admittedly encourages a marginal short-term interest rate cut before rising to 4% as early as the end of this year. With its decision and the reiteration of both inflationary and disinflationary risks, the central bank has tempered the dovish expectations of some market participants and the outlook for a 3.5% rate still seems likely. The key is the reiteration of the thesis of the sustainability of a return to the inflation target through softer core inflation.

Comment by Jaromír Šindel, Chief Economist of the CBA: The central bank did not surprise by unanimously leaving interest rates unchanged, i.e. with the two-week repo rate at 3.50%, for the fifth meeting in a row after a 25bp cut in May. Although the Board did not change its view of the risks and uncertainties surrounding the CNB's November forecast, it did assess the risks to inflation as balanced, given the risks in financial markets and the removal of the renewable energy levy, following November's upside assessment.

Comment by Jaromír Šindel, Chief Economist of the CBA: The Central Bank, through stricter requirements in the form of recommendations for investment mortgages, has decided to make a modest effort to correct mortgage demand on the real estate market, which remains very tight in terms of prices, mainly due to the supply side - see the drop in building permits.

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Comment by Jaromír Šindel, Chief Economist at the CBA: While the CNB unsurprisingly left interest rates unchanged with the two-week repo rate at 3.5%, the Board's statement on the monetary policy settings, however, was more surprising in its less hawkish tone, leaving open all possibilities for future monetary policy settings.

Commentary by Jaromír Šindel, Chief Economist of the CBA: Higher-than-expected wage growth will be the main, but not the only, reason for keeping the interest rate at 3.5% at the CNB's September meeting and for the intensification of the hawkish tone in the communication. The latter may indeed indicate a further upward movement in the interest rate, but rather in an unspecified distant horizon. A stronger koruna or tighter monetary policy through the longer end of the yield curve is unlikely to lead the CNB to a dovish mindset.

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Economic commentary by Jaromir Šindel, Chief Economist of the CBA (adjusted for published data on core inflation from the CNB and registered unemployment data, 18:00 8 August)

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Economic commentary by Jakub Seidler, Chief Economist of the CBA

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Interview with Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association