CNB tightens conditions for investment mortgages: 9% impact or necessary redistribution of demand?

Comment by Jaromír Šindel, Chief Economist of the CBA: The Central Bank, through stricter requirements in the form of recommendations for investment mortgages, has decided to make a modest effort to correct mortgage demand on the real estate market, which remains very tight in terms of prices, mainly due to the supply side - see the drop in building permits.

From April next year, the CNB will introduce stricter recommendations for investment mortgages, with the mortgage to property price ratio at 70% and the debt to annual net income ratio at 7 times. The potential impact on the market could reach between CZK 2.1-2.5 billion per month or around CZK 26-31 billion per year, according to a mechanical calculation. Of course, it will be interesting to see the possible frontloading effect, which the CNB does not "expect" from banks.

The CNB has thus decided to partially tighten conditions on the mortgage market in a segment that is not politically sensitive, i.e. it is not tightening conditions across the board, including the acquisition of own housing, which accounts for about 57% of new mortgages (see slide 5 in the CNB presentation). This segment will be supported in the future, according to the plans of the likely new government coalition. For example, through a state-concessionary loan for a down payment on the purchase of housing (according to the ANO Economic Strategy until 2027) and the planned state support for mortgage interest rates for young families with a child under six and for selected key professions (until 2028). From this perspective, the CNB's decision can be seen as forward-looking.

While investment mortgages (breaching recommended LTV and DTI ratios) account for around 9% of new mortgages, the share of young applicants aged up to 36 with one dependent (which includes not only children under 18) fell to 15% in the second quarter of this year from the long-term average of 21%. In this context, it is also important to note the gradual fall in the number of new births to 84,000 in 2024, 25% lower than the average of 113,000 from 2016-2021, reducing the potential impact of government support on the mortgage and property market.

The announced partial tightening of macroprudential measures is not that much of a surprise given the previous non-trivial discussion over the CNB's macroprudential policy settings in previous quarters, due to the strengthening mortgage market (see October's CBA Hypomonitor) and the significant increase in property prices (comments here). On the other hand, it may still be viewed as a surprise, as the CNB effectively carved out an exception to its own paradigm of refraining from macroprudential measures in the mortgage market in the absence of a material financial-stability risk.

Below, I analyse the tighter guidance on investment mortgages, as well as cosmetic changes to the CBA's other macroprudential measures on capital requirements.

The CNB's next stress test, which leads to a 20% fall in GDP over a three-year horizon compared to the expected trajectory, confirms the strong capital position of the Czech banking sector. It would still maintain a more than solid capital adequacy ratio at 17.4%, above capital requirements. The additional risk of default of the five largest bank borrowers would reduce the capital adequacy ratio to 14.7%, or to 14.4% if the koruna depreciates by 28% to 31 per euro. Banks' capital adequacy ratio reached 23.4% in the second quarter of this year.

What are so-called investment mortgages for the CNB, i.e. mortgages for the acquisition of investment residential property? These include the acquisition of a third or additional property or if the expected rental income from the property enters into the calculation when proving income (in this condition, the impact on the market will be limited by the fact that realised income should enter into the assessment of income, which in the case of expected rental probably needs to be evidenced by a future lease agreement).

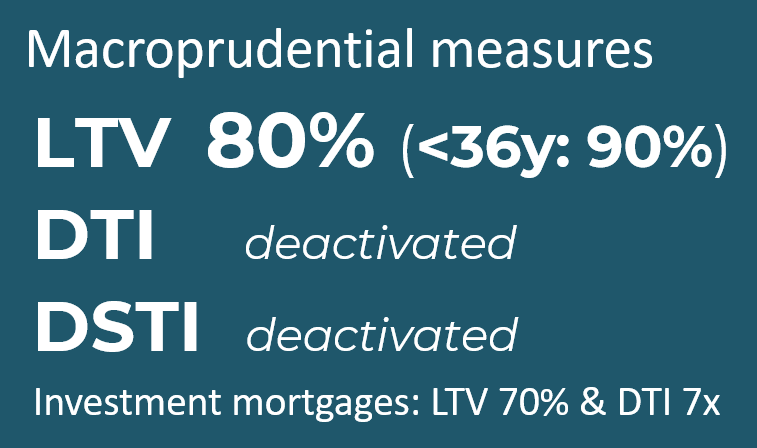

A stricter recommendation? LTVmax of 70% and DTImax of 7 times. The mortgage to property value ratio, i.e. LTV, should not exceed 70% from 1 April 2026 (compared to the general 80% limit or 90% for applicants under 36) and the debt to annual income (DTI) ratio should be no more than 7 times compared to the current recommended 8 times.

Potential impact on the market? A mechanical calculation suggests a potential impact of between CZK 2.1-2.5 billion per month or around CZK 26-31 billion per year. Investment mortgages defined in this way and breaching recommended LTV and DTI ratios, according to the CNB presentation, accounted for around 9% of new mortgage originations, but the CNB's Financial Stability Report Summary indicates an impact of around 7.5%, which, I estimate, reflects the usual 15% overshoot of macroprudential recommendations (such as in the case of the 8x DTI in Q2-2025).

- In the last three months, according to CBA Hypomonitor, actual new mortgage originations (excluding refinances) were 28.7 billion per month (seasonally adjusted) and this year's ten-month average was 26 billion (p.o.). Thus, the full impact could be CZK 2.3-2.6bn per month or around CZK 2-2.2bn at 15% over recommendation or adjustment. Potentially maintaining the recent annualized momentum in new mortgage volume implies a 345 billion new mortgage volume for next year. Thus, fully projecting the 9% impact of these measures, we are talking more like 314 billion in volume, or a 31 billion impact, or a 26 billion impact at 15% overshoot of recommendations or adjustment (or in the range of 20-23 billion over the nine months from April to December 2026).

For a better estimate, it would be useful to know other characteristics of the so-called investment mortgages - their number, average amount, but also the number of applicants for investment mortgages (on average 1.58 people apply for a new mortgage) and their average declared income. In addition, the new recommendation may also lead some applicants to submit additional income, which they had previously avoided due to less bureaucracy.

In the words of board member Jakub Seidler, the new recommendations are already expected boundaries for the banks for the coming months, as he does not expect banks to use the next four months to maximize the granting of investment mortgages. Rather, the next four months should be used to complete the loans currently under consideration and to adjust to the new conditions.

For the record, one Board member voted against tightening the conditions for investment property mortgages (details and reasons will be available on Monday, December 15).

Although the recommended DSTI of 40% is exceeded in more than half of new mortgage originations, the higher DSTI ratio applies to high-income households, which the CNB believes does not increase systemic risks to the mortgage market and therefore does not warrant activation of across-the-board macroprudential measures. Thus, the CNB has not reverted to an across-the-board reactivation of the limits on the DSTI and DTI ratios, which it gradually "turned off" during 2023.

Source: CNB, CBA

Source: CNB, CBA

Other macroprudential measures in the form of capital requirements remain essentially unchanged:

1) countercyclical capital buffer (CyCB) at 1.25% (risk of increase if the Czech financial cycle does not stabilise; see slide 14 in the CNB presentation; we will see on 9 December how the CNB's loss estimates behind the CyCB setting are evolving - see chart below);

2) one bank will drop out of the O-SIIB capital requirement, which will make it applicable to six systemically important banks (4.25% asset share threshold) in the range of 0.5%-2.5% of RWA next year (see slide 22 in the CNB presentation)

3) the systemic risk buffer (SyRB) remains at 0.5% (we will see later whether the CNB discussed the sectoral systemic risk buffer sSyRB, which according to the ESRB is applied in 10 of the 21 countries in Europe that apply SyRB).

Source: CNB, CBA