Banking sector

Basic indicators on the development of the domestic banking sector in the Czech Republic from official Czech National Bank statistics and compulsorily published data from individual banks

CZK billion and % of GDP, annual figures

Q1 / 2026

% of assets and capital

Q1 / 2026

CZK billion and % of profit, annual total

Q1 / 2026

The countercyclical capital buffer should rise to 1.5% from July 2027, which will increase banks' total capital requirements to around 17% next year, in response to continued growth in lending to households and firms and lower perceived risks in the banking sector. Again, we are also seeing stronger wage growth outpacing productivity. In the case of rising investment credit, however, this is a dilemma for macroprudential policy. In addition to the financial cycle, the results of stress tests, including concerns about the interconnectedness of the banking and government sectors, are likely to have factored into the decision. It leaves mortgage rules unchanged.

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Comment by Jaromír Šindel, Chief Economist of the CBA: Mortgage rates are significantly determined by the movement of market interest rates. However, structural factors in the banking market are also important. The CNB's investigation of credit conditions in our analysis helps to explain what factors influence the difference between mortgage and market interest rates deviating from its normal level. The CBA analysis shows that a combination of stronger demand and competition among banks plays a key role. It is the latter that can lead to more favourable rates for clients without undermining market stability. The difference between mortgage rates and market rates that we have been monitoring is therefore mainly dampened by stronger demand, but in an environment of growing competition, which is key. Banks' profitability also plays a role, acting as a corrective mechanism to maintain competitive interest rate spreads but also market stability.

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

The current growth in credit activity is mainly driven by mortgage lending, on which the countercyclical buffer has a more limited impact. Although there was also a recovery in lending activity to non-financial corporations last year, these are still rather early signs of recovery and the economy needs stronger investment activity outside construction. These reasons are probably behind the central bank's decision to leave the countercyclical buffer in banks' capital unchanged at 1.25%, but with the caveat of a growing likelihood of a future increase.

Commentary of the Czech Banking Association on the development of deposits, loans and non-performing loans for January 2026 according to CNB statistics

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Comment by Jaromír Šindel, Chief Economist of the CBA: The central bank did not surprise by unanimously leaving interest rates unchanged, i.e. with the two-week repo rate at 3.50%, for the fifth meeting in a row after a 25bp cut in May. Although the Board did not change its view of the risks and uncertainties surrounding the CNB's November forecast, it did assess the risks to inflation as balanced, given the risks in financial markets and the removal of the renewable energy levy, following November's upside assessment.

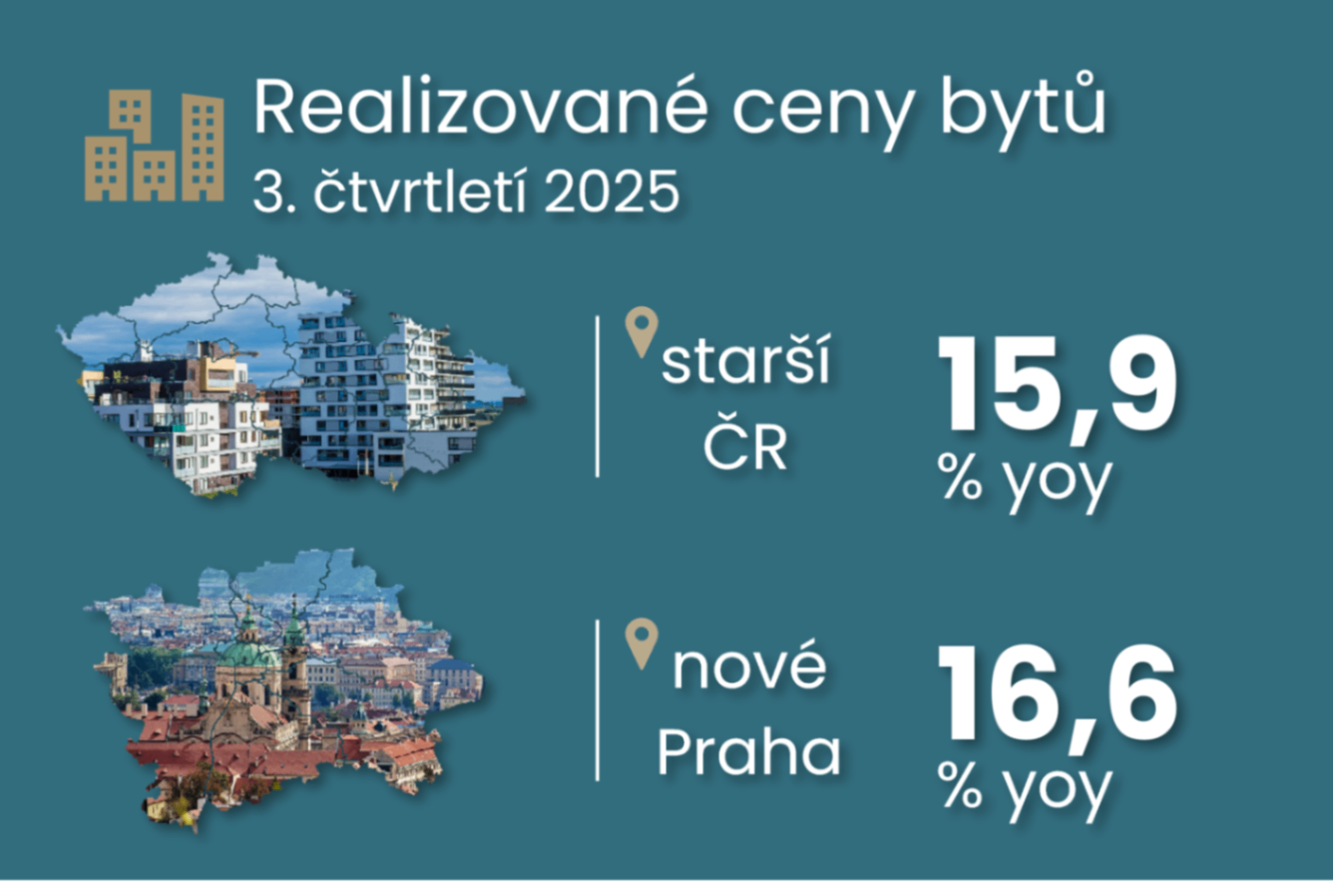

Comment by Jaromír Šindel, Chief Economist of the CBA: According to the Czech Statistical Office, realised prices of older flats in the Czech Republic rose by 3.7% quarter-on-quarter in the third quarter, which exceeds income growth for the seventh quarter already and maintains the too brisk annual pace of property prices at around 16%. Higher property prices are also making their way into the CNB's macroprudential capital policy settings, with discussion over the (arguably unscary) possible introduction of a sectoral systemic buffer, as well as less intuitive discussions over the role of investment activity by non-financial corporates in setting the countercyclical capital buffer.

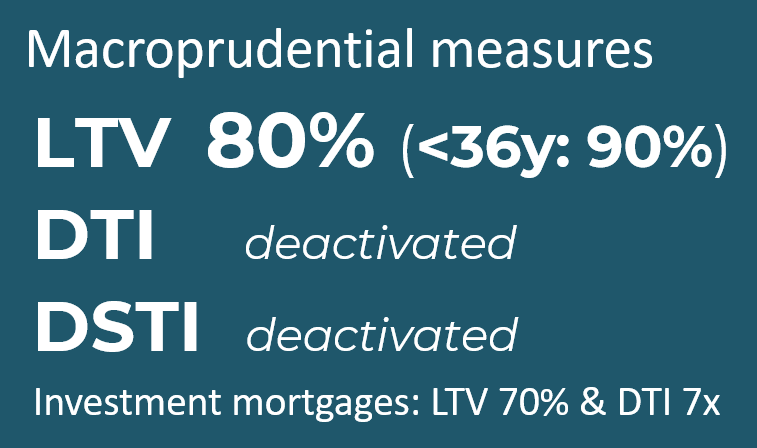

Comment by Jaromír Šindel, Chief Economist of the CBA: The Central Bank, through stricter requirements in the form of recommendations for investment mortgages, has decided to make a modest effort to correct mortgage demand on the real estate market, which remains very tight in terms of prices, mainly due to the supply side - see the drop in building permits.

Comment by Jaromír Šindel, Chief Economist of the CBA: The CNB is waiting for a new impulse. The CNB is waiting for the new government to announce its plans, both from the data and from future analysis of the new government's upcoming plans. The CNB's own outlook, with more moderate consumer price growth at the end of the year and a stronger economy in real terms in Q3, opens up the possibility of more hawkish communication in the rest of the year. But I believe the CNB will wait to reassess its communication until the contours of the new government's policy are clearer.

Comment by Jaromír Šindel, Chief Economist at the CBA: While the CNB unsurprisingly left interest rates unchanged with the two-week repo rate at 3.5%, the Board's statement on the monetary policy settings, however, was more surprising in its less hawkish tone, leaving open all possibilities for future monetary policy settings.

Commentary by Jaromír Šindel, Chief Economist of the CBA: Higher-than-expected wage growth will be the main, but not the only, reason for keeping the interest rate at 3.5% at the CNB's September meeting and for the intensification of the hawkish tone in the communication. The latter may indeed indicate a further upward movement in the interest rate, but rather in an unspecified distant horizon. A stronger koruna or tighter monetary policy through the longer end of the yield curve is unlikely to lead the CNB to a dovish mindset.

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Economic commentary by Jaromir Šindel, Chief Economist of the CBA (adjusted for published data on core inflation from the CNB and registered unemployment data, 18:00 8 August)

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

The CNB Bank Board left interest rates unchanged in March.

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

Commentary by Miroslav Zámečník, Chief Advisor of the Czech Banking Association

Economic commentary by Jaromír Šindel, Chief Economist of the CBA

Economic commentary by Jakub Seidler, Chief Economist of the CBA

Economic commentary by Jakub Seidler, Chief Economist of the CBA

Economic commentary by Jakub Seidler, Chief Economist of the CBA

Economic commentary by Jakub Seidler, Chief Economist of the CBA

Economic commentary by Jakub Seidler, Chief Economist of the CBA