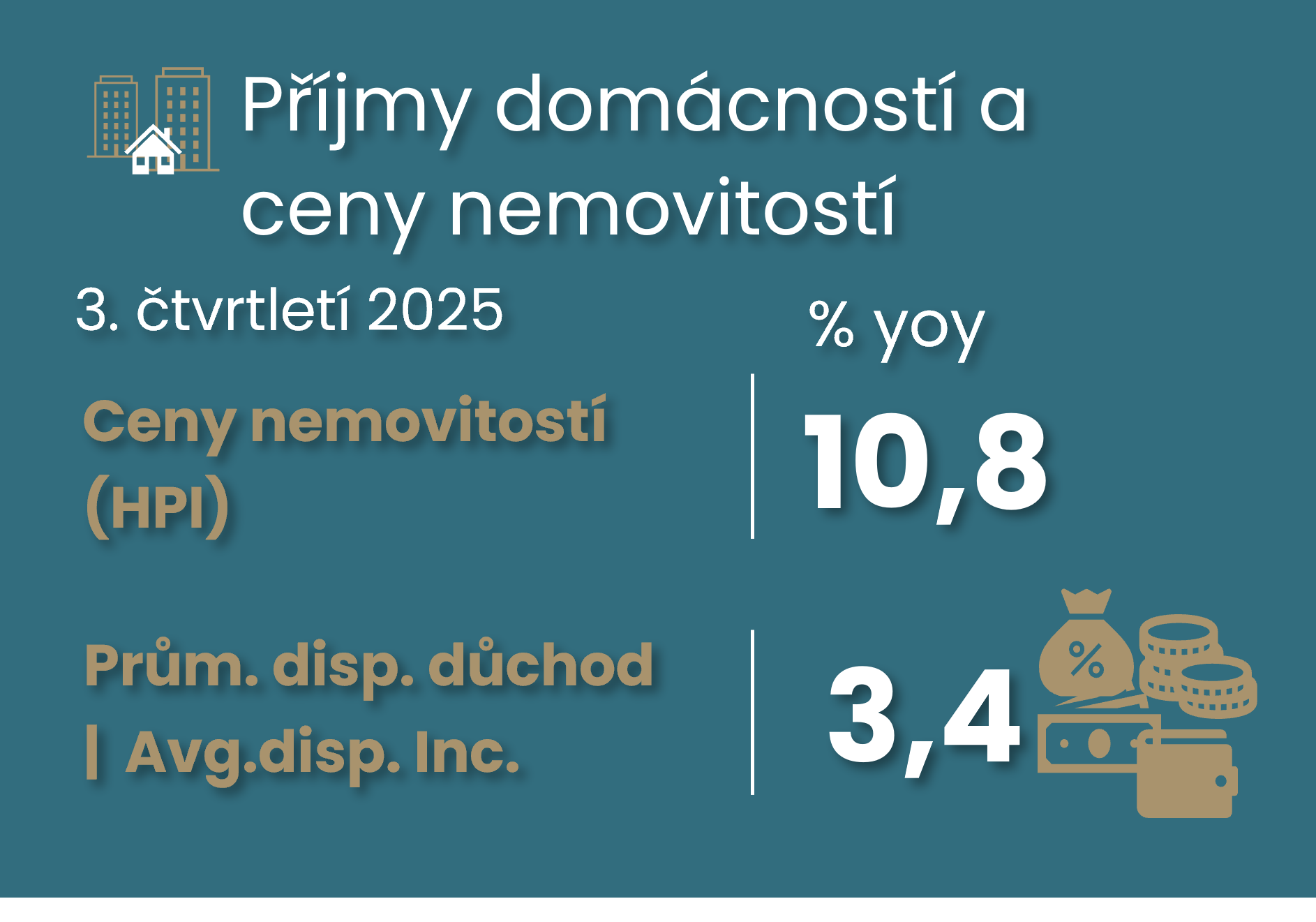

House prices have maintained 10% momentum, which is not the case for disposable income

Comment by Jaromír Šindel, Chief Economist of the CBA: Even the third quarter of 2025 did not bring a significant recovery in household disposable income. Despite this, the household savings rate has been abnormally high for almost six years. In Q3, it was 18.4%. Weaker quarter-on-quarter growth in disposable income has not kept pace with house prices for six quarters in a row. On a year-over-year basis, we are comparing 3.4% growth in disposable income vs. a 10.8% increase in home purchase prices including land (HPI).

House price growth slowed slightly in the third quarter of 2025, but still maintained strong double-digit growth. The House Price Index (HPI), which includes land and houses, rose 2.5% quarter-on-quarter in the third quarter. Although the pace of growth slowed after 3.1% in the second quarter, prices accelerated slightly to 10.8% y/y. However, this is still below the pace of realized home prices of around 16% in the third quarter. A year ago, house price growth was 6.1% year-on-year and realised house prices were rising at around 10%.

Neither housing supply prices nor average mortgage rates in the fourth quarter suggest an early turnaround. Although house price supply growth slowed to 2.4% in the final quarter of 2025 from 3.7% in the third quarter and below the average 4.2% increase in the previous four quarters, the pace remains close to the average 2.5% pace of the previous five to ten years, when the annual rate was around 9-10%. Also, if we look at the relationship between house price growth and average mortgage size (see Chart 10), the 14% year-on-year increase in average mortgage size does not suggest a significant slowdown in house price growth.

Transaction prices for October to November suggest slowing price pressure from first sales of new builds. According to data from Flat Zone, the average November transaction price of new flats on first sale in the Czech Republic reached CZK 142 thousand. CZK/m2. Monthly data for October and November so far indicate a more modest quarter-on-quarter increase of 1% in the average transaction price of new-builds in Q4 2025, following an average 2.4% increase in the previous four quarters. This would imply a slight slowdown in year-on-year growth to 9% after 9.9% in the previous quarter.

The Czech household savings rate remains abnormally high, at 18.4% in Q3 2025, reflecting both softer growth in household consumption (0.3% q-o-q in real terms) and slower growth in disposable income, both in absolute (0.6% q-o-q in nominal terms) and relative terms (0.5%). Growth in disposable income of households (i.e. not just those in employment) slowed in Q3 2025 due to slower growth in compensation of employees (although average earnings from employment grew faster, partly reflecting the more moderate growth in median average wages in Q3). There is also a noticeable impact of lower property income, a typical phenomenon in the current phase of the central bank interest rate cycle. Following the negative impact of fiscal consolidation in previous quarters, net taxes have played a neutral role in household disposable income dynamics (see Figures 5-8).

The dynamics in 2026?

According to our forecast, this year should bring slower but still solid average wage growth of around 5.6%, or less, as the abolition of the POZE will lead to slower-than-expected 2.2% annual consumer price growth. While this should slow real average wage growth to around 3.5%, the change in fiscal policy should support growth in disposable income, which should no longer be so significantly undercutting wage growth.

With mortgage activity still strong, demand for property will remain strong at least in early 2026. Later, it is likely to be partly dampened by the CNB's stricter recommendations on so-called investment mortgages and the stabilisation of mortgage interest rates. However, the supply side, given the weaker building permit statistics - see charts below - will not bring relief to the property market.

The new government's planned steps in the housing sector - including the speeding up of building procedures - may bring some relief on both the supply and demand sides (e.g. through a dampening of the effect of higher demand due to fears of shortages, the so-called FOMO). However, with capacity constraints, both on the labour and building material side, it is probably not possible to expect rapid and significantly noticeable impacts. In addition, the government plans to support the demand side later on by subsidising mortgage rates for young families and key occupations (see selected figures in the third and fourth paragraphs here) or by subsidised down payment loans for first home purchases by young families.

Below are four key charts, followed by charts on disposable income and on house prices and planning permissions.

The savings rate of Czech households remains abnormally high, at 18.4% in Q3 205, reflecting both a more moderate growth in household consumption (0.3% quarter-on-quarter in real terms) ...

... so slower growth in disposable income - 0.6% q-o-q in nominal terms.

House price growth (blue columns), especially in the last five to ten years, has outpaced growth in incomes (orange) and rents (green)

Disposable income

While we observe a recovery in real average wages from 2023 onwards, disposable income grows more slowly, albeit after a small fall.

Growth in disposable income in the third quarter was affected by slower growth in workers' compensation and lower property income ...

... which also reflects a decline in household interest income, a common phenomenon at this stage of the central bank's interest rate cycle.

While the impact of fiscal redistribution (see net taxes excluding social transfers in kind) became more neutral after the negative impact of fiscal consolidation from 2023-2024 and 2024-2025.

Real estate prices

Overview of available property and apartment prices: solid growth of Czech property prices continued during the second half of 2025

The average new mortgage amount does not indicate room for a significantly slower rate of house price growth

According to CSO statistics, prices for home purchases (older ones, including land and new ones, but those are basically only in Prague - for the rest of the country, see our stats on the CBA Monitor from Flat Zone) have risen 10.8% year-over-year in the last four quarters, jumping 13.5% in the last three years and 60.2% in the last five years. In the last decade, it's up 147%, or 162% in the last 15 years.

Supply prices slowed quarter-on-quarter to 2.4% in the last quarter of 2025, the lowest increase since mid-2024. However, the pace remains above the long-term average of 1.8%.

According to data from Flat Zone, the average transaction price of new flats on first sale in the Czech Republic reached CZK 141.6 thousand in November. CZK/m2.