Comment by the Czech Bar Association

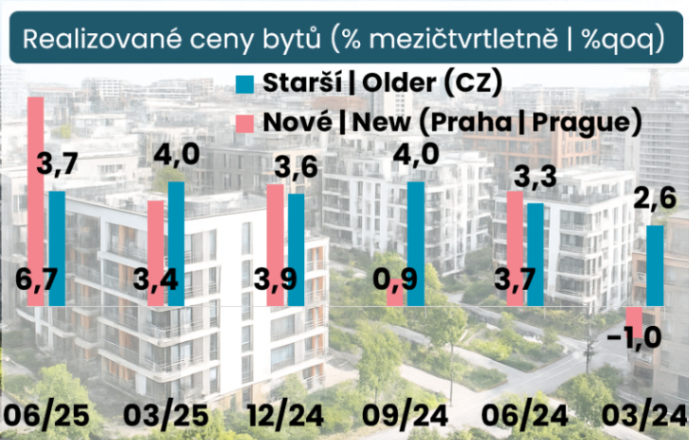

According to data from the Czech Statistical Office, asking prices for new and existing apartments in the Czech Republic rose by 2.7% in the first quarter of 2026, following a 2.4% increase in the previous quarter.This growth rate was thus close to the average quarterly growth of 2.4% recorded since the end of 2019. In Prague, these prices rose by 2.4% quarter-on-quarter, following a 2.2% increase; compared to the long-term average of 2.1%.

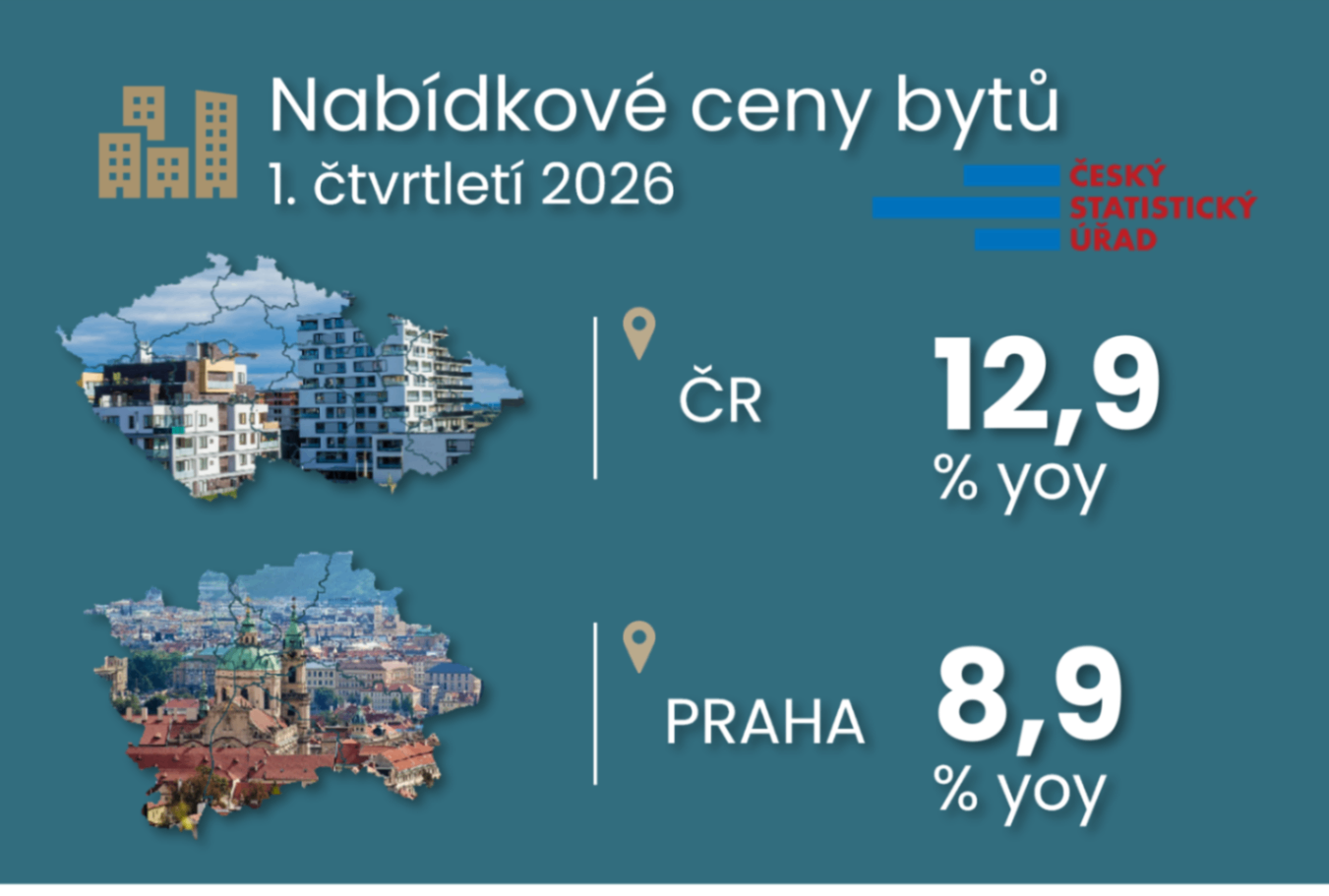

Year-on-year, prices in the Czech Republic rose by 12.9% in Q1 2026,2026, reaching 1.8 times the pre-pandemic level in the fourth quarter of 2019 and 2.9 times the level at the end of 2013. These ratios reached 1.7 and 2.8 in Prague, while in the rest of the country they were 2 and 3.

In 2025, the Czech Republic saw an average year-over-year change in asking prices for new and older apartments of 16.8% (up from 5.1% the previous year), of which prices in Prague rose by 15.9% (following 5.4%).

Trends in Real Estate Asking Prices

(% year-over-year)

Source of primary data

Czech Statistical OfficeCategory

Real Estate PricesData frequency

quarterlyNote

Average asking prices for new and renovated apartments, as well as older apartments.