Comment by the Czech Bar Association

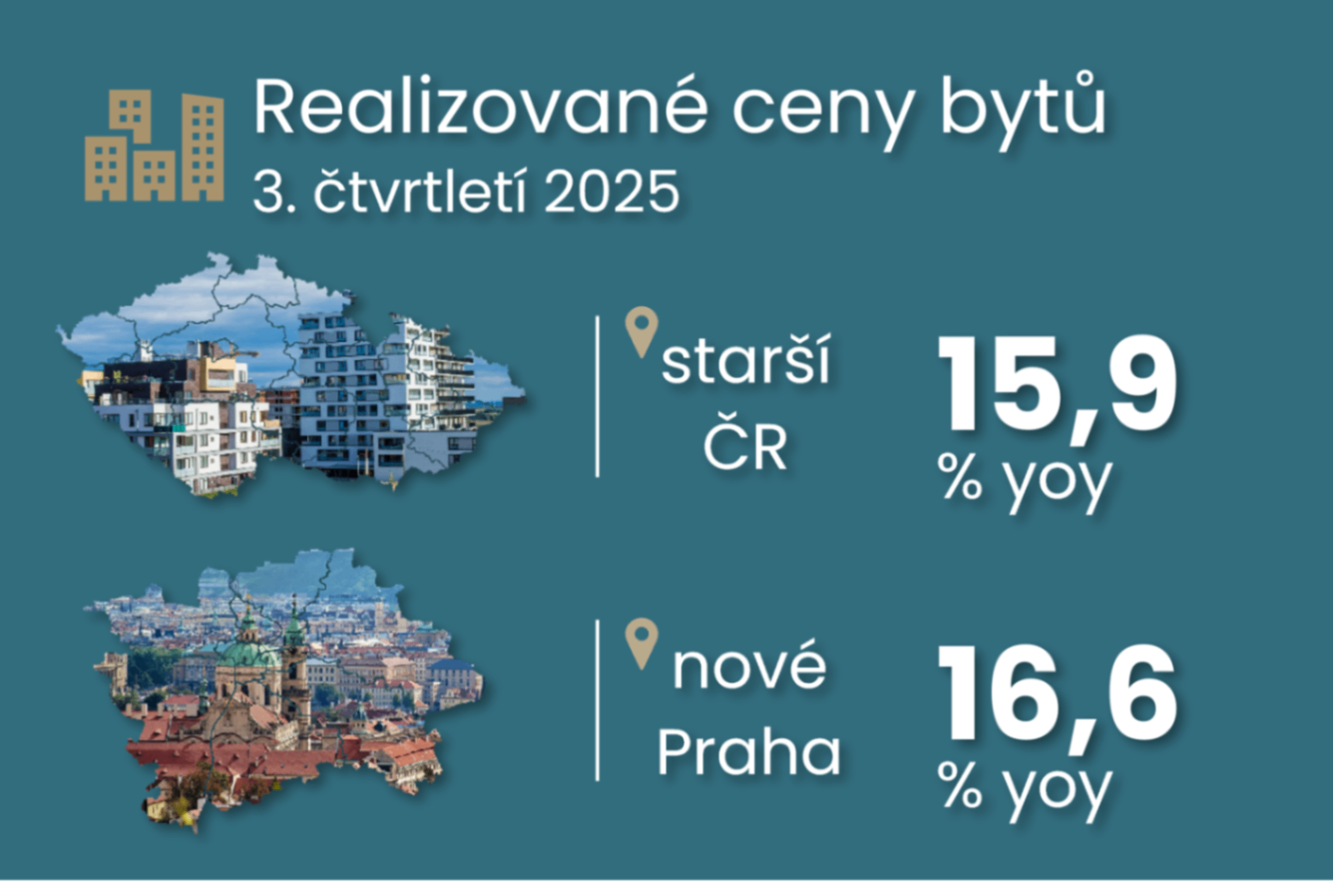

Data from Flat Zone for March 2026 show that the average transaction price of new apartments in Prague sold for the first time rose to CZK 179,000 in the first quarter of 2026, a 3% increase compared to the previous quarter. Their year-over-year growth then accelerated to 12% following a previous 12% increase. In 2025, transaction prices for these new Prague apartments in primary sales rose by 12.6% year-over-year. Compared to the beginning of Flat Zone’s time series—that is, compared to the first quarter of 2023—prices for these Prague apartments in first-time sales in the first quarter of 2026 were 14.4% higher, which is approximately CZK 22,000 per square meter in absolute terms.

Methodologically different data from the Czech Statistical Office (ČSÚ) show a 21% increase in Prague’s new apartment prices at first sale compared to the first quarter of 2023.

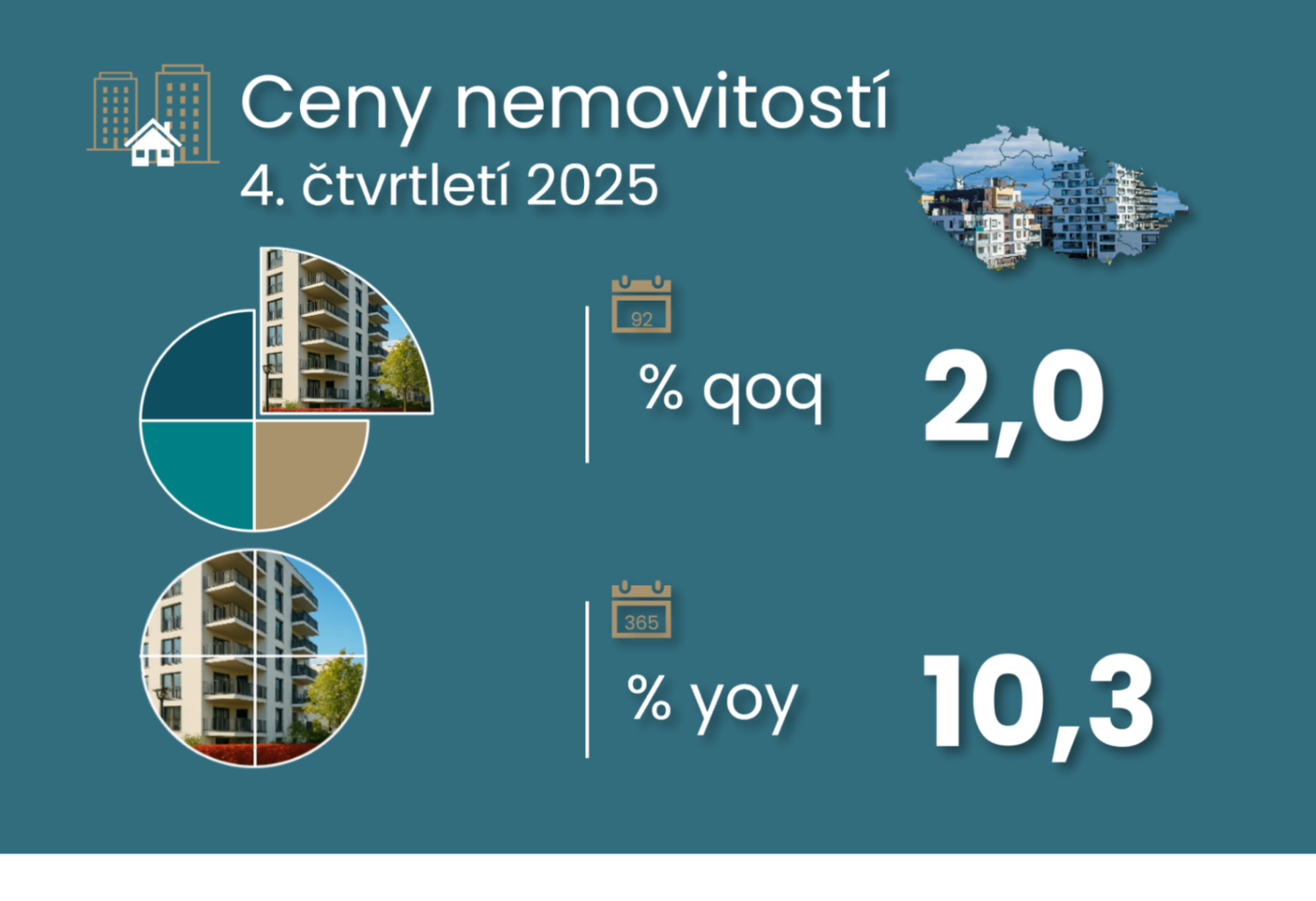

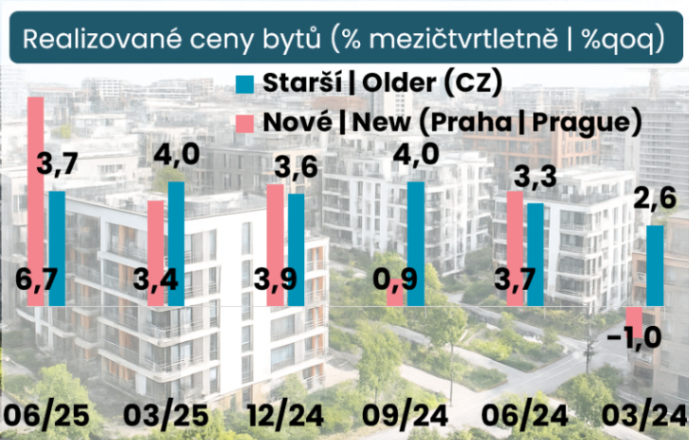

According to CZSO data, realized prices for new first-time sales in Prague rose by 1.3% quarter-on-quarter in the first quarter of 2026, following a previous increase of 0.9%. This growth rate thus fell short of the average quarterly growth of 2.1% recorded since the end of 2019. This resulted in a year-over-year increase of 11.1% in the realized prices of new apartments in Prague during the first quarter of 2026, while the realized prices of older apartments rose by 11.5%.

According to CZSO data, prices of new apartments reached 1.7 times their pre-pandemic levels at the end of 2019 and 2.8 times their levels at the end of 2013. These multiples for realized prices of older apartments in Prague reached 1.8 and 2.9.

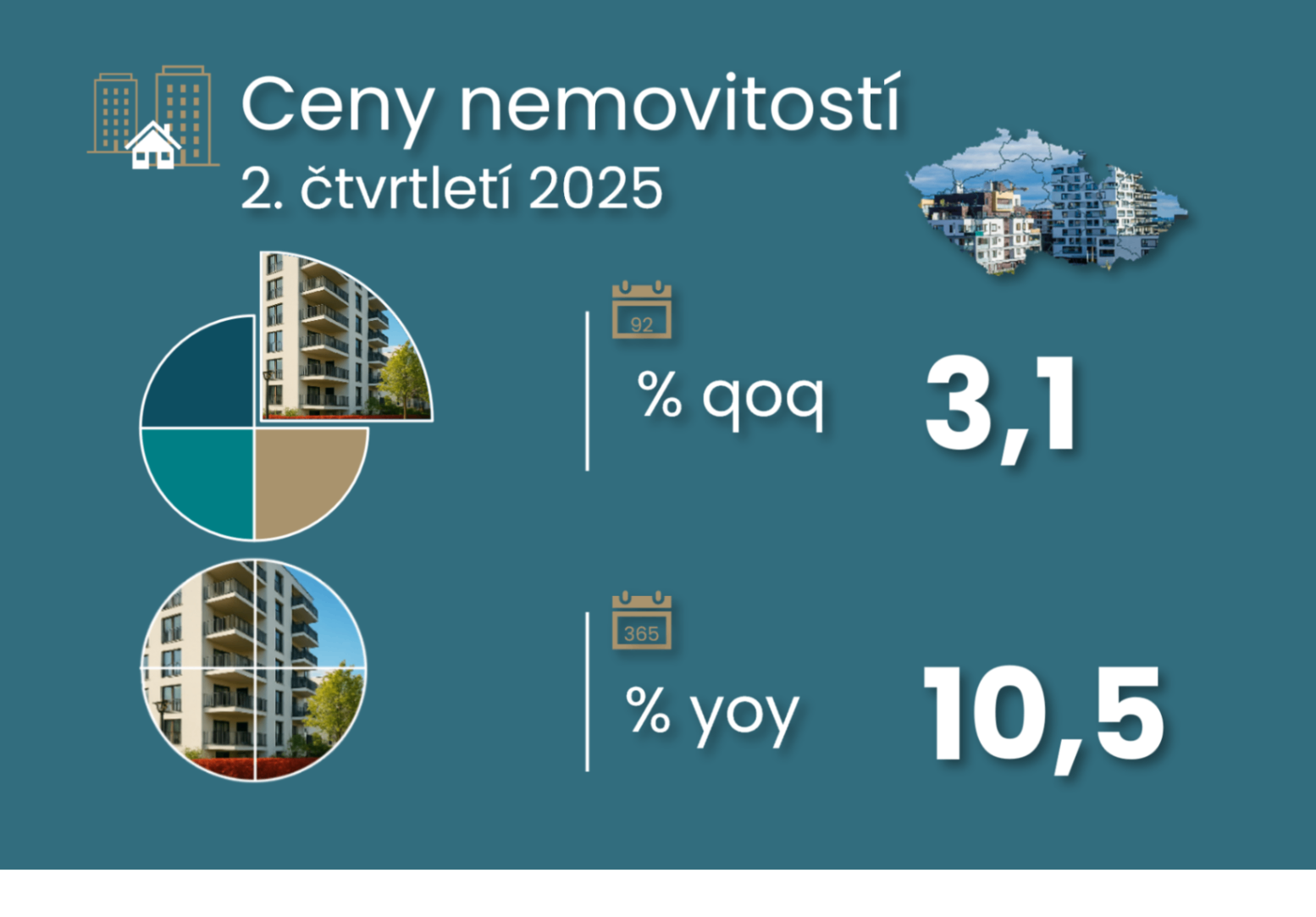

CZSO data show that in 2025, the average year-over-year change in realized prices of new apartments through first-time sales in Prague was 14.5% (up from 1.8% the previous year) and 14.1% for the realized prices of older apartments (following 8.4%).

Changes in actual apartment prices in Prague, % yoy

(%, year-over-year)

Source of primary data

Czech Statistical Office, Flat ZoneCategory

Real Estate PricesData frequency

quarterlyNote

Actual prices. New apartments – these are initial sales.In the case of Flat Zone data, these are transaction prices for initial sales of new apartments in the developer-client relationship at the time of sale.

In the case of CZSO data, the figure for Prague is a weighted average of partial results.

The data methodology therefore differs, which causes differences in the dynamics and levels of the time series, especially in the short term.