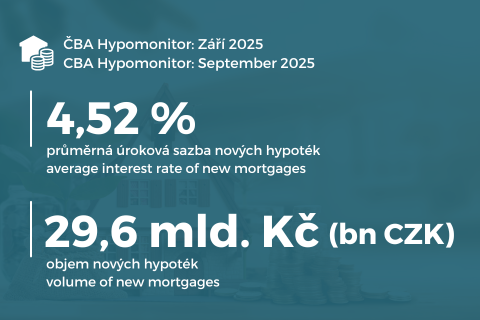

CBA Hypomonitor: Indian summer of strong mortgages at a stable rate of 4.52%

Table 1: Summary of mortgage origination volumes and average interest rates for September 2025 and so far this year

monthly values | values since the beginning of the year | ||||||

Volume | Number | Rate | Volume | Number | Rate | ||

Total | 37,6 | 8 952 | 4,52 | 292,9 | 72 941 | 4,60 | |

New loans | 29,6 | 6 795 | 4,52 | 235,1 | 56 532 | 4,61 | |

of which: | |||||||

for purchase | 23,6 | 5 348 | 4,51 | 187,8 | 44 290 | 4,60 | |

for construction | 4,1 | 959 | 4,50 | 35,5 | 8 756 | 4,57 | |

Other | 1,9 | 488 | 4,66 | 11,9 | 3 486 | 4,79 | |

Refinanced from another institution | 6,8 | 1 845 | 4,49 | 47,3 | 13 555 | 4,56 | |

Refinanced internally, increased | 1,2 | 312 | 4,54 | 10,5 | 2 854 | 4,57 | |

Source. | |||||||

Post-holiday return to strong mortgage volume after milder August correction

"September's figures confirmed that the strong summer activity in the mortgage market was no exception. The mortgage market remains very buoyant, with both the number and volume of new loans increasing.The average amount of a new mortgage exceeded CZK 4.3 million for the first time and its median is probably around CZK 3.4 million," notes Jaromír Šindel, chief economist at the Czech Banking Association.

Chart 1: New mortgages granted without refinancing

In September 2025, banks and building societies granted new mortgages worth CZK 29.6 billion, 14% more than in August. The seasonal adjustment suggests an improvement of more than 20% to CZK 31.3 billion.

The average mortgage rate stabilised at 4.52% in September

"The average interest rate on mortgages is basically unchanged. While swap rates fell slightly in early October, even in the face of lower-than-expected inflation, they are still near their highest levels in a year.Thus, we probably cannot expect a significant cheapening of mortgages," believes Petr Gapko, chief economist at Moneta banka.

Chart 2: Average mortgage rate - new business

The Septembermortgage rate stabilised at 4.52% with a year-on-year decline of less than half a percentage point.

"The September mortgage production figures show that the scope and conditions for further interest rate cuts are now limited and a further move lower cannot be counted on. On the other hand, prices of all types of real estate are rising steeply; according to our CSOB Housing Index, apartments, for example, jumped by as much as 13.8 per cent year-on-year in the second quarter.In this situation, it is therefore better for those interested in owning their own home not to hesitate and to take advantage of the still current property prices and mortgage loan conditions to secure financing for their desired flats or houses," says Martin Vašek, CEO of ČSOB Hypoteční banka.

Chart 3: Market long-term rates continued to rise in September, followed by a slight correction in early October in response to the post-election result and lower-than-expected September inflation

Chart 4: Average amount of actual new mortgages granted by purpose

The average mortgage amount returned to further growth after a short pause in August to CZK 4.35 million. The average mortgage is now 7% higher this year than a year ago.

Impact on the average monthly mortgage payment of around CZK 23.4 thousand

Table 2: Illustration of the average monthly mortgage payment by length of repayment and interest rate

Average size of a new mortgage in CZK: | 4 351 030 | ||||||

Average interest rate in %: | 2,0 | 3,0 | 4,0 | 4,52 | 5,0 | 6,0 | |

Monthly instalment: | |||||||

Mortgage maturity in years: | 15 | 28 000 | 30 050 | 32 180 | 33 330 | 34 410 | 36 720 |

20 | 22 010 | 24 130 | 26 370 | 27 580 | 28 710 | 31 170 | |

25 | 18 440 | 20 630 | 22 970 | 24 240 | 25 440 | 28 030 | |

26,8 | 17 510 | 19 720 | 22 090 | 23 380 | 24 600 | 27 250 | |

30 | 16 080 | 18 340 | 20 770 | 22 100 | 23 360 | 26 090 | |

Source: CBA [2] | |||||||

Note: the coloured column corresponds to the interest rate of the latest CBA Hypomonitor, other rates are illustrative; the coloured row corresponds to the average maturity of new mortgages according to CNB data; amounts are rounded to tens of crowns. | |||||||

[2] The table is available in an xls file attached on the CBA Hypomonitor website

Statistical annex

Chart 5: Illustrative comparison of the average monthly mortgage payment with a year ago, depending on the interest rate, mortgage size and maturity in years

In ayear-on-year comparison, the fall in the mortgage rate resulted in a saving of CZK 1 110 in the average monthly mortgage payment, but the increase in the average mortgage amount caused an increase of CZK 3 170.

Source: CBA. Note: amounts are rounded to tens of crowns.

Source: CBA. Note: amounts are rounded to tens of crowns.

Mortgage market in 2024: record growth of 83%

Chart 6: Annual volume, number and average amount of mortgages granted between 2020 and 2024

CBA publishes summary statistics for the entire banking market

- Purchase of real estate

- Property construction - including property renovation

- Other new arrangements - only new loans that are in no way related to the purchase or construction of the property, e.g. so-called American mortgages, settlement of a JVM, repayment of the purchase price, settlement of an inheritance share, settlement of a cooperative share, etc.

- an increase in the agreed amount

- changes such that the original loan has been refinanced/converted into a new loan within the reporting entity. This is a genuinely new contract and not, for example, just a new arrangement in the context of a refixation of an existing contract. Therefore, the volume of such loans in the CBA statistics is lower than 'other new arrangements' in the Czech National Bank statistics.