CBA Hypomonitor: Still strong October activity with mortgage rates below 4.5%

Table 1: Summary of mortgage origination volumes and average interest rates for October 2025 and so far this year

monthly values | year-to-date values | ||||||

Volume | Number | Rate | Volume | Number | Rate | ||

Total | 37,6 | 8 952 | 4,52 | 292,9 | 72 941 | 4,60 | |

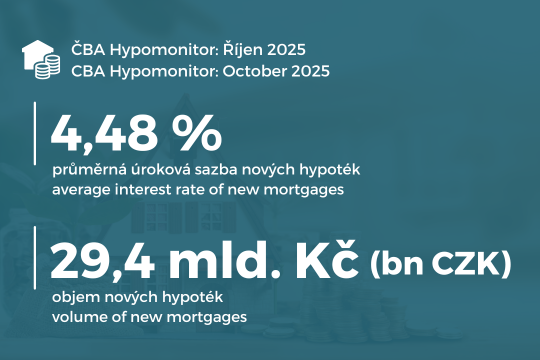

New loans | 29,6 | 6 795 | 4,52 | 235,1 | 56 532 | 4,61 | |

of which: | |||||||

for purchase | 23,6 | 5 348 | 4,51 | 187,8 | 44 290 | 4,60 | |

for construction | 4,1 | 959 | 4,50 | 35,5 | 8 756 | 4,57 | |

Other | 1,9 | 488 | 4,66 | 11,9 | 3 486 | 4,79 | |

Refinanced from another institution | 6,8 | 1 845 | 4,49 | 47,3 | 13 555 | 4,56 | |

Refinanced internally, increased | 1,2 | 312 | 4,54 | 10,5 | 2 854 | 4,57 | |

Source. | |||||||

"Despite the October correction, mortgage numbers remain very strong. The volume of newly granted mortgages has remained around CZK 29 billion in recent months. Numbers are also holding at higher levels and are likely to exceed last year by around a quarter this year, with higher house prices pushing the total volume of new lending up by more than a third.However, the mortgage market needs positive supply impulses - ones that would ease property prices and help bring market interest rates back to lower levels," says Jaromír Šindel, chief economist at the Czech Banking Association.

Strong summer mortgage activity continued in October

"Demand for mortgages is still rising. In October, we received a record number of applications this year, up by a third month-on-month. At the same time, we closed mortgages in record volume, helped by a slight increase in interest in refinancing loans. So much good news.The bad news is that interest rates are slowly starting to rise and if this trend continues, it will be unsustainable to keep mortgage loans at the current average rate of around 4.5%," says Milan Voldřich, product manager for home loans at Raiffeisenbank.

Chart 1: New mortgages granted without refinancing

Chart 2: Average amount of new mortgages actually granted by purpose

"Banks are currently addressing refixations of high volumes of a large part of clients with low interest rates. This means increased activity - they are trying to retain clients and offer them stability and fair terms.It is most advantageous for the client to communicate with his/her bank and in case of switching to a new bank to know the real savings when refinancing, including all fees," says Soňa Holíková, mBank's mortgage manager.

Average mortgage rate moved lower to 4.48% in October

Chart 3: Average mortgage rate - new business

Chart 4: Still higher inflation, stronger economic growth, but also the post-election result keep market long-term rates higher

The average size of actual new mortgage originations fell marginally to 4.34 million in October. CZK

Impact on the average monthly mortgage payment of around CZK 23.2 thousand

Table 2: Illustration of the average monthly mortgage payment by length of repayment and interest rate

Average size of a new mortgage in CZK: | 4 343 490 | ||||||

Average interest rate in %: | 2,0 | 3,0 | 4,0 | 4,48 | 5,0 | 6,0 | |

Monthly instalment: | |||||||

Mortgage maturity in years: | 15 | 27 950 | 30 000 | 32 130 | 33 190 | 34 350 | 36 650 |

20 | 21 970 | 24 090 | 26 320 | 27 440 | 28 670 | 31 120 | |

25 | 18 410 | 20 600 | 22 930 | 24 100 | 25 390 | 27 990 | |

26,8 | 17 480 | 19 690 | 22 050 | 23 250 | 24 560 | 27 200 | |

30 | 16 050 | 18 310 | 20 740 | 21 970 | 23 320 | 26 040 | |

Source: CBA [1] | |||||||

Note: the coloured column corresponds to the interest rate of the latest CBA Hypomonitor, other rates are illustrative; the coloured row corresponds to the average maturity of new mortgages according to CNB data; amounts are rounded to tens of crowns. | |||||||

Chart 5: Illustrative comparison of the average monthly mortgage payment with a year ago, depending on the interest rate, mortgage size and maturity in years

Statistical annex

Mortgage market in 2024: record growth of 83%

Chart 6: Annual volume, number and average amount of mortgages granted between 2020 and 2024

CBA publishes summary statistics for the entire banking market

- Purchase of real estate

- Property construction - including property renovation

- Other new arrangements - only new loans that are in no way related to the purchase or construction of the property, e.g. so-called American mortgages, settlement of a JVM, repayment of the purchase price, settlement of an inheritance share, settlement of a cooperative share, etc.

- an increase in the agreed amount

- changes such that the original loan has been refinanced/converted into a new loan within the reporting entity. This is a genuinely new contract and not, for example, just a new arrangement in the context of a refixation of an existing contract. Therefore, the volume of such loans in the CBA statistics is lower than 'other new arrangements' in the Czech National Bank statistics.