385

billion CZK

Momentum for This Year's Volume of New Mortgages

321

billion CZK

Volume of New Mortgages in 2025

Commentary by the Czech Bar Association

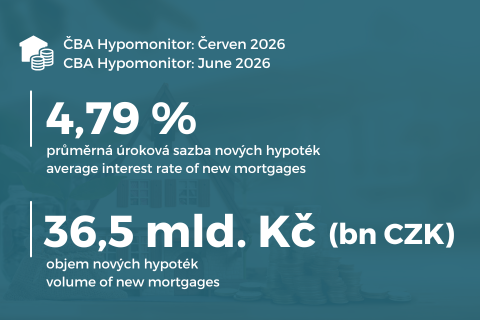

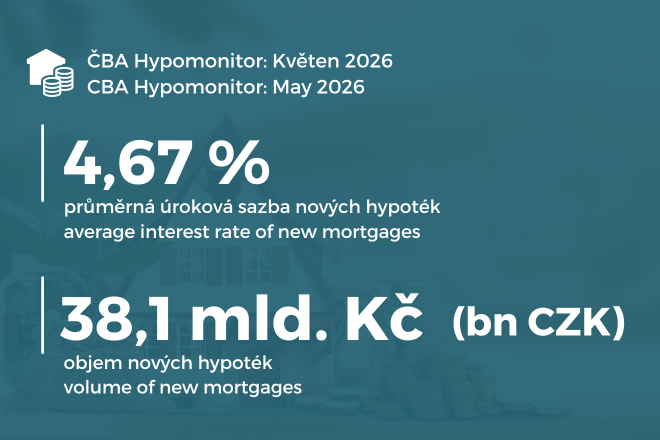

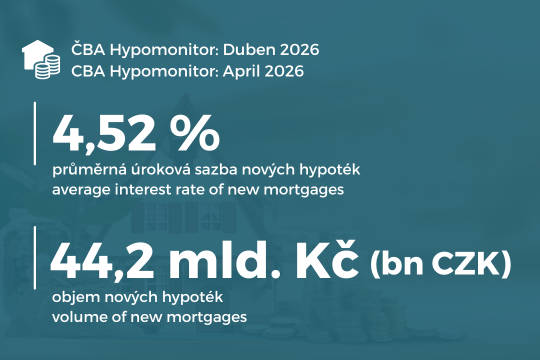

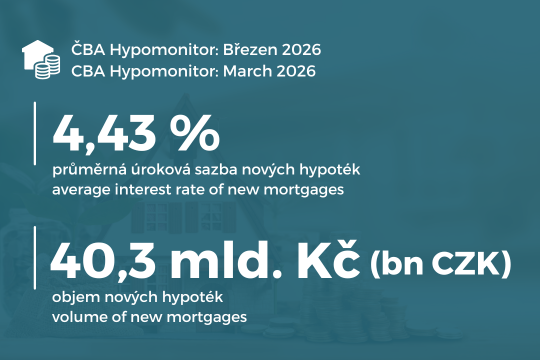

Given the trends in the mortgage market over the past three months—that is, from April through June—the volume of new mortgages (excluding refinancing) could reach CZK 385 billion in 2026, representing a 20% increase compared to last year. This current outlook roughly anticipates a 7% decline in the number of new mortgages compared to the second half of last year, which should increase the number of newly granted mortgages to 82,000—7.8% above last year’s 76,100 (the snapshot forecast itself points to 89,000 new mortgages this year). Hypomonitor’s historical data since 2020 shows the lowest annual volume at 124 billion crowns in 2023 and the highest volume at 379 billion in 2021.

Total Mortgage Volume for the Year

CBA Monitor

You can hide a data set by clicking on the data set name in the chart legend.

Source of Primary Data

ČBA HypomonitorCategory

ČBA HypomonitorData Frequency

annualNote

A more detailed breakdown of the data from the ČBA Hypomonitor is available in its monthly data supplement; see: https://www.cbamonitor.cz/publicistika/soubory/cba-hypomonitor-data