Volume of Newly Granted Mortgages, Including and Excluding Refinancing and Top-Ups

Volume of Newly Granted Mortgages, Including and Excluding Refinancing and Top-Ups

215.9

billion CZK; YTD

New This Year

294.1

billion CZK; YTD

New this year, with refinancing and an increase

Commentary by the Czech Bar Association

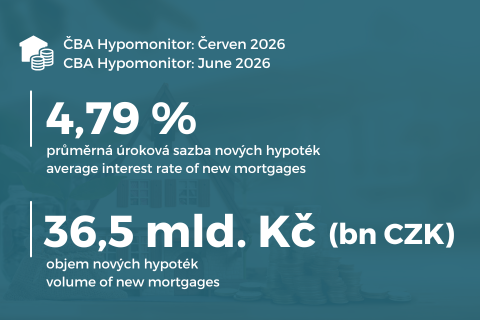

In June, banks and building societies actually granted new mortgage loans totaling 36.5 billion CZK. After seasonal adjustment, the June figures for new mortgages showed a decline (to approximately CZK 29.4 billion, compared with CZK 37.3 billion in the previous three months), reaching a level approximately 21% higher than in the first half of last year. Since the beginning of the year, the total has reached 216 billion crowns, which is 66 billion more than a year ago. The volume of refinanced and increased loans (either internally or from another institution) fell to 12.4 billion crowns in June. This is 75% more than the average of 7.1 billion refinanced last year and 216% higher than the 3.9 billion refinanced in 2024. The share of refinanced loans in the total volume of mortgages granted then fell to 25.4%, which is above last year’s average of 21%. Overall, banks and building societies reported new unconsolidated business in June in the form of new and refinanced mortgages totaling CZK 48.9 billion, which is 7% less than a month ago. Year-over-year, this figure rose by 32%. Their total volume so far this year has reached CZK 294 billion, representing a 59% increase compared to January through June of the previous year.

Volume of Newly Granted Mortgages, Including and Excluding Refinancing and Top-Ups

billion CZK

CBA Monitor

You can hide a data set by clicking on the data set name in the chart legend.

Source of Primary Data

ČBA Hypomonitor

Category

ČBA Hypomonitor

Data Frequency

monthly

Note

This includes new loans, both with and without refinanced and increased loans.

A more detailed breakdown of the data from the ČBA Hypomonitor is available in its monthly data supplement; see: https://www.cbamonitor.cz/publicistika/soubory/cba-hypomonitor-data

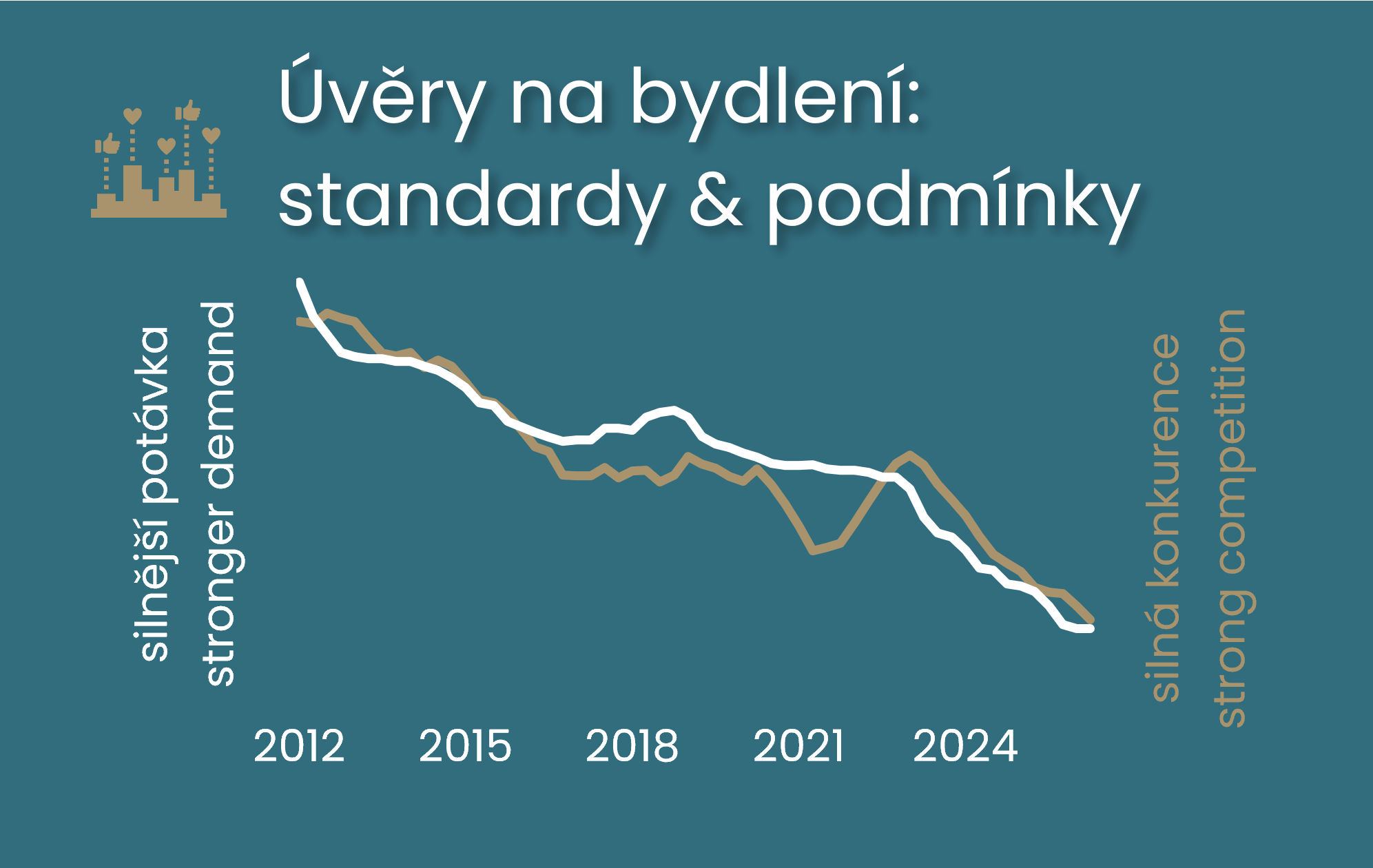

The CNB’s survey of banks’ lending conditions for the second quarter came as no surprise; the most significant change concerned housing loans. The central bank’s stricter criteria for investment mortgages tightened not only the banks’ lending requirements. In line with historical experience, this supported demand, likely temporarily. The impact on lending conditions was partially offset by lower bank margins and more favorable repayment terms. In an environment of continued strong competition, the stronger demand helped mitigate the impact of the spike in market interest rates on mortgage rates, which consequently rose more modestly. However, expectations of weaker demand for housing loans in the third quarter are changing this narrative. Surveys on consumer and business loans are also likely to keep the CNB’s outlook on the hawkish side.

Jaromír Šindel

17. 07. 2026

The average interest rate on new mortgages rose to 4.79%, while the average mortgage amount fell back below 4.7 million crowns. Banks and building societies issued new mortgages (excluding refinancing) totaling 36.5 billion crowns. After months of exceptionally strong mortgage activity, June saw a clear return to the robust normal levels seen in the second half of last year. In the first half of the year, the volume of new mortgages reached 216 billion crowns, which is 66 billion more than last year. Higher market interest rates and expensive real estate remain the main obstacles.

Jaromír Šindel

12. 06. 2026

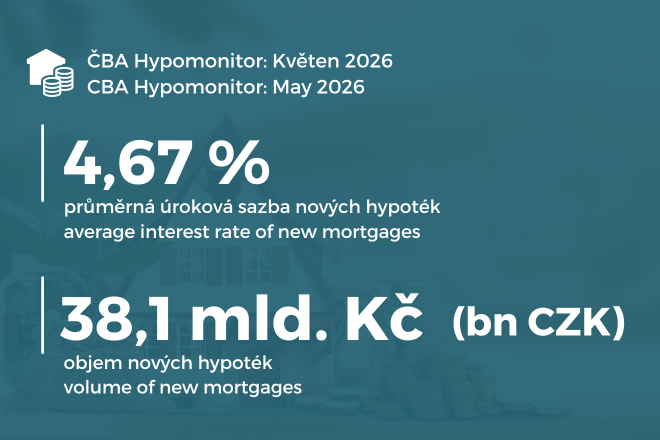

In May 2026, banks and building societies actually issued new mortgages (excluding refinancing) totaling CZK 38.1 billion.

Jaromír Šindel

04. 06. 2026

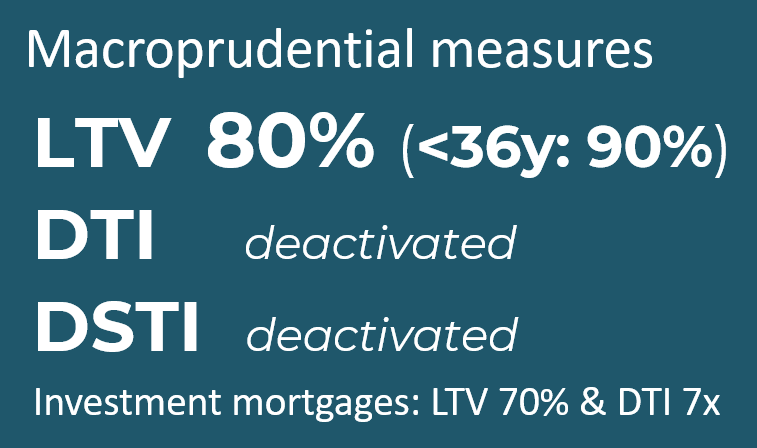

The countercyclical capital buffer should rise to 1.5% from July 2027, which will increase banks' total capital requirements to around 17% next year, in response to continued growth in lending to households and firms and lower perceived risks in the banking sector. Again, we are also seeing stronger wage growth outpacing productivity. In the case of rising investment credit, however, this is a dilemma for macroprudential policy. In addition to the financial cycle, the results of stress tests, including concerns about the interconnectedness of the banking and government sectors, are likely to have factored into the decision. It leaves mortgage rules unchanged.

Jaromír Šindel

18. 05. 2026

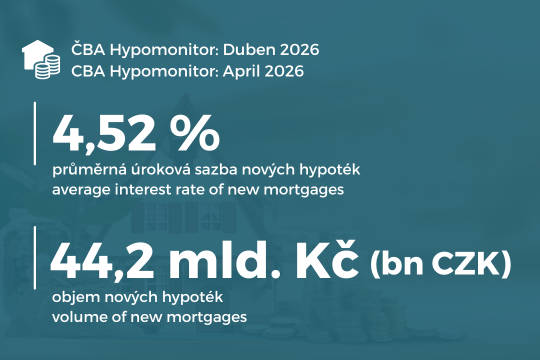

Average mortgage rate rises to 4.52%

Jaromír Šindel

13. 05. 2026

This year is bringing a strong wave of expiring mortgage rate fixations, while the shorter fixation periods agreed in recent years will further increase these volumes in the years ahead. Building on the central bank’s latest estimate that mortgage fixations worth an average of CZK 534 billion per year will expire between 2026 and 2028, we present alternative interest-rate shock scenarios depending on the path of mortgage rates. In 2027–2028, the negative interest-rate shock is expected to ease to 0.1–0.6 percentage points, down from 1.1–1.4 percentage points this year. However, we also outline a more adverse scenario involving a stronger interest-rate shock. This year, the negative interest-rate shock affecting expiring mortgage fixations from the low-rate period will amount to roughly 3.5% of the average household income of mortgage applicants, although across all households the average impact will be about half that level. In both cases, the expected real growth in wages and salaries should be sufficient to offset the shock.

Jaromír Šindel

16. 04. 2026

The average amount of a new mortgage exceeded CZK 4.8 million

Jaromír Šindel

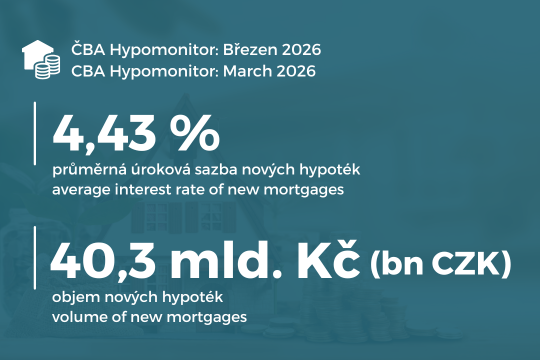

13. 03. 2026

February ranked among the five strongest mortgage months ever in terms of volume in billions of crowns, but also with a continued strong number of new mortgage originations.

27. 11. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: The Central Bank, through stricter requirements in the form of recommendations for investment mortgages, has decided to make a modest effort to correct mortgage demand on the real estate market, which remains very tight in terms of prices, mainly due to the supply side - see the drop in building permits.

16. 05. 2025

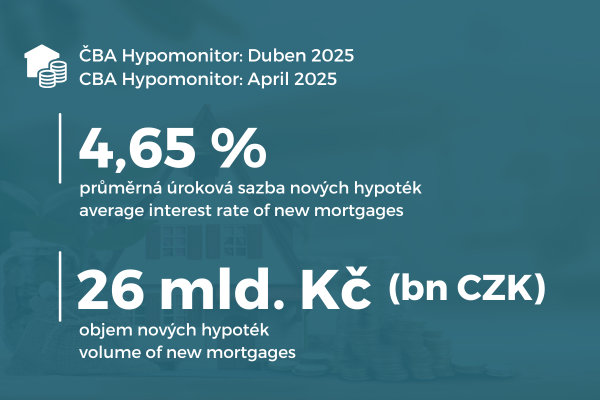

Despite the slight correction, April continued to see strong volumes of new mortgages supported by another slight decline in the average mortgage rate to 4.65%.

14. 04. 2025

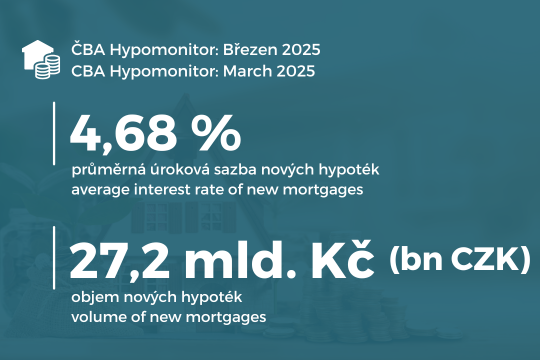

March continued to see strong new mortgage volumes supported by another slight fall in the average rate to 4.68%