Industrial production rose by 1.4% m/m in April on a seasonally adjusted basis. This resulted in stronger growth of 1.5% y/y, below the annualized growth of 11.6% over the past three months (which would be the future twelve-month annualized growth if the month-on-month momentum of the past three months is maintained). Construction output then fell by 1% m/m. Because of this, we see it growing at a stronger 7.9% y/y, below the annualized growth of 21.8%.Retail sales excluding autos fell by 0.9% m/m in April on a seasonally adjusted basis, while sales in the core segment (excluding food, fuel and autos) rose by 0.3% m/m on a seasonally adjusted basis. This resulted in a more modest 2.2% y/y growth in retail sales, above the annualized growth of 1.7%. Year-over-year growth in core sales strengthened to 5.4%, above annualized growth of 4.5%.Services sales (both consumer and business) fell 0% m-o-m in April on a seasonally adjusted basis. As a result, we observe them growing at a more moderate 2.3% y/y, which is below the annualized growth of 3.4%. This available data shows a level of industrial production 3.9% above the January-February 2020 pre-forecast level. Other sectors show the following differences to the pre-forecast period: 3.3% for retail sales excluding autos (10.5% for its core segment), 8.8% for services sales and 10.9% for construction production.

Post-Covid revival of economic activity

(3mma index against January-February 2020)

CBA Monitor

You can hide a data set by clicking on the data set name in the chart legend.

Source of primary data

CSO

Category

Economics

Data frequency

Monthly

Note

The index is in the form of a 3-month average. Data are in constant prices, adjusted for calendar and seasonal effects. Core retail trade corresponds to "retail trade for non-food goods", i.e. retail trade excluding cars, food and fuel.

April's monthly figures open the way for stronger GDP growth in Q2 for now, after slowing to 0.2% q-o-q in Q1. The April industrial numbers are 1.8% above the first quarter average thanks to the April rebound. Despite a slight April decline, the construction sector is on an uptrend, thanks in part to strong housing starts, which rebounded from weaker building permits. Moreover, its sentiment does not suggest a change in trend. Foreign trade reached its lowest surplus below CZK4bn since the end of the energy crisis in 2022. However, this mainly reflects higher non-energy imports, while export activity also showed solid growth thanks to ICT. Thus, net exports are unlikely to drive GDP, similar to the first quarter when their weaker contribution was offset by stronger investment activity.

Jaromír Šindel

04. 06. 2026

April's decline in retail sales was largely the result of a correction of the previous strong growth in fuel and food. Although the correction after a strong March was also evident in core retail sales, they maintained their growth momentum, confirming the continued willingness of households to spend, supported by real wage growth and credit activity. However, factors are beginning to emerge in the second quarter that may slow the pace of household consumption. We discuss three of them below - real wage growth, credit activity and retail bonds.

Jaromír Šindel

29. 05. 2026

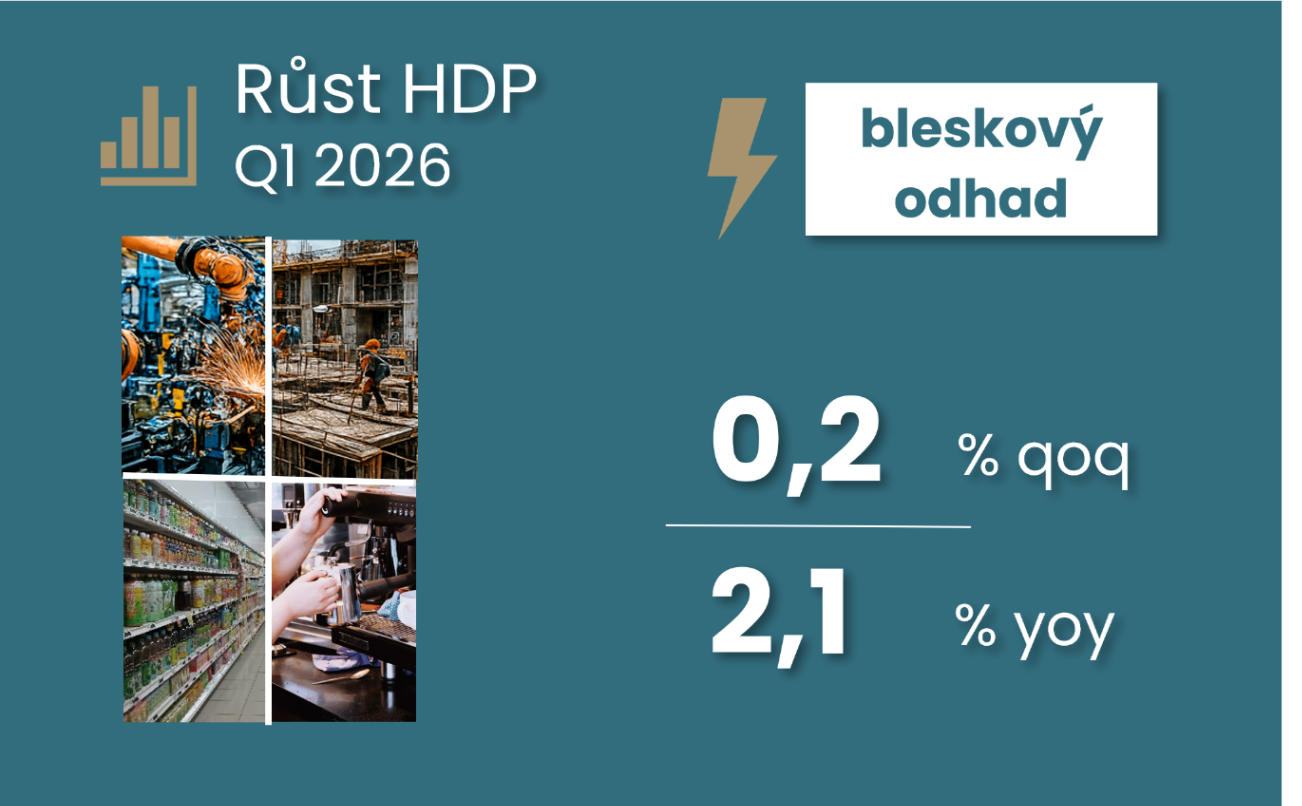

The Czech economy grew by 0.2% quarter-on-quarter in Q1. The weaker result was mainly due to technical factors, including the negative contribution of net exports and the budget provisionality. However, the structure of growth remains favourable thanks to continued growth in household consumption, investment and exports. In addition to the Iran war, weaker industry and persistent wage inflation pressures with slower productivity growth pose risks to the recovery to 2% economic growth this year.

Jaromír Šindel

21. 05. 2026

Slightly worse sentiment in May hides a drop in expected large purchases by consumers. If they translate into worse retail sales results in the coming months, these more modest plans would pose a downside risk to the 2% growth outlook for the Czech economy this year. This is based on a stable growth of almost 3% in household consumption. Other details reveal a slight correction in price expectations, which mitigates upside risks to inflation. The labour market receives a neutral report given its recent trend, i.e. slightly negative.

Jaromír Šindel

11. 05. 2026

March retail sales returned to strong growth, while March did not bring a turnaround in the stagnation of services. Industrial production did not build on February's better numbers, and a more significant deterioration was prevented by energy-intensive sectors, which does not look like a robust support in the current energy shock. Export activity also remained weaker. However, the month-on-month decline in imports resulted in the return of a solid foreign trade surplus of CZK 18 billion. Construction output, on the other hand, continued to outperform, especially in the buildings segment. However, despite still weak building permit numbers, the number of construction starts continued to rise. Infrastructure construction, on the other hand, remains weaker, presenting an opportunity for future growth. The output side of the economy thus developed in March in line with the weaker GDP growth of 0.2% q-o-q in the first quarter, which was characterised by a decline in industrial activity and a deterioration in foreign trade. These factors were only partly offset by stronger construction output and solid growth in trade and services sales (still with February data). For the CNB, the data, along with higher unemployment and softer industrial wage growth, signal a less hawkish environment than the still elevated momentum in core inflation suggests.

Jaromír Šindel

05. 05. 2026

GDP growth slowed to below 0.2 percent in the first quarter, a negative surprise. Instead of the expected household consumption, the economy was mainly driven by investment, while foreign trade worked against growth. However, the weaker consumption may be only a temporary correction after the strong end of last year. The same applies to industrial production, and the government's temporary budget provision also had a negative impact on the first quarter. The outlook will be significantly affected by the intensification of the commodity supply crisis due to the Iranian conflict.

Jaromír Šindel

07. 04. 2026

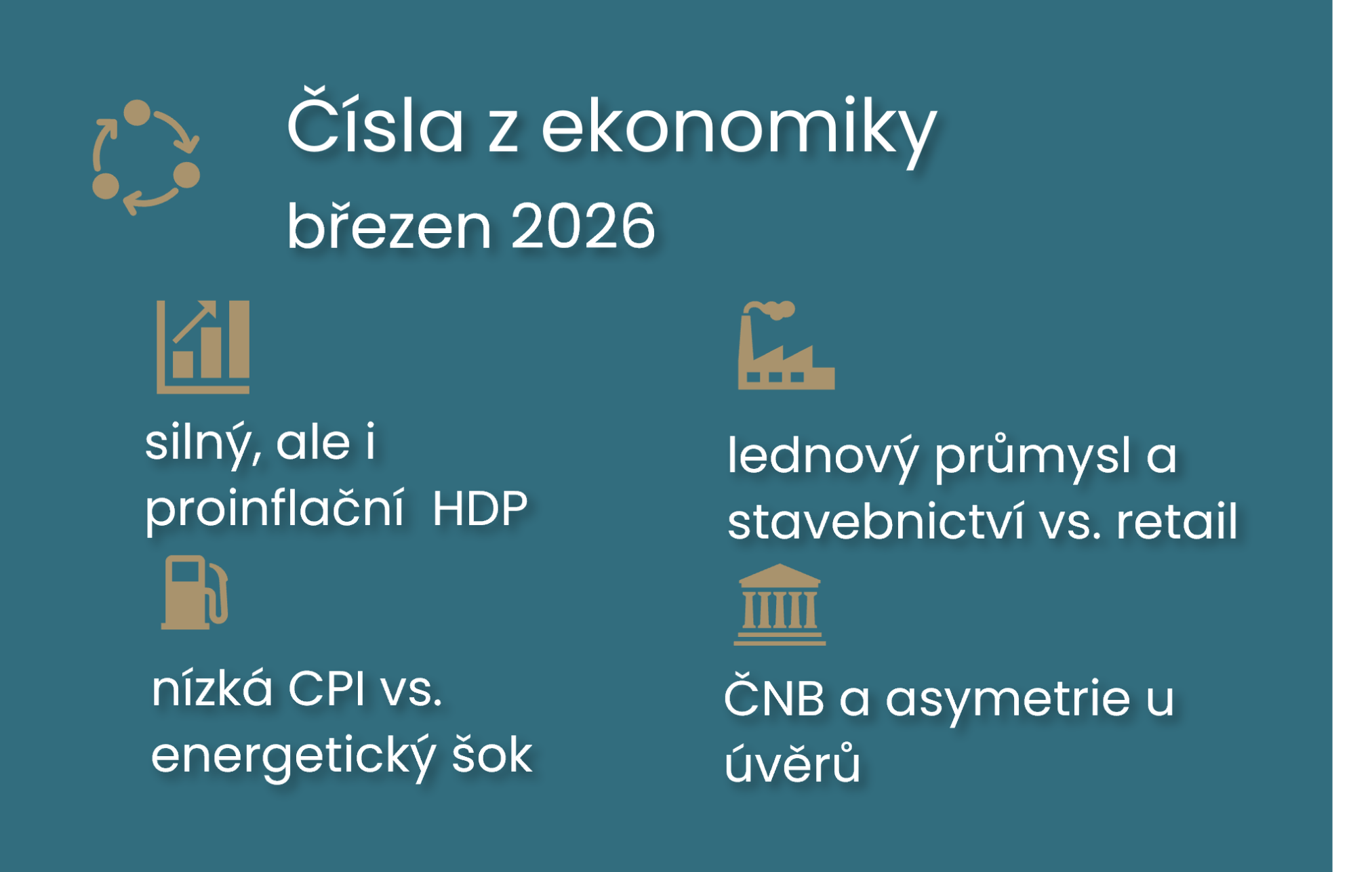

March inflation accelerated to 1.9% year-on-year in March, mainly reflecting higher fuel prices. However, the acceleration was somewhat milder than expected, helped by lower food prices. However, preliminary data suggest an acceleration in core inflation to 2.8%, which is not surprising given the still strong growth in retail sales. Although these did slightly correct the previous strong increase in January in the core segment in February. However, the strength of demand is relatively limited given the rather sluggish sales in services in the first two months of the year. The central bank will monitor the dynamics of these demand pressures, wages and core inflation, which will determine the speed and extent of its interest rate hikes in the coming months. Stronger demand is also translating into more robust imports, shrinking the foreign trade surplus that has not yet been affected by the energy price shock.

Jaromír Šindel

30. 03. 2026

The Czech economy accelerated at the end of last year and maintained its inflationary bias due to strong household consumption and strong wage growth unsupported by productivity. However, the central bank's New Year communication hinted at a possible interest rate cut. However, this rhetoric has been changed by the recent energy shock. For the central bank, the dynamics of core inflation will be key in the coming months, but also the pass-through of higher oil and gas prices to other price segments in the economy. March price expectations rose, but their April perception will be more guiding for the central bank.

06. 02. 2026

Comment by Jaromír Šindel, Chief Economist of the CBA: December data brought a positive end to the year with continued better-than-expected industrial production, including its structure. The same is true for construction output, which returned to a better performance, but the weaker number of building permits remains a drag. Foreign trade posted an improved surplus of over 25 billion kronor in December and nearly 220 billion kronor for the full year 2025. This is equivalent to 2.6% of GDP, down from 2.8% a year ago. While retail trade did not impress at the end of the year, this was not the case for industrial wages, which returned to double-digit annualized growth at the end of the year. Overall, the December data should not prompt more dovish rhetoric from the CNB, as it does not yet signal a disinflationary contribution from the real economy towards core inflation. However, in its new, stronger outlook, the CNB is also assuming an improvement in labour productivity, which, together with tighter monetary conditions, will bring inflation back towards its target.

05. 02. 2026

Comment by Jaromír Šindel, Chief Economist of the CBA: The significant slowdown in consumer prices to 1.6% year on year in January did not surprise the consensus and mainly reflects lower energy prices, but also food and fuel prices. On the contrary, I expect core inflation to remain at at least 2.8% growth from the end of last year. Although core retail sales corrected with a 0.6% month-on-month decline in December, annualized momentum, along with household plans, remains strong and does not suggest easing demand pressures. Thus, even in light of fiscal plans, interest rate stability appears to be an appropriate stance for the central bank, at least for the coming months. This is inconsistent with interest rate market targeting, but in my view this would require significantly lower core inflation pressures.

27. 01. 2026

Comment by Jaromír Šindel, Chief Economist of the CBA: January show stable economic sentiment, but industry continues to be plagued by weak demand with negative consequences for investment. On the other hand, consumer purchasing plans remain full of optimism, also thanks to both lower price expectations, which are dampened by industry but not services, and better expectations on the labour market, where the service sector, which is lacking more workers, is making a positive contribution. Thus, it looks like continued solid economic growth this year with noticeably lower headline inflation. This combination is likely to shift the discussion at the CNB from rate stability or growth to rate stability or a possible decline, which is, however, not certain given the ongoing "services inflation" and the change in fiscal policy settings.

08. 01. 2026

Comment by Jaromír Šindel, Chief Economist of the CBA: The November data confirm an acceleration in industrial activity, driven by the automotive industry and the recovery of energy-intensive sectors, which pushed annual industrial growth closer to 6%, the highest this year. However, further improvement may be hampered by the December decline in industrial sentiment and export expectations. Construction remains weak, and its high 7% y/y growth reflects the past rather than the current reality of limited public investment and weak building permits issued. The labour market has not yet cooled significantly despite a higher 3.3% selection unemployment rate, confirming continued solid wage growth of around 6% in industry. Quarter-on-quarter GDP growth will thus be underpinned by industrial production in Q4, probably also retail, but construction and the foreign trade surplus will rather take a bite out of it.

08. 12. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: The manufacturing part of the Czech economy remained subdued in October, which supports expectations of weaker GDP growth at the end of this year. However, a post-covetous historical foreign trade surplus is supporting the crown, which, together with a persistently solid wage pace, supported October retail sales. This part of the recent Czech growth model thus remains unchanged, but this is no longer the case for the construction sector, where persistent weakness in building permits and uncertainty over investment financing pose downside risks next year.

07. 11. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: Retail and services sales disappointed in September despite solid wage growth, which was confirmed by September industrial wages. A gradual but steady rise in unemployment is likely to be in evidence here. Thus, the stronger GDP growth in Q3 was helped by September's industrial production, which complemented the strong construction output of the previous months. Given sentiment, things might not be different in October.

30. 10. 2025

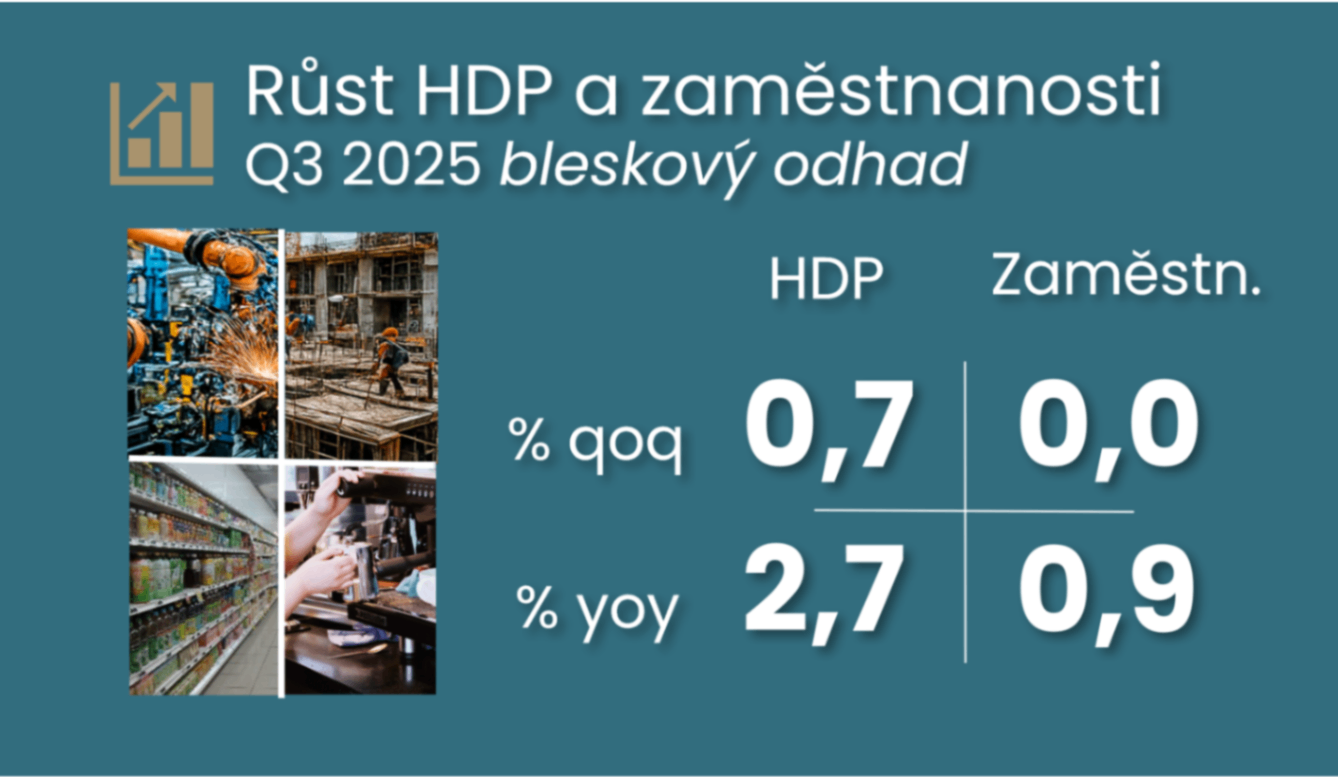

Comment by Jaromír Šindel, Chief Economist of the CBA: The return to stronger economic growth of 0.7% quarter-on-quarter in Q3 was a surprise, confirming the indications of stronger confidence in September. At the same time, stagnant employment added a welcome return to stronger productivity, which may partially dampen the hawkish impulse of stronger GDP for the CNB. The CNB will most likely leave interest rates unchanged at 3.5%, not only at the November meeting, but GDP details may set a more distinct tone to its communication later in November.

24. 10. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: Stronger sentiment in October suggests a return to stronger GDP growth for the end of this year after a probably slightly worse result in Q3. Higher price expectations may delay the return of core inflation to the target.

08. 10. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: The continuation of the construction boom and the recovery in retail sales in August was dampened by the return of weaker industrial production, despite stronger exports. However, the positive sentiment in September suggests that the slowdown in GDP growth in Q3 may not be as pronounced as the July and August figures suggest.

24. 09. 2025

Comment by Jaromír Šindel, Chief Economist at the CBA: September sentiment brings a boost after weaker monthly data in July and thus better prospects for GDP growth - mainly thanks to retail trade and construction.

08. 09. 2025

Economic commentary by Jaromír Šindel, Chief Economist of the CBA: Although the economy breathed a half-percent growth in the second quarter, the July figures were rather disappointing and suggest a cooling. However, the Czech economy is generating upside risks to inflation, which limits the room for manoeuvre of the CNB, which is likely to stick to the CNB's 3.5% terminal interest rate thesis. August's registered unemployment confirmed a worse trend, which, however, is not confirmed by other data.

07. 08. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

06. 08. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

30. 07. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

24. 07. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

11. 06. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

30. 05. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

12. 05. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

30. 04. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

25. 04. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

09. 01. 2025

Economic commentary by Jaromír Šindel, Chief Economist of the CBA

07. 10. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

06. 06. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

07. 05. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

08. 01. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA