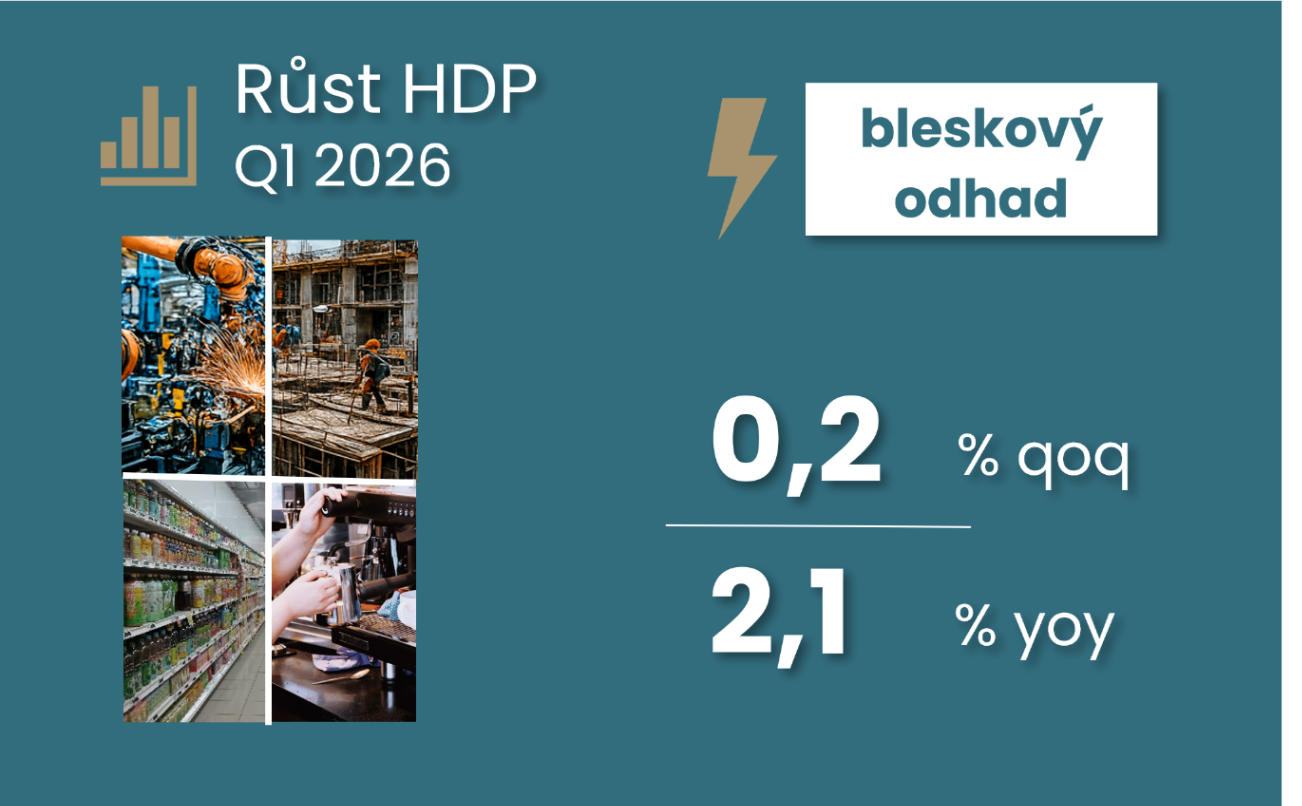

Quarter-over-quarter GDP growth in the first quarter of 2026 slowed to 0.2% from the previous 0.7% growth. This rate is below its long-term average growth of 0.68% from 1998 to 2019 and is below the average growth of 0.92% from the pre-pandemic period of 2015–2019. GDP in the first quarter of 2026 was thus 5.4% above the pre-pandemic level recorded in the fourth quarter of 2019. Average quarter-over-quarter GDP growth over the last four quarters reached 0.54%. On a year-over-year basis, GDP rose by 2.2% in the first quarter of 2026, following a previous growth rate of 2.7%. In the previous year, 2025, Czech GDP rose by 2.6% year-over-year, following 1.1% growth in 2024.

Gross Domestic Product Trends

CBA Monitor

You can hide a data set by clicking on the data set name in the chart legend.

Source of primary data

Czech Statistical Office

Category

Economy

Data Frequency

quarterly

Note

Data adjusted for the impact of varying numbers of working days and seasonal factors.

April's monthly figures open the way for stronger GDP growth in Q2 for now, after slowing to 0.2% q-o-q in Q1. The April industrial numbers are 1.8% above the first quarter average thanks to the April rebound. Despite a slight April decline, the construction sector is on an uptrend, thanks in part to strong housing starts, which rebounded from weaker building permits. Moreover, its sentiment does not suggest a change in trend. Foreign trade reached its lowest surplus below CZK4bn since the end of the energy crisis in 2022. However, this mainly reflects higher non-energy imports, while export activity also showed solid growth thanks to ICT. Thus, net exports are unlikely to drive GDP, similar to the first quarter when their weaker contribution was offset by stronger investment activity.

Jaromír Šindel

29. 05. 2026

The Czech economy grew by 0.2% quarter-on-quarter in Q1. The weaker result was mainly due to technical factors, including the negative contribution of net exports and the budget provisionality. However, the structure of growth remains favourable thanks to continued growth in household consumption, investment and exports. In addition to the Iran war, weaker industry and persistent wage inflation pressures with slower productivity growth pose risks to the recovery to 2% economic growth this year.

Jaromír Šindel

05. 05. 2026

GDP growth slowed to below 0.2 percent in the first quarter, a negative surprise. Instead of the expected household consumption, the economy was mainly driven by investment, while foreign trade worked against growth. However, the weaker consumption may be only a temporary correction after the strong end of last year. The same applies to industrial production, and the government's temporary budget provision also had a negative impact on the first quarter. The outlook will be significantly affected by the intensification of the commodity supply crisis due to the Iranian conflict.

03. 03. 2026

Comment by Jaromír Šindel, Chief Economist of the Czech Bank of Economics: The Czech economy closed last year with stronger growth than originally expected. The Czech economy could repeat its 2.6% annual growth this year. Household consumption was the driving force at the end of last year, supported by stronger wage growth, but also by strong growth in manufacturing. However, higher wage costs have far outpaced productivity growth, and so still elevated core inflation will remain the central bank's focus, which should result in the CNB interest rate holding steady at 3.5%.

30. 01. 2026

Comment by Jaromír Šindel, Chief Economist of the CBA: Economic growth slowed down at the end of last year, but still achieved solid 0.5% quarter-on-quarter GDP growth.The structure of growth has not changed significantly - consumption is dominant, which is probably not true of investment. This is in line with the latest sentiment data. A more positive sign is improving productivity. The outlook for this year is a repeat of last year's 2.5% growth, thanks to a better outlook for real wage growth and a change in fiscal policy. Conversely, weaker external demand, even given industrial sentiment, is likely to be a drag on stronger economic growth.

28. 11. 2025

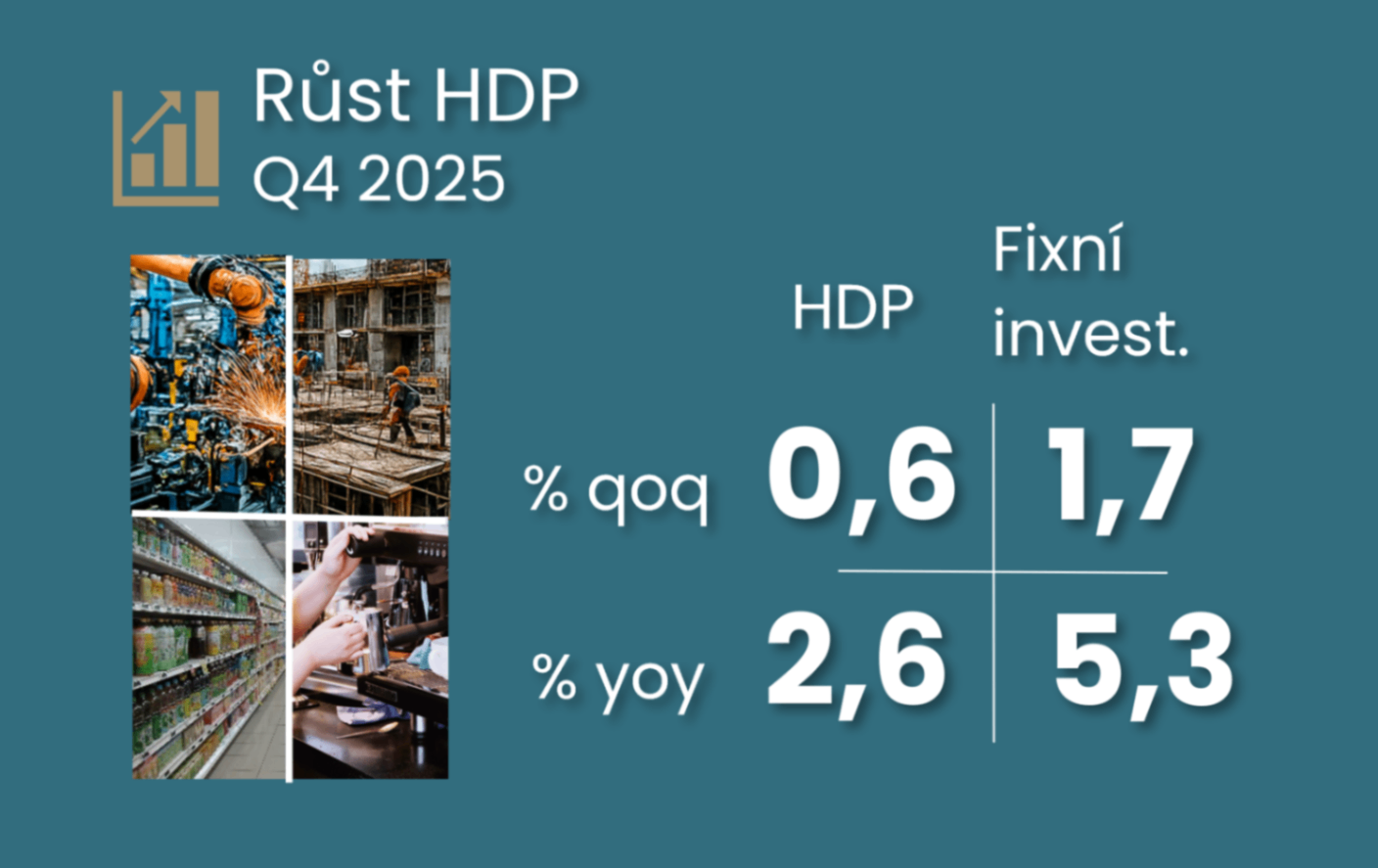

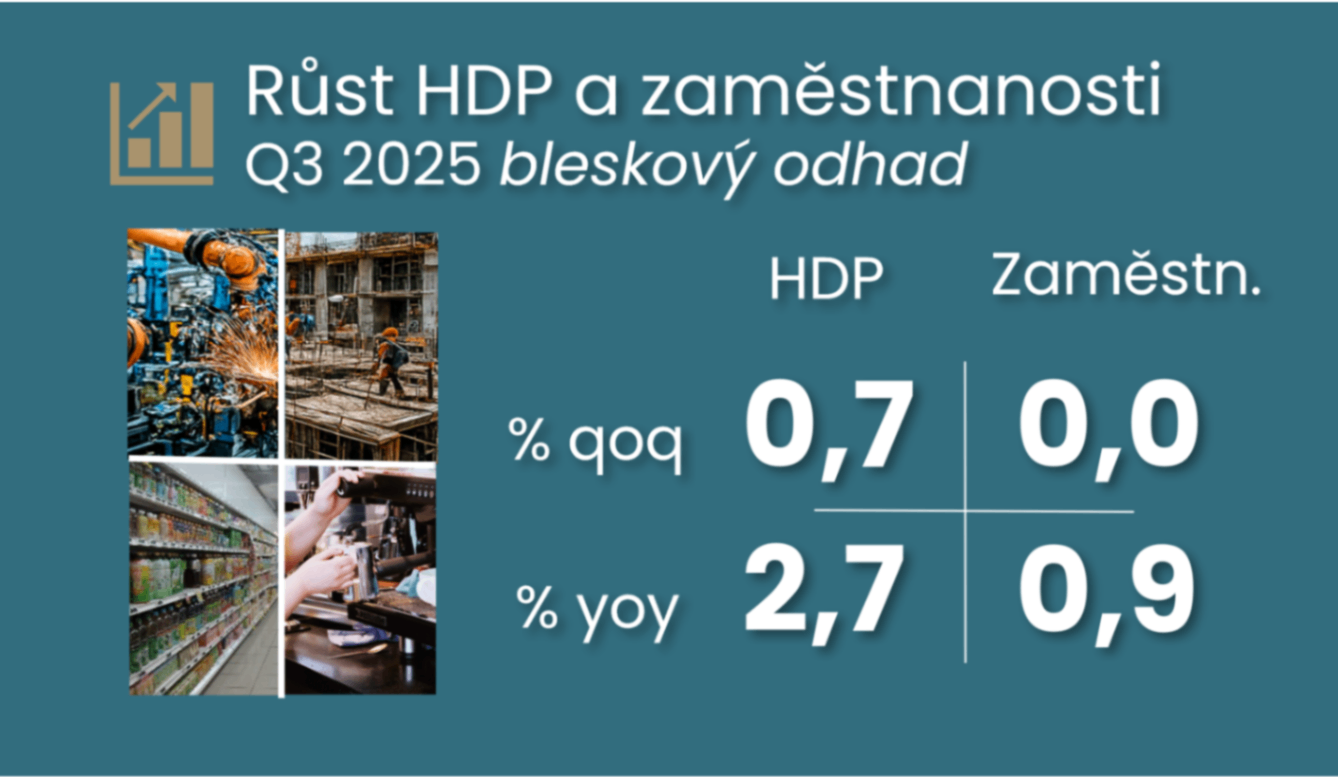

Comment by Jaromír Šindel, Chief Economist of the CBA: The stronger quarter-on-quarter GDP growth of 0.8% in Q3 mainly reflected foreign trade, while the contribution of domestic demand was not as strong as in the previous quarter. Moreover, there has been a continuous decline in fixed investment excluding construction investment, undermining the future potential of the economy and keeping productivity growth low and fuelling inflationary growth in unit labour costs (see five key points below).

30. 10. 2025

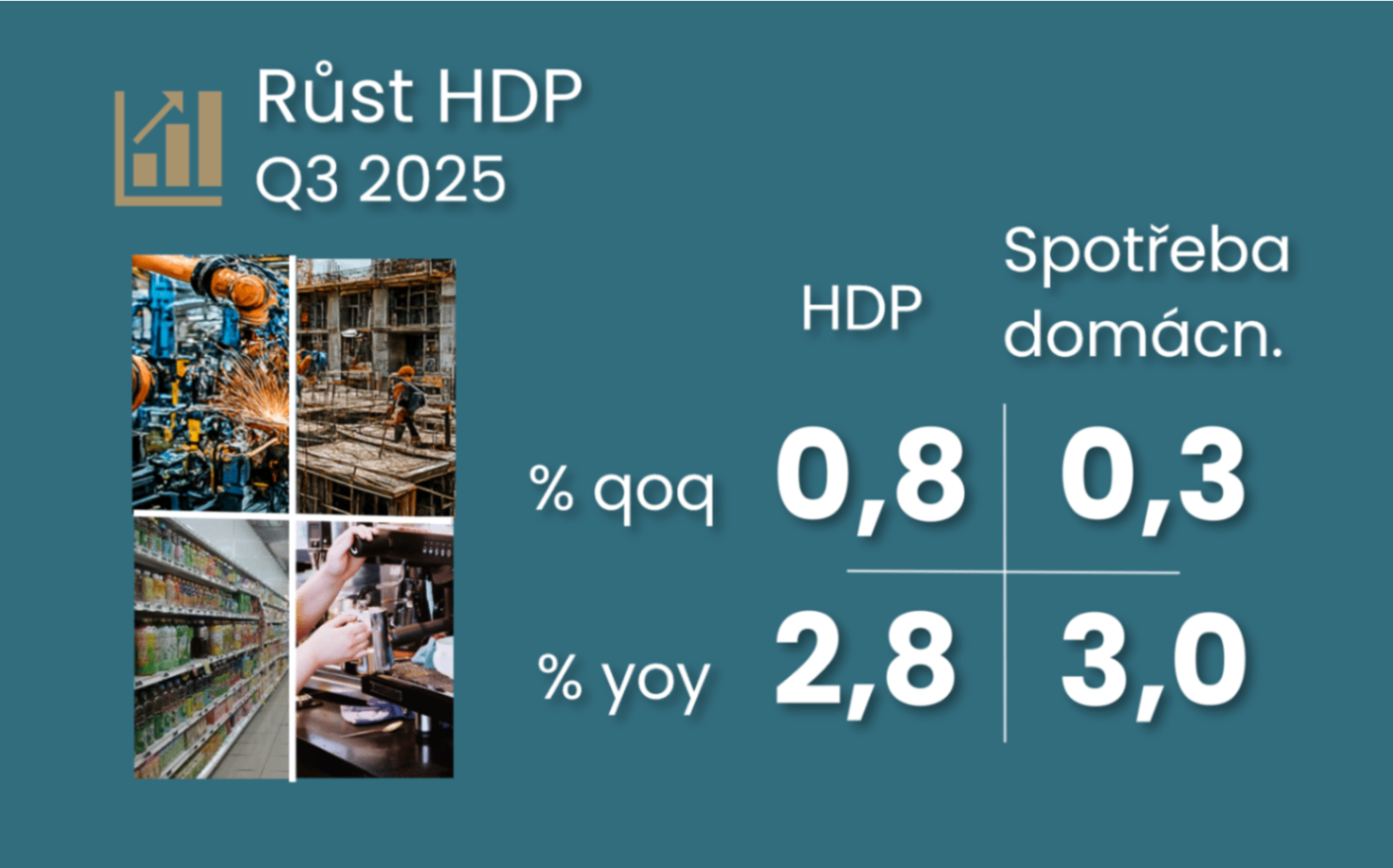

Comment by Jaromír Šindel, Chief Economist of the CBA: The return to stronger economic growth of 0.7% quarter-on-quarter in Q3 was a surprise, confirming the indications of stronger confidence in September. At the same time, stagnant employment added a welcome return to stronger productivity, which may partially dampen the hawkish impulse of stronger GDP for the CNB. The CNB will most likely leave interest rates unchanged at 3.5%, not only at the November meeting, but GDP details may set a more distinct tone to its communication later in November.

24. 10. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: Stronger sentiment in October suggests a return to stronger GDP growth for the end of this year after a probably slightly worse result in Q3. Higher price expectations may delay the return of core inflation to the target.

01. 10. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: The recovery in disposable income in Q2 was still dampened by fiscal policy, so it remained weaker compared to the increase in wages and property prices. Nevertheless, households managed to increase both consumption and their savings.

08. 09. 2025

Economic commentary by Jaromír Šindel, Chief Economist of the CBA: Although the economy breathed a half-percent growth in the second quarter, the July figures were rather disappointing and suggest a cooling. However, the Czech economy is generating upside risks to inflation, which limits the room for manoeuvre of the CNB, which is likely to stick to the CNB's 3.5% terminal interest rate thesis. August's registered unemployment confirmed a worse trend, which, however, is not confirmed by other data.

06. 08. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

30. 07. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

27. 06. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

11. 06. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

05. 06. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

30. 05. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

26. 05. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

30. 04. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

25. 04. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

30. 08. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

30. 07. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

30. 04. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

30. 01. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA