Strong GDP growth masks a key problem, namely continued weak investment and falling productivity while wage growth remains strong

Comment by Jaromír Šindel, Chief Economist of the CBA: The stronger quarter-on-quarter GDP growth of 0.8% in Q3 mainly reflected foreign trade, while the contribution of domestic demand was not as strong as in the previous quarter. Moreover, there has been a continuous decline in fixed investment excluding construction investment, undermining the future potential of the economy and keeping productivity growth low and fuelling inflationary growth in unit labour costs (see five key points below).

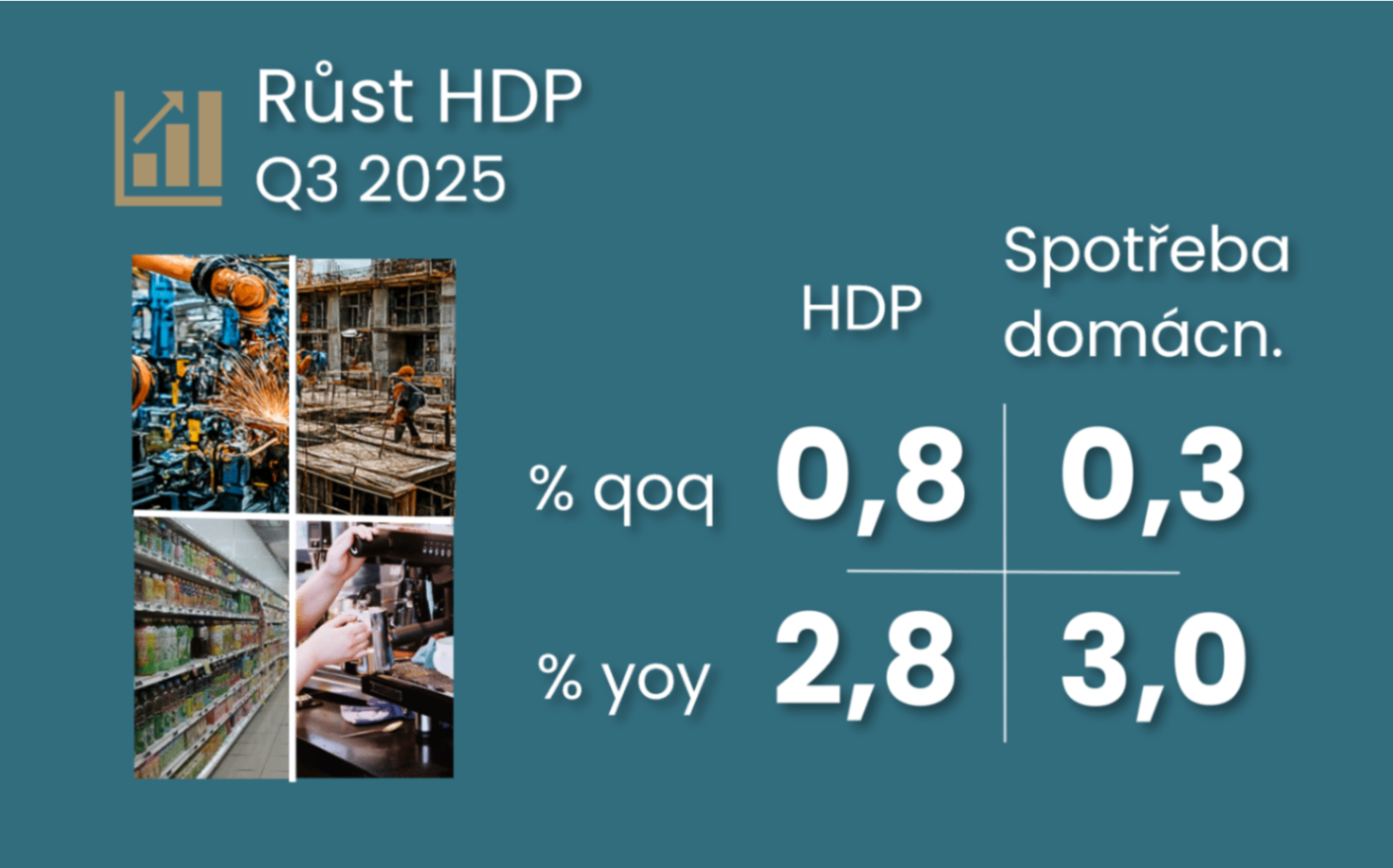

GDP growth in Q3 further exceeded expectations with its revision of quarter-on-quarter growth to 0.8%, which lifted annual growth to 2.8% (both seasonally adjusted). The original estimate of 0.7% and 2.7% growth had already "wiped out" many eyes. However, this is where the heady joy of a return to stronger economic growth ends.

The main expenditure components, i.e. household consumption, government and fixed investment, did not impress with their 0.3%, 0.1% and 0.4% increases, although they follow stronger increases of 1.2%-1.7% in the previous quarter. In contrast, quarter-on-quarter GDP growth was strongly supported by foreign trade, which in turn took a bite out of GDP in Q2. This reflects an acceleration in export dynamics, especially in services (goods continued to grow at a weak 0.3% q-o-q), and weaker domestic demand was also reflected in a decline in imports of goods.

For the CNB, the data represent neutral news despite stronger GDP growth, thanks to slower growth in unit labour costs and weaker domestic demand. However, weak investment activity and persistently strong quarter-on-quarter growth in unit labour costs in services do not suggest a break in the inflationary underpinning in the economy.

Five important points from Q3 on the outlook, which remains unchanged despite the better Q3 GDP, as the CBA's November Forecast announces a slowdown in the economy later this year (see chart-pack here), which should slow annual GDP growth next year to 2.2% from around 2.5% this year. In fact, however, we expect a return to stronger growth next year, as GDP should actually grow by 2.5% during that time. Continued real wage growth remains underpinning the outlook.

- Strong wage growth with likely high savings rate - This continued at a solid 1.5% q-o-q nominal per worker pace. This is admittedly less than the average 1.7% improvement in the previous three quarters. However, real growth fell only slightly to 1.1% from 1.3% in the previous quarter, and both figures exceeded the 0.7% growth in the previous five quarters. So the next national accounts data (January 2) will probably show a still high household savings rate(after 18.4% in Q2).

- Weakfixed investment - A continuous decline is evident after excluding the still strong construction investment in infrastructure and housing. This poses a challenge to kick-start productivity growth and dampen unit labour cost growth. It also poses a risk to the outlook for next year, which assumes more steady economic growth.

- Languishing productivity but demand-driven productivity recovery in business is becoming a reality - Employment growth slowed to 0.1% q-o-q in Q3 amid strong GDP growth, but GDP productivity growth per hour worked fell further (in construction, or public and financial services, among others) due to a 1.2% increase in hours worked.

- Higher employment utilisation - The economy thus grew due to more efficient use of the employed labour force. However, this has its limits, although it is possible that this may reflect higher employment of foreigners who are willing to work longer hours.

- Unit labour costs: divergence in industry vs. services - Although these slowed to 4.6% y/y in line with the CNB's forecast and showed a more modest quarter-on-quarter increase. However, the business services sector maintained its elevated quarter-on-quarter pace, which is unwelcome news given the higher price expectations in the services sector. In contrast, in construction and manufacturing, unit labour costs slightly corrected their previous growth.

- End note: the cumulative contribution of inventories to GDP growth is within the norm.

Productivity lags due to downturn in construction