The economy delivered another surprise with productivity growth picking up in Q3.

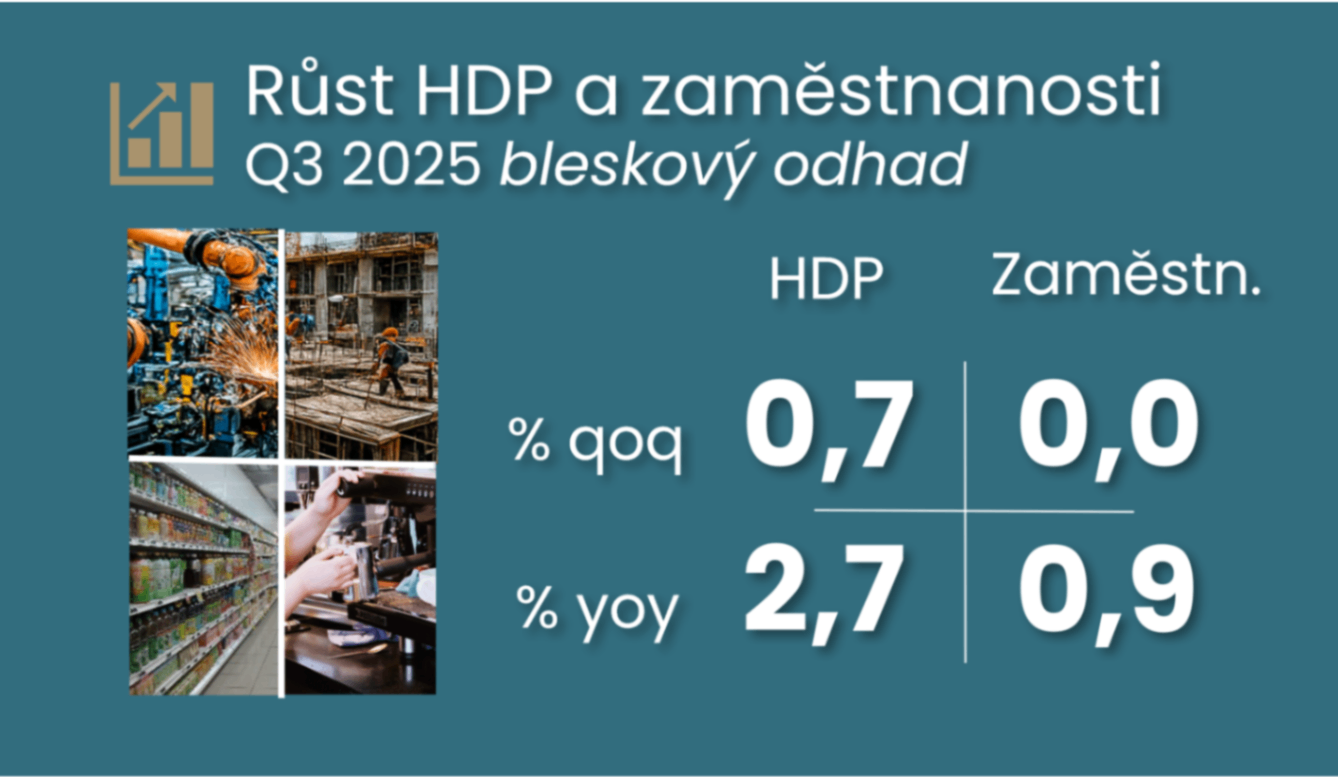

Comment by Jaromír Šindel, Chief Economist of the CBA: The return to stronger economic growth of 0.7% quarter-on-quarter in Q3 was a surprise, confirming the indications of stronger confidence in September. At the same time, stagnant employment added a welcome return to stronger productivity, which may partially dampen the hawkish impulse of stronger GDP for the CNB. The CNB will most likely leave interest rates unchanged at 3.5%, not only at the November meeting, but GDP details may set a more distinct tone to its communication later in November.

The economy returned to stronger growth in the third quarter, with GDP expanding 0.7% quarter-on-quarter, suggesting stronger monthly economic data for September. This would be consistent with September's stronger confidence in the economy, which strengthened further in October, albeit not with a clean slate. The acceleration in the economy comes after - from today's perspective - a modest half-percent slowdown in second-quarter GDP growth. The economy beat market and my expectations (0.3%) with its dynamism.

Unsurprisingly, construction and trade contributed positively to the quarter-on-quarter GDP growth, but other services also added - surprisingly, given the July and August figures so far. The stagnant employment is surprising from both perspectives, i.e. given the strong GDP growth and the higher unemployment (see Chart 3).

As a result, annual GDP growth rose modestly to 2.7% y/y, and the year-to-date average is 2.6%. If, given the stronger October sentiment, we conservatively expect the economy to slow to 0.3% q/q, then GDP would have added 2.5% y/y this year. Even so, it would almost match the Czech National Bank's 2.6% forecast and would then solidly beat both the Treasury's August forecast and the CBA Forecast, which counted on the economy growing 2.1% this year. The surprisingly strong GDP growth encourages expectations of a continuation of this solid trajectory, with the biggest hurdle being the ongoing structural challenges in the industrial sector.

The detailed economic numbers due on November 28 will offer two important insights.

1) Which sectors have led the way to higher productivity and stagnant employment. That is, whether the higher productivity was driven by industry (continued change in employment structure), which could dampen the CNB's fears of a stronger crown (see the September CNB meeting) and thus close off the possibility of a rate cut for the CNB in terms of communication.

2) How wage growth has evolved, which with its strong growth in Q2 - but coupled with low productivity growth - has increased market concerns towards future interest rate hikes. I currently perceive a general belief that the strong quarter-on-quarter momentum in the second quarter was temporary.

The return to stronger economic growth of 0.7% quarter-on-quarter in the third quarter was a surprise, confirming the signs of stronger confidence in September

At the same time, stagnant employment has added a welcome return to stronger productivity

The stagnant employment is surprising from both perspectives, given the strong GDP growth and higher unemployment