According to the Czech Statistical Office’s June economic sentiment survey, confidence in the Czech economy remains around the long-term average following a month-over-month improvement. Sentiment is above last month’s level but remains below that of the previous three months. Compared to last year’s figure, it is in a better position. Individual sectors stand as follows relative to the long-term average: * industry and trade are below long-term averages, * while the household, services, and construction sectors are above the long-term average. The month-over-month improvement in economic confidence in June primarily reflects stronger confidence in the industry and household sectors, while a decline in sentiment in the construction, services, and trade sectors partially offset this. Sector-specific trends show that June household sentiment was above last month’s level (but below the level of the previous three months) and above last year’s level; in industry, it is better than last month (and above the previous three-month average) and better than last year; in services, it is below last month’s level (but above the level of the previous three months) and worse than a year ago; in retail, it is worse than last month (and below the previous three-month average) but better than last year; and in construction, it is below last month’s figure (and below the level of the previous three months) and below last year’s level. For more, see the “Comments” section on the ČBA Monitor: https://www.cbamonitor.cz/kategorie/ekonomika

Confidence Indicators

indices, long-term average = 100

CBA Monitor

You can hide a data set by clicking on the data set name in the chart legend.

Source of primary data

Czech Statistical Office

Category

Economy

Data Frequency

monthly

Note

Seasonally adjusted data. For more detailed information on the methodology, see https://csu.gov.cz/konjunkturalni_pruzkum

Economic confidence improved slightly in June. Stronger sentiment among households and manufacturers outweighed continued weakness in retail trade, although retail conditions may improve over the coming months. At the same time, the services sector points to higher risks for both unemployment and core inflation—that is, inflation excluding the volatile prices of energy and food. For the Czech National Bank (CNB), the June sentiment survey suggests a need for caution, reflecting stronger household demand and a renewed rise in price expectations in services.

Jaromír Šindel

21. 05. 2026

Slightly worse sentiment in May hides a drop in expected large purchases by consumers. If they translate into worse retail sales results in the coming months, these more modest plans would pose a downside risk to the 2% growth outlook for the Czech economy this year. This is based on a stable growth of almost 3% in household consumption. Other details reveal a slight correction in price expectations, which mitigates upside risks to inflation. The labour market receives a neutral report given its recent trend, i.e. slightly negative.

Jaromír Šindel

24. 04. 2026

April sentiment already reflects the impact of the Iranian conflict on the Czech economy more strongly, but unevenly across sectors. Sentiment deteriorated as expected in industry, households and retail trade, while services dampened the overall deterioration thanks to stronger demand and construction. Price expectations continued to rise in industry, households and construction, while retail sales remained close to the long-term average and services corrected slightly after the previous increase. Meanwhile, labour market effects remain limited even in the harder-hit sectors and, in fact, the overall slightly worse sentiment still does not provide an immediate signal for worse growth expectations for the economy.

Jaromír Šindel

30. 03. 2026

The Czech economy accelerated at the end of last year and maintained its inflationary bias due to strong household consumption and strong wage growth unsupported by productivity. However, the central bank's New Year communication hinted at a possible interest rate cut. However, this rhetoric has been changed by the recent energy shock. For the central bank, the dynamics of core inflation will be key in the coming months, but also the pass-through of higher oil and gas prices to other price segments in the economy. March price expectations rose, but their April perception will be more guiding for the central bank.

27. 01. 2026

Comment by Jaromír Šindel, Chief Economist of the CBA: January show stable economic sentiment, but industry continues to be plagued by weak demand with negative consequences for investment. On the other hand, consumer purchasing plans remain full of optimism, also thanks to both lower price expectations, which are dampened by industry but not services, and better expectations on the labour market, where the service sector, which is lacking more workers, is making a positive contribution. Thus, it looks like continued solid economic growth this year with noticeably lower headline inflation. This combination is likely to shift the discussion at the CNB from rate stability or growth to rate stability or a possible decline, which is, however, not certain given the ongoing "services inflation" and the change in fiscal policy settings.

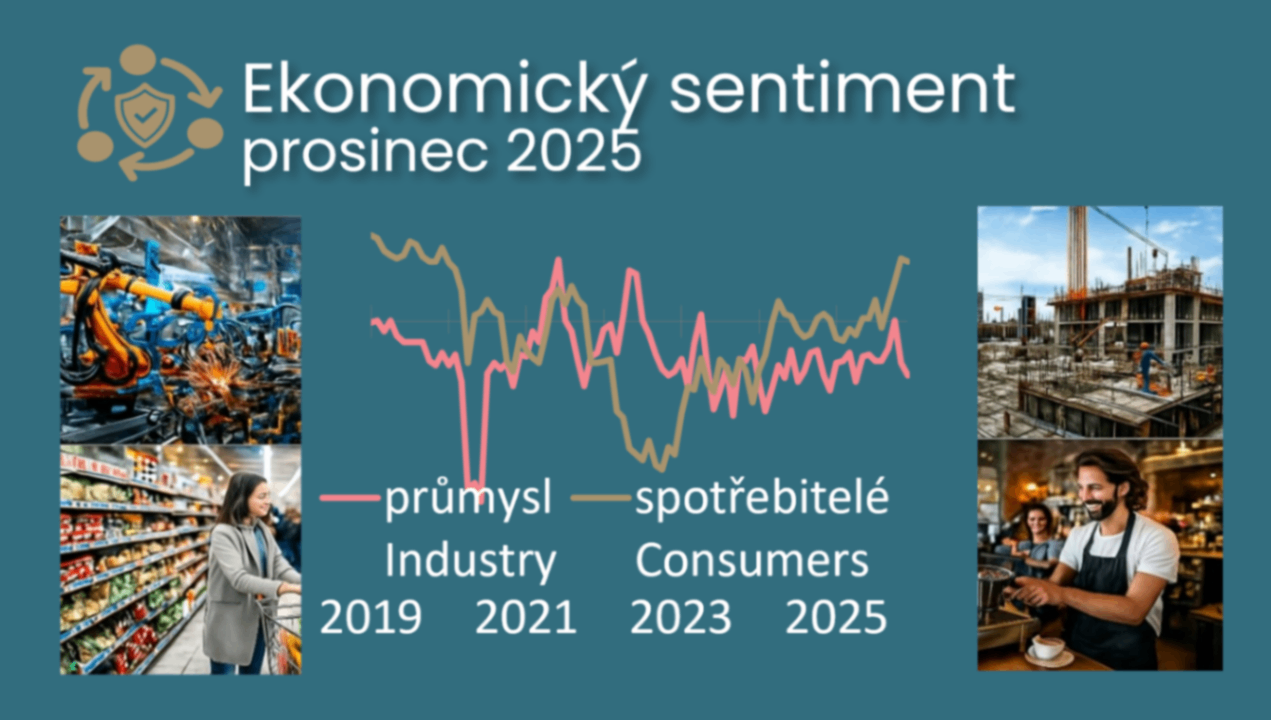

23. 12. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: The deterioration in economic sentiment in December does not yet represent a turning point for the outlook for the Czech economic recovery, which anticipates a deterioration in dynamics at the end of the year 2025. Household consumption plans remain resilient, while industry and the labour market are sending rather cautious signals, which poses a risk to the expected recovery in investment activity and the early stabilisation of rising registered unemployment. The outlook for lower administered energy prices supports falling price expectations, but persistent pressures in construction and services continue to dampen disinflationary optimism, sending a neutral rather than dovish message to the central bank.

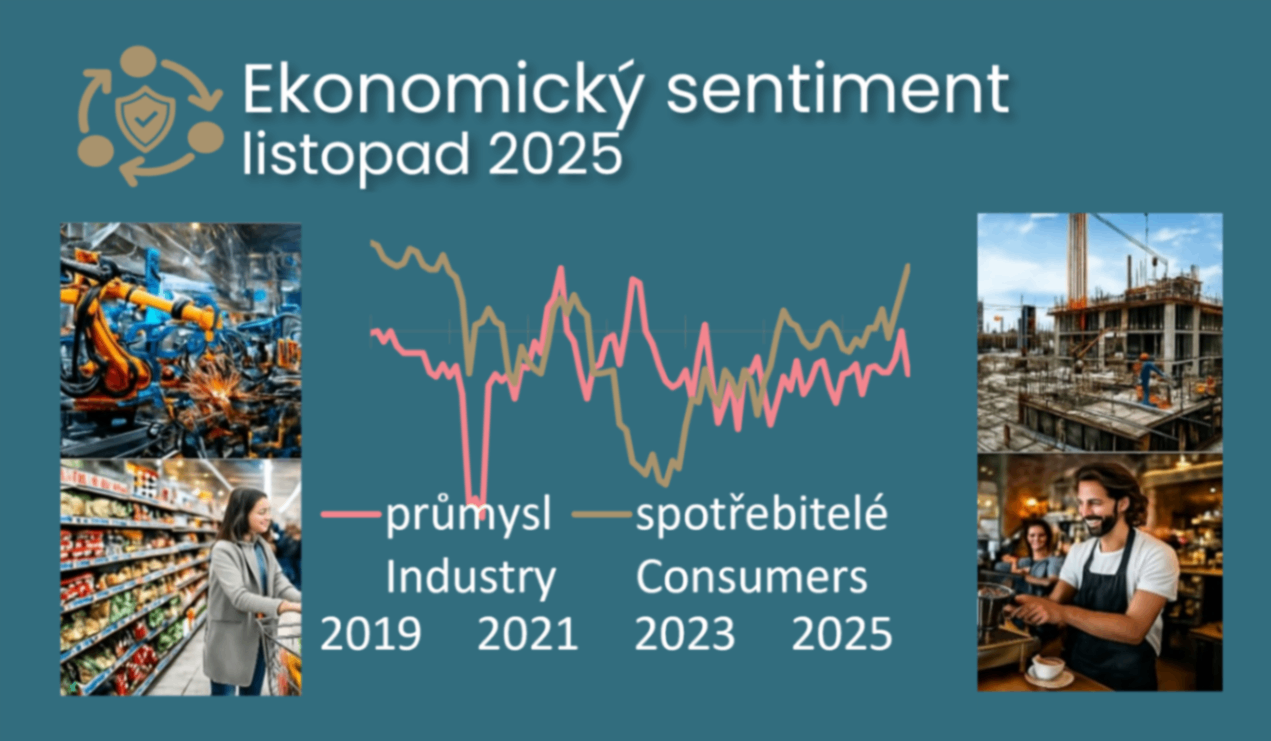

24. 11. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: November's confidence in the Czech economy weakened slightly, but still suggests continued growth. However, there are significant differences across sectors, reflecting the looming change in economic policy after the elections. Households remain visibly more optimistic, thanks to rapidly rising wages and perhaps in response to the new government's plans, while industry is returning to earlier weakness. Services are again reporting rising price expectations, keeping the central bank in hawkish mode.

24. 10. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: Stronger sentiment in October suggests a return to stronger GDP growth for the end of this year after a probably slightly worse result in Q3. Higher price expectations may delay the return of core inflation to the target.

25. 08. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

24. 07. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

24. 06. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

26. 05. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

25. 04. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

29. 01. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

24. 10. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

24. 09. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

26. 08. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

24. 07. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

24. 05. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

25. 03. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

23. 02. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

24. 01. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA