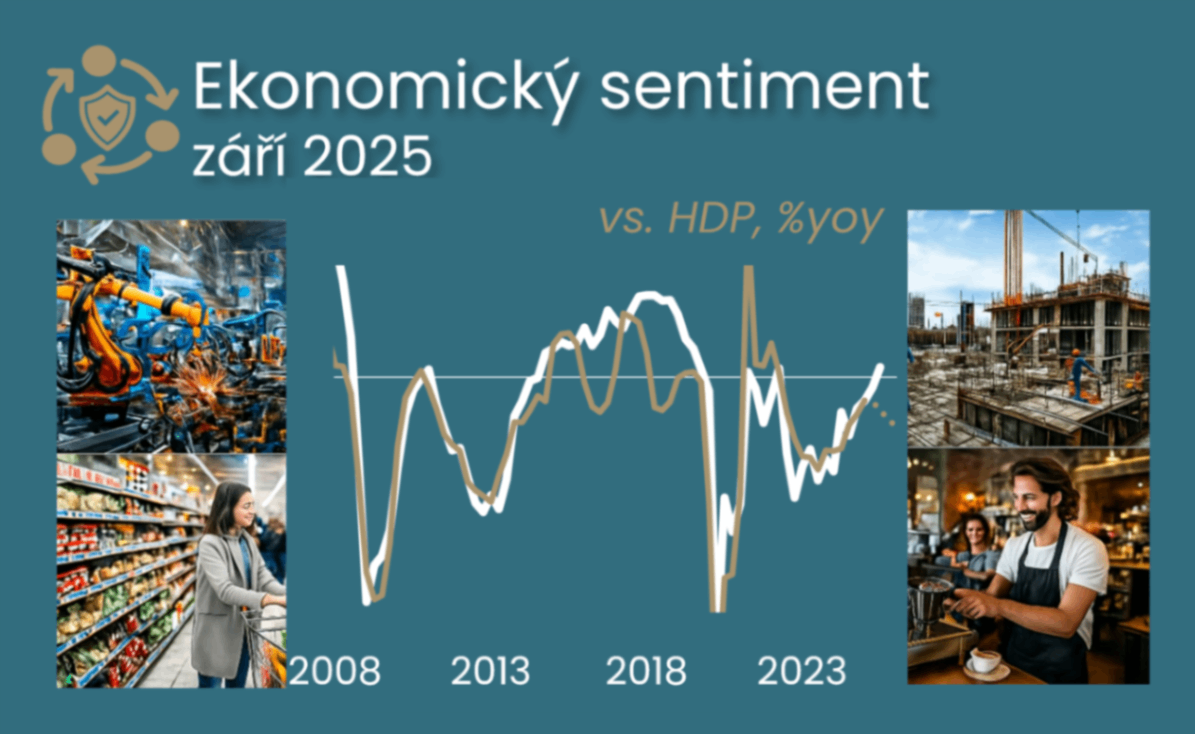

September sentiment pleasantly surprised

If September's improved sentiment is sustained and reflected in the monthly data, then this would indicate a chance to maintain the solid GDP growth momentum. September's stronger sentiment improved on the previous three months and is slightly above the long-term average. It thus represents a boost for the monthly economic data, which rather disappointed in July - either by a slow recovery in the case of industry or retail trade, or by weakening momentum in services. The July data also represented the limit for a repeat of the decent GDP growth in the third quarter, following 0.5% quarter-on-quarter growth in the second quarter. Thus, September sentiment may represent a positive signal compared to July and for our forecast of 2.1% annual GDP growth this year.