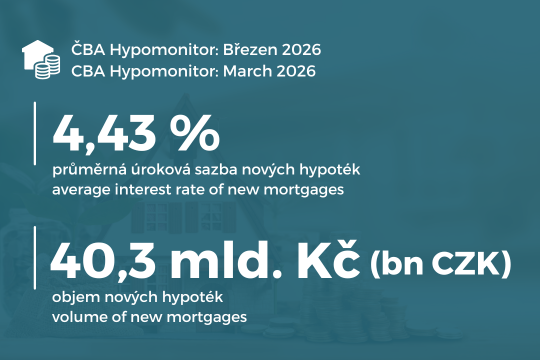

CBA Hypomonitor: March continued with a temporary boom in mortgages, thanks to a lower rate of 4.43%.

The average amount of a new mortgage exceeded CZK 4.8 million

Prague, 16 April 2025 - March ranked among the strongest months with its volume of newly granted mortgages, with a still high number of new mortgages granted. In March 2026, banks and building societies actually granted new mortgages without refinancing for CZK 40.3 billion. Compared to February, activity was up 36% in volume terms, reflecting the seasonal effect, and even after seasonal adjustment the mortgage market remained as strong as in January and February. Since the beginning of the year, the volume of new mortgages has reached CZK 97 billion, i.e. CZK 30 billion more than a year ago. Added to this is the strong volume of refinanced mortgages, which accounted for more than 27% of the more than 55 billion in new mortgage business in February.

Despite the rise in market interest rates, another contributor to the higher volume of new mortgage originations was a slight decline in the average realised interest rate on new mortgages to 4.43% from 4.46% in February, in addition to the approaching stricter CNB conditions for so-called investment mortgages. Banks thus dampened the rise in market interest rates in March. In our study, we pointed to structural factors, particularly the strength of demand in a competitive market, that affect the impact of market interest rates on mortgage rates. The effect of frontloading with a lower interest rate or investment mortgage is likely to have been reflected in a higher average mortgage size. It surpassed CZK 4.8 million in March. This increase was also reflected in a higher monthly repayment for newly granted mortgages, which exceeded CZK 25,000 on average in March and CZK 20,000 for the median mortgage.

The above information is derived from data from the CBA Hypomonitor, which captures data from all domestic banks and building societies providing mortgage loans. The next CNB meeting related to the setting of macroprudential policy on mortgages will take place on 4 June, following March's relatively hawkish comments on the setting of the current 1.25% countercyclical capital buffer (subsequent meetings will be held on 10 September and 26 November).

Table 1: Summary of mortgage origination volumes and average interest rates for March 2026

|

|

Monthly values |

|

year-to-date values |

||||

|

|

Volume |

Number |

Rate |

|

Volume |

Number |

Rate |

|

|

|

||||||

|

Total |

55,4 |

12 197 |

4,42 |

|

131,2 |

29 589 |

4,44 |

|

New loans |

40,3 |

8 381 |

4,43 |

|

97,0 |

20 807 |

4,45 |

|

of which: |

|

|

|

|

|

|

|

|

for purchase |

29,5 |

6 153 |

4,43 |

|

73,3 |

15 716 |

4,45 |

|

for construction |

5,9 |

1 244 |

4,40 |

|

14,0 |

3 008 |

4,42 |

|

Other |

4,9 |

984 |

4,49 |

|

9,7 |

2 083 |

4,52 |

|

Refinanced from another institution |

12,7 |

3 241 |

4,37 |

|

28,7 |

7 414 |

4,41 |

|

Refinanced internally, increased |

2,3 |

575 |

4,42 |

|

5,5 |

1 368 |

4,42 |

Source. Note: seasonally unadjusted data

"The strong March figures were probably due to the frontloading factor of lower interest rates and more favourable conditions for investment mortgages. The former reason reflects the reverberations of the central bank's New Year interest rate cut, while March reversed the trend with the Iranian price shock.The second reason is the April activation of stricter central bank rules for investment mortgages," believes Jaromír Šindel, chief economist at the Czech Banking Association.

Note: the outlook to the end of the year is momentary - it is based on the current trend, not on a model forecast.

March remained on probably temporarily strong volumes and numbers

"The housing market has maintained its high momentum in recent months and we expect house prices to continue to rise, albeit at a more moderate pace. The long-term excess of demand represents a structural characteristic of the Czech market, which stems mainly from limited new construction. We are therefore also focusing on broader approaches to achieve better housing affordability for different groups of the population.An example is our support for cooperative housing with significant potential for expanding the market supply," adds Martin Vašek, CEO of the Mortgage Bank of ČSOB Group.

Overall, banks and building societies granted new and refinanced mortgages in the amount of CZK 55.4 billion in March, which is 36.8% more than a month ago. Their total volume so far this year has reached CZK 131 billion, a 62% increase compared to January-March of the previous year.

In March, banks and building societies actually granted new mortgage loans without refinancing for CZK 40.3 billion. Compared to February, new mortgage activity was thus up by around 36% in volume terms, partly due to seasonal effects (typically, the volume of new mortgages rises by 28% month-on-month in March; the previous month it was up by 10% compared to the usual 13%). After seasonal adjustment, March's new mortgage figures brought a 6% improvement to CZK 35.8 billion compared to February's CZK 33.8 billion. It thus slightly surpassed January's record and ranked first in terms of volume. In year-on-year terms, the growth in the volume of mortgage originations strengthened to 49% in March after an average 41% year-on-year increase last year. Around 76% of new lending volume this year has been for purchase, below last year's average of 79%, with construction lending up slightly to 14% and other lending growing at 10%.

The number of new mortgages rose 30.7% month-on-month to 8,381 in March, up 25% from a year ago. We estimate the seasonally adjusted number to be around 7,480, around 5% above the average number (7,104) in the previous three months. Year-to-date, the number of new mortgages has reached 20,800, almost a quarter more than a year ago. The dynamics of the number of new mortgages from the last three months, i.e. January to March, imply an increase this year to a total of around 89.2 thousand, which would be almost 17% more than last year. But after the CNB's tightening of conditions in April, we can expect fewer new mortgages, which, with a negative 7% shock, would close this year below 85k, 11% higher than last year. However, these numbers would remain below the average of 95k from 2016 to 2018 or, more significantly, below the 114k of 2021.

The share of refinanced and increased loans is increasing despite strong growth in new mortgages. This is 113% above the average 7.1 billion refinanced last year and 285% above the 3.9 billion refinanced in 2024. The share of refinanced loans in total mortgage originations then rose to 27.3%, above last year's average of 20.7%. It is thus above the 17.2% share from 2022-2023, but still below the nearly 29% share from 2020-2021, when households refinanced at a mortgage rate of 2.14%. In March 2026, households refinanced at a rate of 4.38%, but this is 0.3 percentage point lower than the 4.66% rate a year ago. The higher refinancing volumes reflect the confluence of expiring longer fixings from the low interest rate period and shorter fixings from the recent period of higher interest rates.

Chart 2: Trend in new mortgages granted without refinancing

The beginning of this year showed strong above-average volumes, even as a percentage of the economy's performance.

Source: Czech banking association, CNB, CZSO, Flat Zone

Chart 3: Average mortgage size by purpose

The average size of an actual new mortgage increased to CZK 4.81 million in March. The number of new mortgages granted was CZK 1.6 million, up 19% year-on-year.

Source: CNB, Czech banking association - Hypomonitor

"March was very successful in terms of mortgages and one of the factors behind this success is the price. It was very favourable in March but is expected to rise in the coming months.Geopolitical events are to blame, as the Iranian conflict is driving up fuel prices, which will result in higher inflation and probably higher interest rates," says Petr Gapko, chief economist at MONETA Money Bank.

The average mortgage rate fell slightly further to 4.43% in March, but the jump in market rates will break this trend

The average realised interest rate on new mortgages fell slightly further to 4.43% in March from 4.46% in February. Its reduction follows February's slight decline, reflecting the previous decline in market interest rates, which had been pricing in a CNB rate cut in the first two months. As a result, the March mortgage rate is a quarter of a percentage point lower than the 4.68% rate a year ago, which reduces monthly mortgage payments by approximately 0.7% of the applicant's net income, or 0.7k. CZK. By comparison, the average mortgage rate in 2025 was 4.58% compared to 5.07% in 2024.

However, Czech market longer-term interest rates,[1] which are a key influence on mortgage rates, rose significantly in March. At 4.43%, the March mortgage rate was 0.34 percentage points above average market swap rates. This is about 0.72 p.p. below the long-term average since 2014 (1.06 p.p.). Czech five-year interest rate swaps rose 0.6 percentage point to 4.2% in March from 3.6% in February. Their March level is a quarter of a percentage point above the previous fourth quarter's average of 3.93%. Over the past twelve months, Czech five-year swaps have ranged between monthly averages of 3.29% (as of April 2025) and 4.19% (as of March 2026).

Similarly, in response to the supply shock due to the Iran war, US five-year interest rate swaps rose to 3.8% in March from 3.7% in February, while euro five-year swaps rose to 2.74% in March from 2.45% in February and were 0.4 bps above their average level last year of 2.34%. Domestic factors that may also have fed into the interest rate swaps were mainly (I) higher March core inflation; (II) still solid retail sales; (III) strong industrial wage growth; (IV) following strong wage growth at the end of last year; and (V) accompanied by weaker productivity growth.

[1] These are mainly long-term interest rate swaps (IRS), which reflect the price of money at longer maturities, such as 2 to 10 years.

Chart 4: Average mortgage interest rate - new business

March mortgage rates fell slightly further

Source: CNB, Czech banking association - Hypomonitor

Chart 5: The US attack on Iran significantly increased market swap interest rates

Source: LSEG, Macrobond (15 April 2026), CBA

Impact on the average monthly mortgage payment of around CZK 25.6 thousand, but with a median of over CZK 20 thousand

The combination of the fall in interest rates and the higher average mortgage amount in March 2026 compared to the 2025 averages increased the average monthly mortgage payment of a newly granted mortgage by 2.8k. Kc. Table 2 shows the monthly repayment scenarios for different mortgage maturities. It suggests that a fall in mortgage rates of almost 0,2 percentage point relative to their average rate of 4,58 % in 2025 would, for an average mortgage size with a typical repayment term of around 26,8 years, reduce the monthly repayment by less than CZK 400 to around CZK 25,6 thousand. This is a reduction of 0.4% of the applicant's net income compared to the average repayment in the previous year.

Conversely, compared to the average 2.8% mortgage rate for new mortgages in 2019, the current refinance mortgage rate of 4.16% for a shortened loan term raises the monthly payment on the average mortgage by almost CZK 1,300, or about 2.6% of the current gross average wage.

Table 2: Illustration of the average and median monthly repayment of a new mortgage by maturity and interest rate

Source: CBA (a table with values is available in the xls file attached to this report)

Note: The colored bar corresponds to the interest rate of the latest CBA Hypomonitor combined with the usual maturity, the other rates are illustrative. The coloured row corresponds to the average and median maturity of new mortgages according to CNB data; amounts are rounded to the nearest ten kroner. The median repayment amount is based on the median mortgage size. It is calculated on the basis of the ratio of the average and median size of new mortgage loans over the last three quarters according to CNB statistics (118,7 %). The calculation also assumes an average maturity of 30 years (corresponding to the median) and an average interest rate, since the difference between the average and median rates is negligible in the long term (approximately 0,045 percentage point). The median, unlike the mean, represents a 'typical' value - half of the loans are lower and half are higher - and is not affected by outliers.

The average size of a newly granted mortgage has increased with January's 4.51 million. CZK is on a growth trajectory

The average size of an actual newly granted mortgage rose to CZK 4.81 million in March. CZK, i.e. by almost 4% month-on-month. Its size is thus 19% higher than the CZK 4.04 million in the same period last year. CZK a year ago. The higher average mortgage size probably reflects the frontloading effect for so-called investment mortgages, where the CNB will tighten requirements from April (LTV to 70% and DTI to 7x), but the frontloading effect is also likely to be relevant due to the break in market interest rates. The gradual rise in real household wages (5.1% y/y in Q4-2025 or charted here) is also a backdrop.

Mortgage rates are then also linked to house price developments, which continued to grow strongly at almost 11% y/y in Q4-2025. Offer prices accelerated slightly to 2.7% quarter-on-quarter in Q1 2025, still above their long-term average increase of 1.8%. According to data from Flat Zone, the average transaction price of both new and older apartments in the country reached CZK 97.5k in Q4. This reflects a 2% quarter-on-quarter and 11.3% year-on-year increase.

Chart 6: Illustrative comparison of the monthly instalment of the average newly granted mortgage with a year ago, depending on the interest rate, mortgage size and maturity in years

In a year-on-year comparison, the fall in the mortgage rate resulted in an illustrative saving of CZK 700 on the average monthly instalment, but the increase in the average mortgage amount caused an increase of CZK 3,370.

Source: Czech banking association - Hypomonitor

Note: Amounts are rounded to tens of crowns.

Statistical annex

Chart 7: Seasonality of new mortgage loans

Source: Czech banking association - Hypomonitor

Note: These are actually new mortgages (i.e. excluding refinancing and increases). The underlying data is available in the xls file attached on the CBA Hypomonitor website.

Chart 8: Distribution of new mortgage loans by purpose

Source: Czech banking association - Hypomonitor

Note: The last figure represents the average for the last 12 months.

Mortgage market to deliver strong volume growth of 41% in 2025 and nearly a quarter in numbers

In the full year 2025, banks and building societies provided new mortgage loans worth CZK 321 billion. This is CZK 93 billion more than the CZK 228 billion created in 2024. This year-on-year jump corresponds to a 41% increase. On top of that, mortgages were refinanced to the extent of CZK 85 billion, bringing the entire mortgage market to CZK 406 billion in 2025 from CZK 275 billion in 2024. If we adjust the volumes for the increase in house prices of around 15-16% (according to various statistics), the volume of new mortgages grew slightly less in real terms. This corresponds to a more moderate increase in the number of new mortgages in 2025, by less than a quarter to more than 76.11 thousand, and a nearly 15% increase in the average amount of a new mortgage granted to CZK 4.21 million.

New mortgages were financed at an average interest rate of 4.58% in 2025, half a percentage point lower than in 2024, with the spread to the market swap rate curve less than one percentage point, slightly below the long-term average. The average monthly mortgage payment in 2025 was just under CZK 22,800, up 8.6% from 2024, and slightly above the likely more than 7% increase in average nominal wages last year. The average year-on-year increase in the monthly mortgage payment of approximately CZK 1,800 in 2025 mainly reflected a higher average mortgage level with an increase in the payment of almost CZK 2.9k. CZK, while the lower mortgage interest rate reduced the average monthly payment by more than CZK 1.2 thousand. CZK.

Chart 9: Annual volume, number and average amount of mortgages granted between 2020 and 2025

Source: Czech banking association - Hypomonitor

CBA publishes summary statistics for the entire banking market

The Czech Banking Association, in cooperation with its member banks, publishes new aggregate statistics on the housing market. These are mainly the volumes and numbers of newly granted and refinanced mortgages and the respective interest rate. These statistics are published by the CBA in aggregate form for the entire banking sector on a regular basis around the middle of each month. All domestic banks and building societies providing mortgages in the Czech Republic participate in the survey. The data are available from January 2020 in the attached file on the website www.cbaonline.cz, where the relevant statistics can also be found separately for banks and building societies. The above figures are for the sector as a whole, which can also be viewed in a simple graphical form on the website www.cbamonitor.cz.

Methodology of the CBA Hypomonitor

The CBA Hypomonitor divides mortgage loans granted by banks and building societies to households into several categories in order to distinguish new loans from refinanced or internal refixations. New loans are then reported in categories according to the purpose of the loan:

1. new loans

These are loans whose full volume enters the economy for the first time. This category does not include loan consolidations or loan refinancing. It is divided into three categories:

- Purchase of real estate

- Property construction - including property renovation

- Other new arrangements - only new loans that are in no way related to the purchase or construction of the property, e.g. so-called American mortgages, settlement of a JVM, repayment of the purchase price, settlement of an inheritance share, settlement of a cooperative share, etc.

2. Refinanced loans from another financial institution

These are loans that have been originated by refinancing one or more loans from a financial institution other than the reporting one. Irrespective of the amount refinanced and regardless of the amount of any increase, the total amount of the newly originated loan is reported in this category.

3. Loans increased or internally refinanced

These are loans that were already part of the reporting entity's portfolio in the previous reporting period and have undergone one of the following changes during the reporting period:

- an increase in the agreed amount

- changes such that the original loan has been refinanced/converted into a new loan within the reporting entity. This is a genuinely new contract and not, for example, just a new arrangement in the context of a refixation of an existing contract. Therefore, the volume of such loans in the CBA statistics is lower than 'other new arrangements' in the Czech National Bank statistics.

The following banks and building societies provide data for the CBA Hypomonitor: Air Bank, Banka Creditas, Česká spořitelna, ČSOB, ČSOB Stavební spořitelna, Fio banka, Hypoteční banka, Komerční banka, mBank, Modrá pyramida, MONETA Money Bank, MONETA Stavební spořitelna, Oberbank, Partners Banka, Raiffeisen stavební spořitelna, Raiffeisenbank, Stavební spořitelna České spořitelna, UniCredit Bank.