Stronger household incomes outpaced house price growth for six quarters

According to the CSO statistics, property prices, which include land and family houses, rose by 2% quarter-on-quarter in the final quarter of 2025. This slowed from the previous average 2.6% increase in the previous four quarters. Although the income side of demand is still lagging, real household incomes accelerated more sharply at 1.4% q-o-q (up nearly 3% in nominal terms) at the end of last year. And so did the household savings rate, which rose to 19.7%. Moreover, both figures were positively revised and there was a slight positive revision to GDP growth in the final quarter of 2025, albeit with more limited effects on the economic outlook.

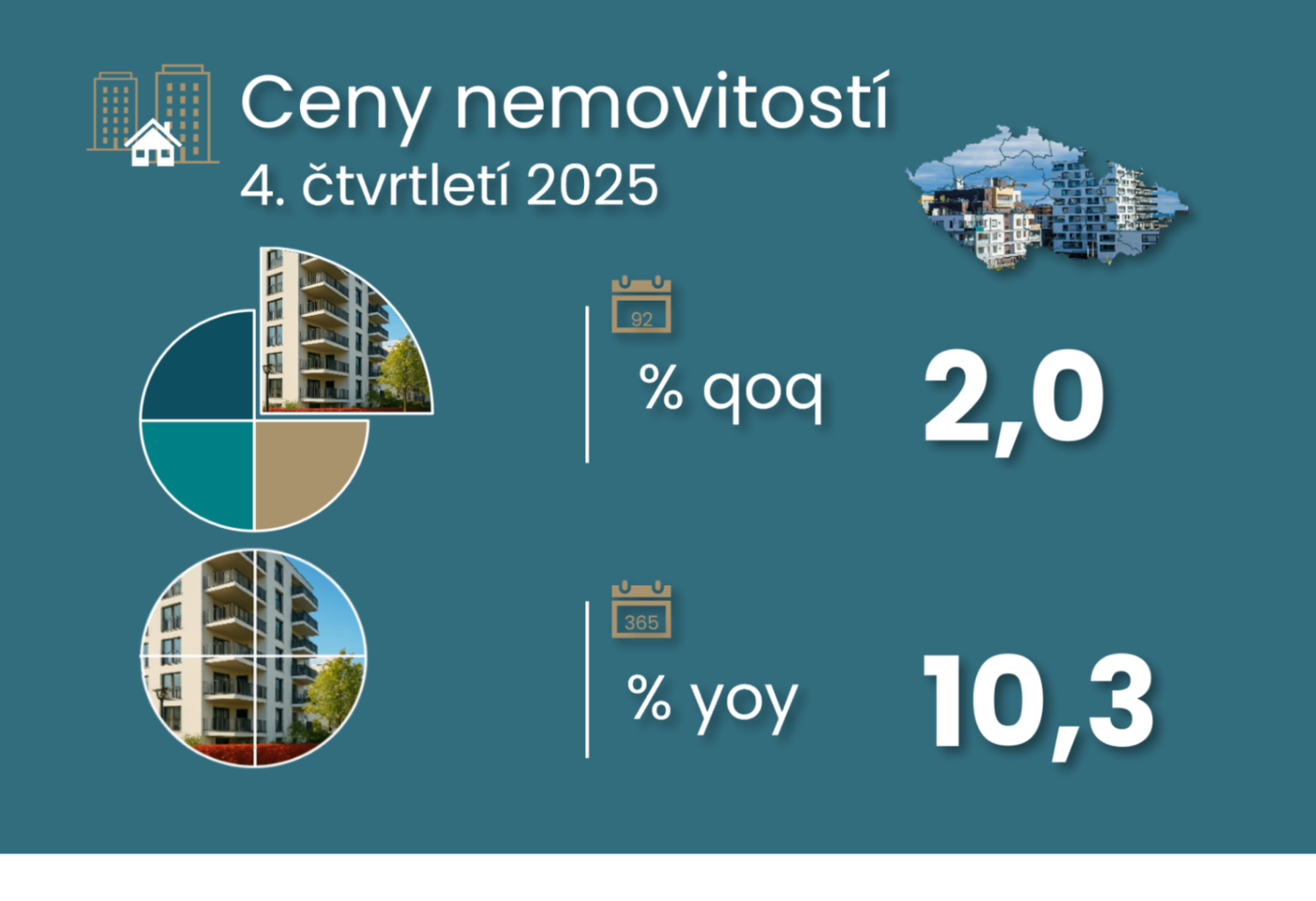

According to the CSU, house prices (HPI) therefore continued to grow at a more moderate but still strong (annualized) rate of 8% after 10% growth in the previous quarter. This slowdown to 2% quarter-on-quarter reflects slower 0.7% growth in Prague after an average 3.5% increase in the previous four quarters. However, older properties still maintained a strong 2.4% pace, the same as the previous quarter's average. This qualitative difference is in line with the slower pace of realised prices (3.7% for older and 0.9% for new in Prague; see dashboard below right for more). The slower quarterly pace also slowed the year-on-year price growth to 10.3% from 10.8% in the previous quarter. The slower quarter-on-quarter pace may pave the way for a gradual return to the 8.5% year-on-year dynamics seen a year ago. However, the renewed increase in the average mortgage amount from the end of this year risks going in the opposite direction (see Chart 8).

HPI statistics in detail: According to the CSO statistics, prices for home purchases (older including land and new, but these are essentially only in Prague - for the rest of the country, see our stats on the CBA Monitor from Flat Zone) have risen 10.3% year-on-year in Q4 2025, having jumped 18.4% in the last three years and 59.3% in the last five years. It's up 150% over the last decade or 167% over the last 15 years. If we look at the cost of owner-occupied properties (i.e. including self-build or self-repair), these have risen by 4.7% year-on-year over the last four quarters, according to CSO statistics, up 7.6% over the last three years and 38.4% over the last 5 years. Over the last decade, it was up 68%, or 81% over the last 15 years. Over those 15 years, this increase in the cost of purchasing property, including self-help and repairs (owner occupied housing), has amounted to a 51% increase in the price of buying a home (the house price index).

Real household incomes strengthened in the fourth quarter. These average disposable incomes rose by 1.4% quarter-on-quarter, having risen by 0.4% on average over the previous two years. This acceleration was supported by continued strong household income growth of 1.4% (see stronger wage growth in the fourth quarter - see report here). This was compounded by a larger quarter-on-quarter change in net property income. On the other hand, fiscal policy was at work, with net taxes (net of welfare and pensions) cutting more from incomes. Its impact (not on disposable income) on real household consumption was moderated by higher social transfers in kind (see the green line in the right-hand graph next to the triple chart below in the "To disposable income and household savings" section).

As a result, household income growth outpaced house price growth in Q4, but this was not the case for older dwellings. Moreover, relative to mid-2024, the increase in average disposable income loses around 7% relative to the increase in house prices.

Coupled with stronger household income and savings numbers, there was a slight positive revision to GDP growth in the final quarter of 2025. This was revised up a tenth to 0.7% quarter-on-quarter and 2.7% year-on-year due to stronger fixed investment growth contrasted with lower government consumption spending. This could have a slight disinflationary impact on the central bank, but it is indeed slight. The positive impact on the forecast is also likely to be slight, as value added growth, on the other hand, was revised down slightly to 0.5% q-o-q and was up 2.7% y-o-y.

Year-on-year momentum was solid at the end of the year, but weaker value added momentum will dampen any positive impact on the economic outlook. The latter will be increasingly affected by the more likely negative effects from the energy supply shock, which will feed through into weaker demand, due to higher prices, but later on the negative consequences associated with the supply shock will start to feed through into external demand, as well as local production.

Stronger household incomes ...

... outpaced house price growth after six quarters, but not for older flats

On property prices

With a 10.4% annual increase in 2025, house prices outperformed the 16-17 increase in 2024, but after a stronger decline in 2024.

The renewed increase in average property values does not bode well for the indicated slowdown in house price growth below 10%

House prices have approximately doubled the growth in prices associated with repairing or self-building

Despite the acceleration of disposable income, its gap to house price dynamics remains significant

On disposable income and household savings

Abnormally high savings rate of Czech households ...

...like in Germany or Hungary

Stronger savings reflect stronger income, boosted in particular by income from employment ...

... which in the post-cide recovery have risen above my estimate of net average wages and salaries with children

Disposable household income was also supported by wages ...

... but also income from assets (here in real terms vs. the CNB rate) ...

... income tax and insurance taxes on gross income slightly more than in the third quarter

On the GDP revision

The stronger quarter-on-quarter growth in GDP at the end of the year reflects stronger tax collections on products ...

... while value added remained at half a percent growth