Consumer price inflation of 2.5% year-over-year in 2025 remained in the middle of the upper half of the CNB’s inflation target tolerance band. Its year-to-date average year-over-year growth of 1.8% so far in 2026 is close to the center of the central bank’s target. Year-over-year growth in core inflation—which accounts for more than half of the consumer basket (excluding food, alcohol, tobacco, energy prices—including fuel—and regulated prices), has so far reached 2.8% in 2026, following 2.7% in the previous year.

Rise in Consumer Prices (Inflation)

(year-over-year figures, % yoy)

CBA Monitor

You can hide a data set by clicking on the data set name in the chart legend.

Source of primary data

Czech Statistical Office

Category

Economy

Data Frequency

annual

Note

Annual average and year-to-date average for the current year.

Data not adjusted for variations in the number of working days or seasonal factors.

While the acceleration in consumer price growth to 1.7% in July was likely accompanied by a return of demand-driven core inflation to 2.9%, this signals a further slight slowdown in its monthly momentum. Furthermore, retail sales declined slightly in June. This combination gives the central bank room to keep interest rates at the current level of 3.75%. However, core inflation remains above the central bank’s inflation target, which will keep it vigilant and open to another interest rate hike to 4%. This is especially true if August consumer prices continue the stronger momentum seen in July.

Jaromír Šindel

10. 06. 2026

Consumer price inflation slowed to 2.1% year on year in May, close to the CNB's target. However, domestic inflationary pressures continue to operate beneath the surface. Core inflation remained at 2.9% y/y and its short-term dynamics suggest an acceleration closer to 4%. The latest economic numbers do not suggest a reversal and thus a relief of the inflationary nature of the Czech economy due to strong wage growth and weak productivity growth. This constellation, together with the ongoing Iranian conflict, reinforces the rationale for a 0.25 percentage point increase in the central bank's interest rate to 3.75% at the June meeting. This will not be an easy decision for the Board.

Jaromír Šindel

04. 06. 2026

Consumer price inflation slowed to 2.1% in May, surprising at a more moderate pace than the market had expected. However, some of the factors now dampening inflation may not be permanent. This is particularly true for food prices, which may be affected by rising global commodity prices in the months ahead. At the same time, strong wage growth of 8.1% year-on-year is divorced from labour productivity, creating pressures for higher core inflation. It is the contradiction between low headline inflation and persistent domestic inflationary pressures that poses a non-trivial economic and political dilemma for the CNB.

Jaromír Šindel

06. 05. 2026

April consumer prices accelerated to 2.5% year-on-year and the story behind the inflation numbers is very similar to March. The acceleration mainly reflects higher fuel prices, but higher core demand inflation and, more recently, higher alcohol and tobacco prices are also creeping in. While energy and food prices still dampened the acceleration. The current dynamics and the Iranian conflict pose a risk of higher inflation for this year, and for the outlook for next year. While risks to the forecast remain volatile due to the uncertainty associated with the Iranian conflict, even if it calms down, higher core inflation represents a hawkish signal for the CNB in the form of a higher interest rate.

Jaromír Šindel

14. 04. 2026

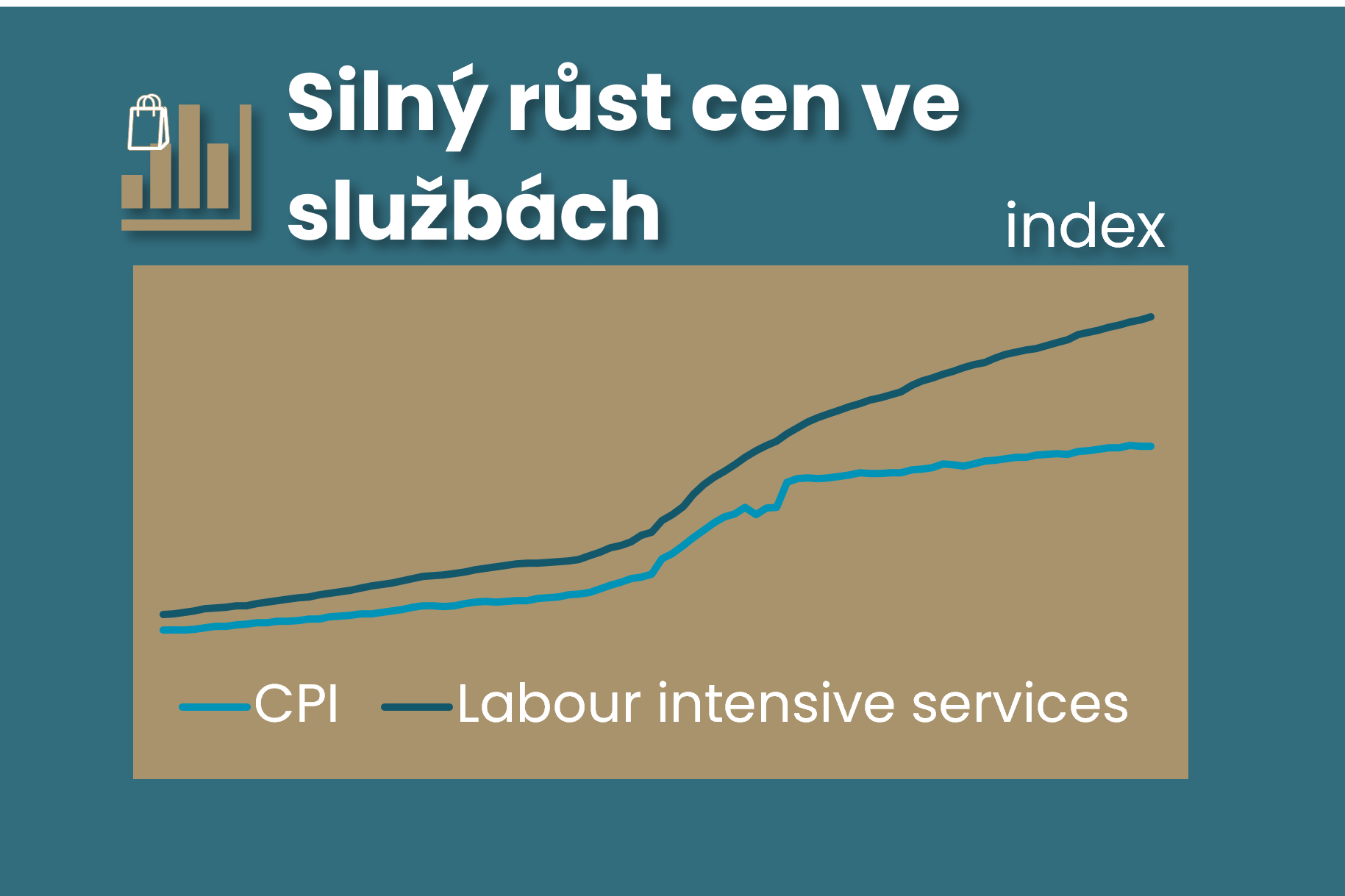

The March acceleration in consumer price inflation to 1.9% was not surprising in itself, but the acceleration in core inflation to 2.9% was less favourable, including the momentum across key segments. This indicates that price pressures in the domestic economy remain strong, especially for labour-intensive services and imputed rents, but also the koruna no longer provides a disinflationary factor for goods prices, amid strong household demand. For the Czech National Bank, the March core inflation is a hawkish signal that may reinforce interest rate growth expectations, especially if the current energy shock persists.

Jaromír Šindel

07. 04. 2026

March inflation accelerated to 1.9% year-on-year in March, mainly reflecting higher fuel prices. However, the acceleration was somewhat milder than expected, helped by lower food prices. However, preliminary data suggest an acceleration in core inflation to 2.8%, which is not surprising given the still strong growth in retail sales. Although these did slightly correct the previous strong increase in January in the core segment in February. However, the strength of demand is relatively limited given the rather sluggish sales in services in the first two months of the year. The central bank will monitor the dynamics of these demand pressures, wages and core inflation, which will determine the speed and extent of its interest rate hikes in the coming months. Stronger demand is also translating into more robust imports, shrinking the foreign trade surplus that has not yet been affected by the energy price shock.

04. 03. 2026

Comment by Jaromír Šindel, Chief Economist of the CBA: February consumer inflation pleasantly surprised the consensus and the central bank by slowing to 1.4% year-on-year. The inflation was mainly helped by a further decline in food prices, but also by a slightly milder rise in services prices. However, the energy shock due to the Iran war, together with still higher core inflation, is likely to pull annual consumer price growth back to an average 1.7% for the rest of the half-year. Details on core inflation, and hence services prices, will be important for both the inflation outlook and the central bank's interest rate outlook in the context of continued wage and unit labour cost growth (see charts below for market developments).

13. 02. 2026

Comment by Jaromír Šindel, Chief Economist of the CBA: January's significant slowdown in consumer prices to 1.6% year-on-year mainly reflected the transfer of contributions for renewable energy from household invoices to the state budget. By contrast, core inflation eased slightly to 2.7% y/y from 2.8% at the end of last year. Food prices, which had contributed significantly to the moderation of inflation at the end of last year, rose in January, but less than would have been seasonally consistent. Consumer price growth is expected to reach around 1.7% yoy this year, following a 2.5% rise in 2025, but with core inflation still rising at around 2.5%, this will also require a disinflationary impulse, which is not yet coming from the property market segment, for example. Higher core inflation should keep the CNB interest rate steady at 3.5%, although the market is pricing in a slight cut, as are half of the CBA forecast panelists.

05. 02. 2026

Comment by Jaromír Šindel, Chief Economist of the CBA: The significant slowdown in consumer prices to 1.6% year on year in January did not surprise the consensus and mainly reflects lower energy prices, but also food and fuel prices. On the contrary, I expect core inflation to remain at at least 2.8% growth from the end of last year. Although core retail sales corrected with a 0.6% month-on-month decline in December, annualized momentum, along with household plans, remains strong and does not suggest easing demand pressures. Thus, even in light of fiscal plans, interest rate stability appears to be an appropriate stance for the central bank, at least for the coming months. This is inconsistent with interest rate market targeting, but in my view this would require significantly lower core inflation pressures.

29. 01. 2026

Comment by Jaromír Šindel, Chief Economist of the CBA: The analysis summarizes the government's regulatory steps that will further slow consumer price growth this year, probably well below 2%. What does this mean for the CBA, which seems to be starting to deflate the pigeon balloons, at least more than at the end of last year? Given its earlier communications, where inflation is headed in 2027 should be key, which will also indicate the direction of core inflation in the months ahead. And it is not just the case of still strongly rising services prices that are the focus of this analysis, the first part of the triptych ahead of the CNB's February board meeting.

07. 01. 2026

December inflation in the Czech Republic remained at 2.1% year-on-year and was lower than expected by the Czech National Bank and the market. Developments in food and energy prices helped keep headline inflation low, while core inflation is likely to have rebounded to 2.8% after a slowdown in November. However, both figures still missed the CNB's outlook, and this is likely to be repeated this year. This should dampen the upside risk to the central bank's interest rate, but it will remain impatient in waiting to see how fiscal policy affects the economy and inflation through 2027.

10. 12. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: November consumer price growth did not slow to 2.1% year-on-year only thanks to volatile food prices, which were lower in November. The slowdown in core inflation to 2.6% was probably also due to lower prices for holidays, clothing, household furnishings, as well as lower prices in healthcare and energy. This, and November's move closer to the price inflation target for both headline and core inflation, eases hawkish pressures on the central bank. However, the continued brisk momentum in rent and food and other service prices will not allow the central bank to contemplate an interest rate cut.

04. 12. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: Consumer price growth slowed to 2.1% yoy in November. The main reason was a deeper decline in food prices, partly due to a slowdown in core inflation from the recent 2.8%. Thus, although inflation surprised positively, food price volatility and still strong rapid wage growth of 7.1% in Q3 will dampen the CNB's willingness to return to rate cuts. And the same reasons dampen the risks to the CBA's outlook for consumer inflation next year at around 2.2%. There remains a significant gap in the recovery in real gross wages between the market and non-market sectors.

11. 11. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: October consumer inflation not only confirmed a more pronounced shock from higher food prices, but also showed higher prices of transport services and prices of means of transport as part of core inflation. In the longer term, it is worth noting that imputed rental prices have already caught up with the previous inflation shock, and the same has been true for a few months for holiday prices. Thus, the higher October inflation and unemployment data will not help the central bank or the market resolve its dilemma of the next interest rate move.

05. 11. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: The return of consumer price inflation to 2.5% in October will keep the CNB vigilant. Although this was due to higher food prices, the current core inflation rate remains slightly above the inflation target, which will probably be evident next spring. Although selected plans of the new coalition will help to further tame price rises, others are more likely to maintain an inflationary undercurrent in the economy.

10. 10. 2025

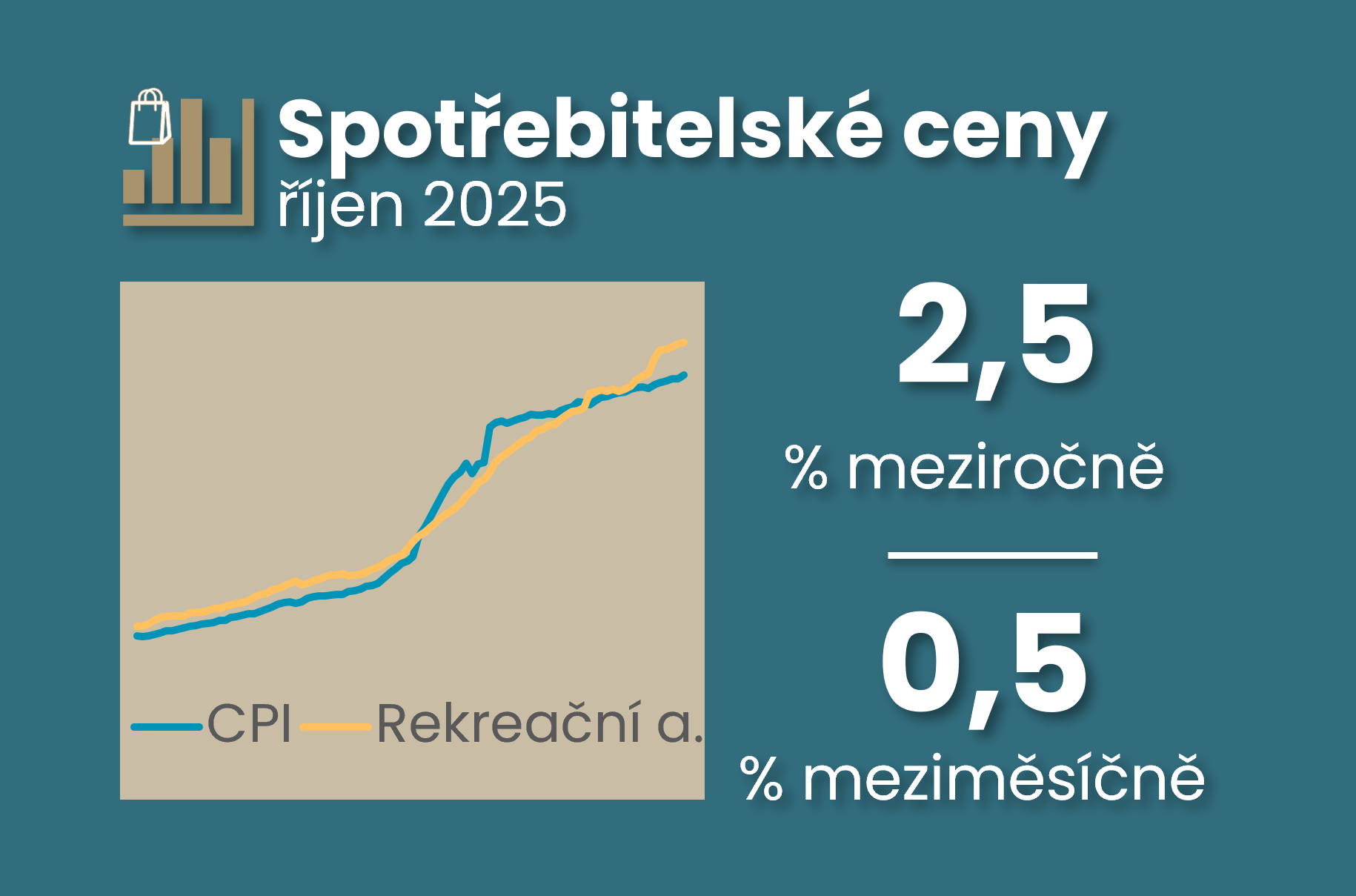

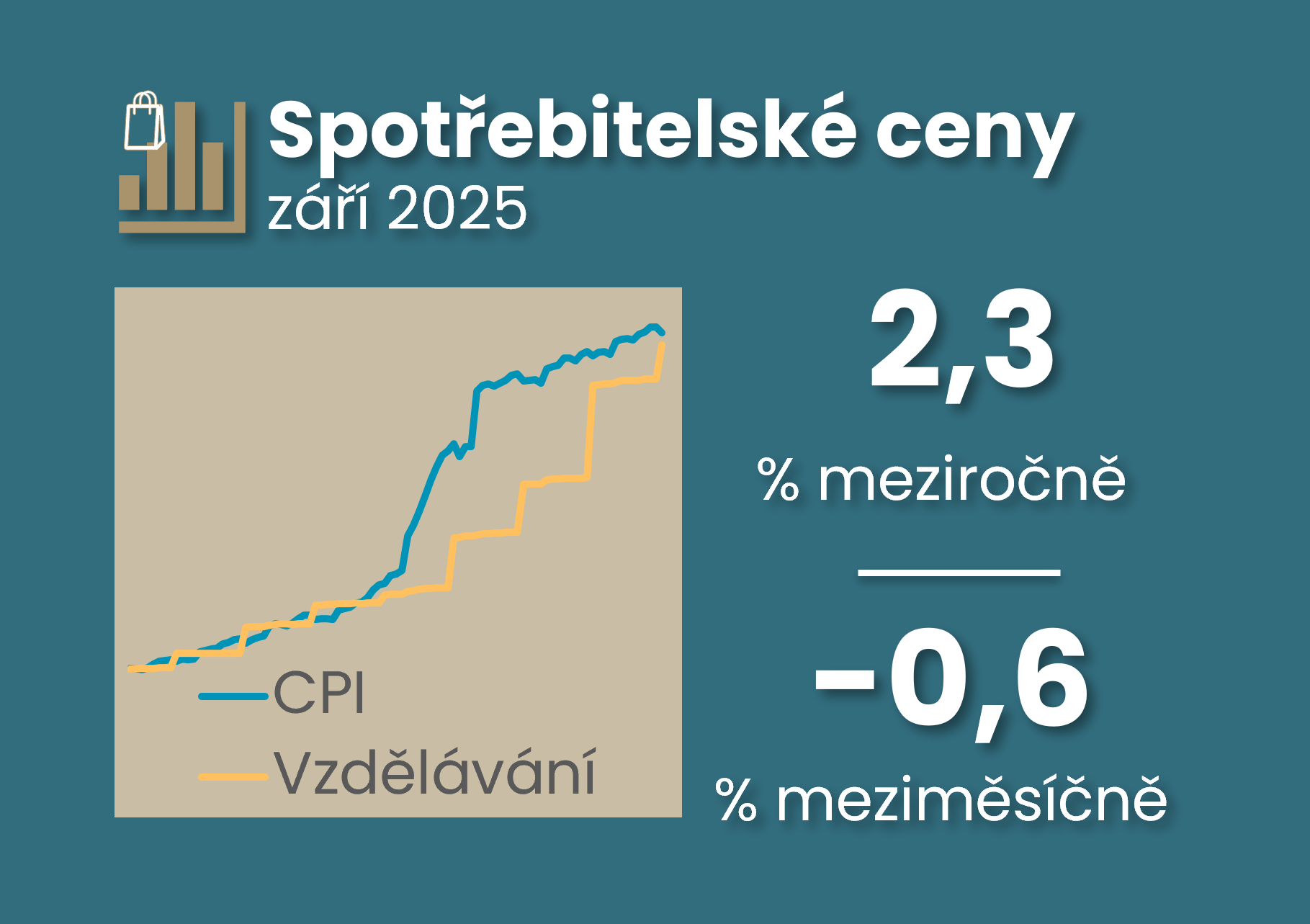

Comment by Jaromír Šindel, Chief Economist of the CBA: Lower food prices, a seasonal decline in holiday prices and a slight catch-up in education prices contributed to September's more moderate consumer price growth of 2.3%, which, however, reminds us of possible price catch-up in other segments next year as well (see Chart 4).

06. 10. 2025

Comment by Jaromír Šindel, Chief Economist of the CBA: The more pronounced slowdown in September consumer price growth to 2.3% year on year reflects a decline in most components of the consumer basket. There are three messages for the CNB that are likely to leave the CNB's communication unchanged, i.e. open to all interest rate possibilities.

18. 09. 2025

Commentary by Jaromír Šindel, Chief Economist of the CBA: Higher-than-expected wage growth will be the main, but not the only, reason for keeping the interest rate at 3.5% at the CNB's September meeting and for the intensification of the hawkish tone in the communication. The latter may indeed indicate a further upward movement in the interest rate, but rather in an unspecified distant horizon. A stronger koruna or tighter monetary policy through the longer end of the yield curve is unlikely to lead the CNB to a dovish mindset.

10. 09. 2025

Economic commentary by Jaromír Šindel, Chief Economist of the CBA: CPI growth slowed to 2.5% yoy in August, but core inflation accelerated slightly to 2.8% in line with the CNB's forecast. The core services price segment, excluding imputed rent, accelerated month-on-month in August, but its three-month average remains well below the pace observed in H1-2025.

08. 08. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA (adjusted for published data on core inflation from the CNB and registered unemployment data, 18:00 8 August)

10. 07. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

04. 07. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

11. 06. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

04. 06. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

13. 05. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

07. 05. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

06. 05. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

10. 04. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

04. 04. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

12. 03. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

05. 03. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

13. 02. 2025

Economic commentary by Jaromir Šindel, Chief Economist of the CBA

10. 09. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

12. 08. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

10. 07. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

11. 06. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

13. 05. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

10. 04. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

01. 02. 2024

Interview with Jakub Seidler, Chief Economist of the Czech Banking Association

19. 01. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA

17. 01. 2024

Economic commentary by Jakub Seidler, Chief Economist of the CBA