Wages closed stronger last year and could add another 4% in real terms this year

Wage growth remained strong at the end of 2025. Average wages rose by 7.4% year-on-year and added 7.2% for the year as a whole. Thanks to low inflation, this meant real wage growth of 4.7%, higher than forecast. While nominal growth should slow this year, real wages may continue to grow solidly. The average nominal wage reached CZK 49.2 thousand last year, surpassing CZK 50 thousand at the end of the year on a seasonally adjusted basis and reaching almost CZK 51 thousand in market sectors. The median wage of CZK 42 thousand was approximately 85% of the average wage.

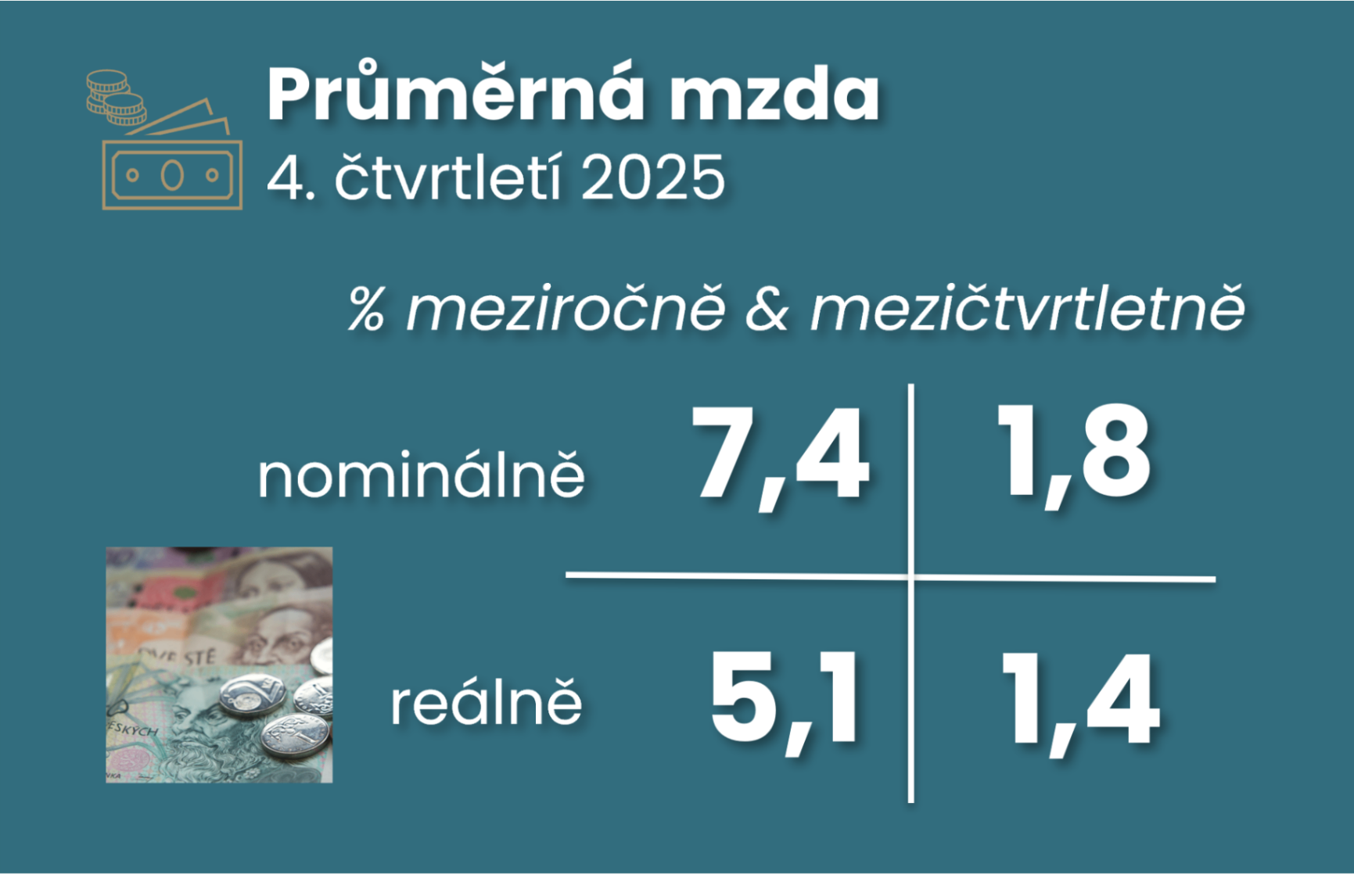

Average nominal wage growth in the final quarter of last year, according to wage statistics, did not reach the 8% increase suggested by the national accounts, but maintained strong quarter-on-quarter growth of 1.8% (seasonally adjusted). However, this still led to an acceleration in annual growth to 7.4% from 7.1% in the previous quarter. Average wage growth thus slightly exceeded the central bank's 7.1% estimate, which had also expected a more moderate acceleration in unit labour costs in the economy in Q4.

The quarter-on-quarter increase of 1.8% on average persisted throughout last year and was supported in the fourth quarter by industry, construction and agriculture (after weak growth in the previous quarter), as well as administrative activities and continued strong momentum in real estate. In contrast, finance or healthcare posted weaker growth, which is also true for education after a strong increase at the beginning of the year.

On a positive but also inflationary note, median wage growth accelerated to 8.4% year-on-year at the end of last year, reflecting its stronger but more volatile quarter-on-quarter dynamics. However, its average growth of 2.2% last year outpaced the 1.8% quarter-on-quarter pace of average wages. And this was the same for both market and non-market sectors.

So 2025 maintained a strong full-year wage growth rate of 7.2% y-o-y, the same as the year before and the year before that. And with consumer price growth accelerating only marginally to 2.5% in 2025 from 2.4%, the real rate maintained its 4.7% growth. This beat the CBA forecast (4.4%) and slightly beat the CNB forecast (4.6%).

The CBA forecast for this year is for a more moderate increase in nominal average wages of 5.8%, slightly below the central bank's outlook (6.2%). The outlook for more moderate consumer inflation at 1.7% this year should then result in still strong real wage growth of 4% y/y. This should underpin still robust private consumption with a near 3% strengthening this year. Risks to the inflation outlook are both ways (see the commentary on the February numbers for more detail).

Thus, real gross wages are slightly above pre-pandemic levels (+0.3%) and slightly more so for the median (+1.5%). Market wages are also slightly higher in real terms (+2.2%), while non-market wages remain well below pre-pandemic levels (-7.3%; we compare seasonally adjusted data here with Q4 2019). However, real wages still fall short of their Q2 2021 peak. They lost 3% to it by the end of 2025.

In the case of net wages, I estimate that they close 2025 more than 5.3% above the pre-pandemic level, or nearly 2.5% in the simulation with two children, but still more than 3% below it in the case of two children, daycare, and a wife with income below 70k per year.