Consumption, wages and industry dragged GDP growth, but do not favour a fall in interest rates

Comment by Jaromír Šindel, Chief Economist of the Czech Bank of Economics: The Czech economy closed last year with stronger growth than originally expected. The Czech economy could repeat its 2.6% annual growth this year. Household consumption was the driving force at the end of last year, supported by stronger wage growth, but also by strong growth in manufacturing. However, higher wage costs have far outpaced productivity growth, and so still elevated core inflation will remain the central bank's focus, which should result in the CNB interest rate holding steady at 3.5%.

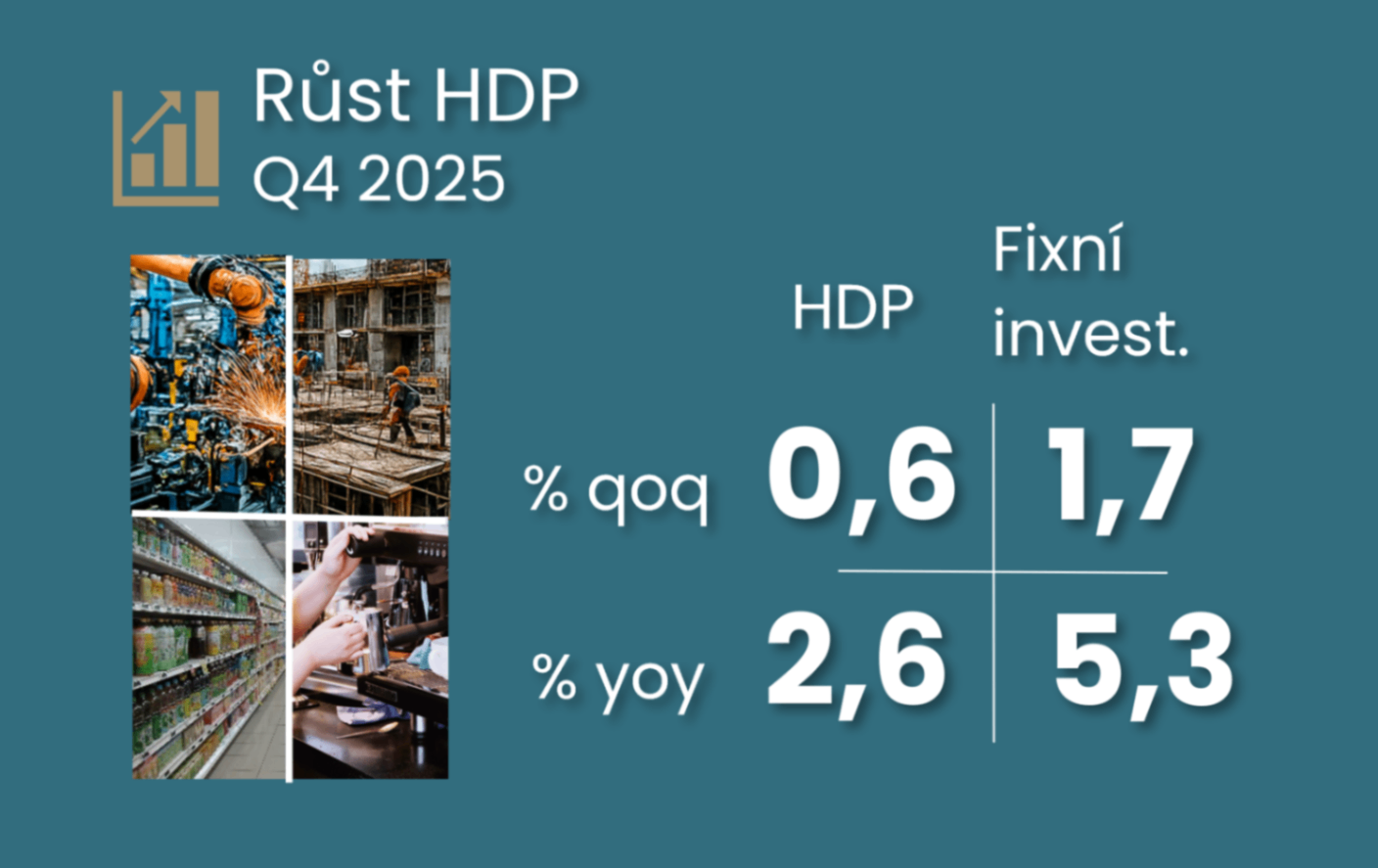

The performance of the economy closed last year with a slightly better growth of 0.6% q-o-q (+0.1 p.p. compared to the flash estimate). As a result, annual growth accelerated to 2.6% in the final quarter, which was also the average growth in 2025 after 1.1% in the previous year. Unsurprisingly, the solid growth of more than half a per cent quarter-on-quarter in the final quarter of 2025 was underpinned by stronger growth in household consumption (1.3% quarter-on-quarter) and a strong 2.2% increase in manufacturing value added.

Continued stronger government consumption (1%) added to this. Fixed capital formation also surprised positively, growing at a brisker 1.7%, along with an overall positive revision in fixed investment. At the same time, this was accompanied this time by a rebound in investment in machinery and equipment, while the construction part, again given the stagnation in the monthly construction numbers, declined slightly. Given the solid industrial performance, the economy also leaned on a slightly positive contribution from foreign trade. Exports maintained solid growth of 0.8% quarter-on-quarter (with nearly 2% growth in exports of goods), which offset a 0.6% acceleration in imports.

Figures from the final quarter of last year send a rather hawkish message to the central bank, which favours interest rate stability over expectations of an early decline. While growth in GDP levels is in line with the CNB's forecast, both household and government consumption are stronger. At the same time, the fourth quarter figures brought higher growth in unit labour costs, thanks to stronger wage growth in the economy (2.8% quarter-on-quarter and 8% year-on-year). Although productivity per employee rose by 0.6% qoq (1.5% yoy), the number of hours worked rose with it (1.2% qoq and 2.9% yoy). As a result, productivity per hour worked fell again, this time by 0.5% qoq and 0.4% yoy.

This, in constellation with the current geopolitical shock in energy prices, should keep the central bank's focus on bringing core inflation closer to its target. Core inflation, heavily influenced by demand and the labour market, rose 2.8% y/y in January, in contrast to the 1.6% rise in headline consumer inflation.

The CBA forecast calls for continued strong GDP growth of 2.6% y/y this year. Growth should be underpinned by continued strong growth in household consumption (2.8%), where we see two conflicting risks - rising unemployment (the January reading of 3.3% is 0.6pp higher than a year ago) vs. higher wage growth and stronger government support. This is compounded in our outlook by continued growth in government consumption (2.2%). Given the positive revision to fixed investment, we may see it recover more modestly than our expected 3.2% y/y after 0.9% in 2025, as fixed investment actually rose 2% last year.

Accelerating private consumption and investment drove GDP growth at the end of last year

On the supply side, it was manufacturing that compensated for weaker services and a decline in value added in construction

A complete post-caucus recovery thanks to the return of private consumption to pre-pandemic levels ...

... and on the supply side, the recovery was mostly about private and public services, while the slump in value added in the energy sector remained in place

The recovery in real GDP growth has been accompanied by strong growth in unit labour costs ...

... because the economic recovery was first associated with rising employment and then higher employee utilisation (more hours worked per worker), but productivity growth remained weak and even deteriorated per hour worked

Stronger wage growth at the end of last year ...

... thus resulted in stronger growth in unit labour costs than expected by the CNB, and this also applies to growth in private and government consumption

The year 2025, despite the original data, brought stronger growth in fixed investment and a slight recovery in investment in machinery and equipment thanks to the revision