Strong pace of growth in supply prices of flats also at the beginning of 2026

In Q1 2026, the offer prices of flats rose by 2.7% quarter-on-quarter. The housing market is slowing down slightly in terms of offer prices after last year's significant increase in prices, but price growth remains above average and is not sufficient to improve the ratio of housing prices to household incomes significantly. In the regions, prices continue to rise faster than in Prague and the year-on-year cooling is still evident in Prague. Overall annual growth in the supply side of house prices has slowed to 12.9% from the previous 16-18% during 2025. Higher supply side house prices have been heralded by continued growth in average mortgage rates.

In Q1 2026, apartment offer prices rose by 2.7% quarter-on-quarter. While this represents a slight acceleration from 2.4% at the end of 2025, the pace remains below the 2025 average (4.0%). Last year's average reflected a strong market awakening in Prague in Q1 and in the regions in Q2 and Q3. Although the market is stabilising growth after last year's jump in prices, it is still at a high pace, i.e. well above long-term averages (see Chart 3 below). Regionally, the dynamics remain different - outside Prague, prices grew faster (+3.1%), while Prague slowed to 2.4%.

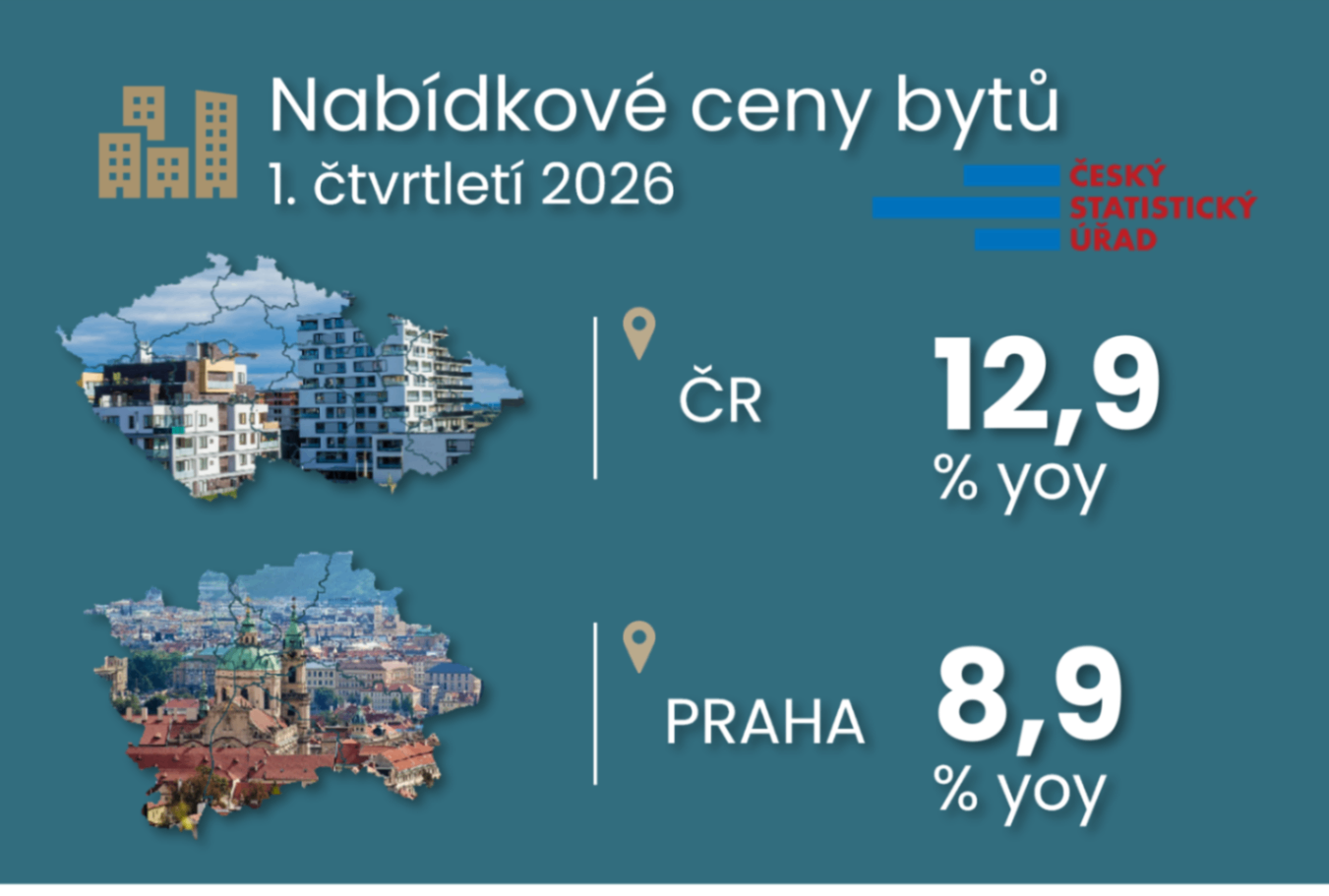

In annual terms, there has been a visible cooling, but insufficient in terms of the ratio to disposable income. Year-on-year growth in housing supply prices has slowed to 12.9% from the previous 16-18% over 2025 (see summary table below). This decline is particularly noticeable in Prague (to 8.9% from an average of 15.9%), while in the regions the pace remained virtually unchanged at 17.7% relative to last year, albeit slowing from a pace of over 19% in its second half. However, quarter-on-quarter growth remains strong. It implies future potential growth still around 8% in Prague and around 12% in the regions.

The still strong quarter-on-quarter pace of house price growth, here so far only in the supply segment, is not a big surprise given the ever-increasing pace of average mortgage amounts. During February, the mortgage rate for actual new mortgages exceeded CZK 4.6 million. The average so far in the first quarter suggests a 5% increase quarter-on-quarter and over 15% year-on-year.

Housing supply prices have only moderated their otherwise still strong growth rate, which does not significantly reduce the deviation from household disposable income

The current quarter-on-quarter momentum in house price growth is outpacing the long-term average ...

... which also holds for the annual growth rate

Causality between asking and realized prices of apartments has not been evident in recent years, which is not true for the correlation

The continued strong pace of growth in housing supply prices is not surprising given the ever-increasing average mortgage rate.