CBA Hypomonitor: April also rewrote mortgage highs with still low rate of 4.52%

Average mortgage rate rises to 4.52%

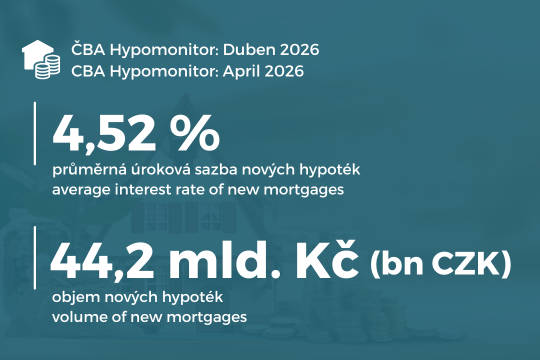

Prague, 18 May 2025 - In April 2026, banks and building societies granted new mortgages without refinancing for CZK 44.2 billion. Since the beginning of the year, their volume has reached CZK 141 billion, i.e. CZK 48 billion more than a year ago. Added to this is the strong volume of refinanced mortgages, which accounted for 28% of the total almost 62 billion in new mortgage business in April. Despite the jump in market interest rates, the average realised interest rate on new mortgages has so far risen marginally to 4.52% from 4.43% in March. The above information comes from the CBA Hypomonitor, which captures data from all domestic banks and building societies providing mortgage loans.

The rise in market interest rates is likely to have contributed to a further frontloading effect with ever lower interest rates following the frontloading effect due to the CNB's tightening of conditions for so-called investment mortgages in April. This was probably reflected in a higher average mortgage size. It rose slightly to CZK 4.9 million in April. This increase was also reflected in a higher monthly instalment, which reached CZK 26,000 in April for a newly granted mortgage and almost CZK 21,000 for the median mortgage.

The next CNB meeting related to the setting of macroprudential mortgage policy will take place on 4 June, following March's relatively hawkish comments on the setting of the current 1.25% countercyclical capital buffer (subsequent meetings will be held on 10 September and 26 November).

Table 1: Summary of mortgage origination volumes and average interest rates for April 2026

|

|

Monthly values |

|

year-to-date values |

||||

|

|

Volume |

Number |

Rate |

|

Volume |

Number |

Rate |

|

|

|

||||||

|

Total |

61,5 |

13 396 |

4,49 |

|

192,7 |

42 985 |

4,46 |

|

New loans |

44,2 |

9 049 |

4,52 |

|

141,3 |

29 856 |

4,48 |

|

of which: |

|

|

|

|

|

|

|

|

for purchase |

29,9 |

6 166 |

4,52 |

|

103,3 |

21 882 |

4,47 |

|

for construction |

7,7 |

1 623 |

4,45 |

|

21,7 |

4 631 |

4,43 |

|

Other |

6,6 |

1 260 |

4,58 |

|

16,3 |

3 343 |

4,54 |

|

Refinanced from another institution |

14,5 |

3 696 |

4,41 |

|

43,2 |

11 110 |

4,41 |

|

Refinanced internally, increased |

2,7 |

651 |

4,45 |

|

8,2 |

2 019 |

4,43 |

Source. Note: seasonally unadjusted data

"The strong April figures were probably due to a double factor of frontloading, probably with the reverberations of the April tightening of conditions for investment mortgages, but also to the desire to avoid higher interest rates, as April brought a slight increase in mortgage interest rates compared to the jump in market interest rates," believes Jaromír Šindel, chief economist at the Czech Banking Association.

Mortgages pre-arranged in March are likely to have still made it into the April figures

Overall, banks and building societies reported new unconsolidated business in the form of new and refinanced mortgages in April in the amount of CZK 61.5 billion, which is 11% more than a month ago. It was up 90% year-on-year. Their total volume so far this year has reached CZK 193 billion, a 70% increase compared to January-April of the previous year.

In April, banks and building societies actually granted new mortgage loans without refinancing for CZK 44.2 billion. Compared to March, new mortgage activity thus rose by around 10% in volume terms, while the usually strong seasonal upturn in March is partly corrected in April. On a seasonally adjusted basis, April's new mortgage numbers brought a 13.2% improvement to CZK 40.5bn compared to March's CZK 35.8bn, while being above the average volume of the previous three months (CZK 35bn). The volume of new mortgages granted in April was up by around 67% compared to the first half of last year. In year-on-year terms, the growth in the volume of mortgage originations picked up again in April to 69% from 49% in March, following an average 41% year-on-year increase last year. Around 73% of new lending this year has been for purchase and 15% for construction, while the share of the other category, which in some cases includes so-called non-real estate mortgages, rose to 12%.

The number of new mortgages rose 8% month-on-month to 9,049 in April, up 41% from a year ago. We estimate the seasonally adjusted number to be around 8,533, about 15% above the average number (7,431) in the previous three months. Year-to-date, the number of new mortgages has reached 29.9 thousand (+28.5% yoy). The dynamics of the number of new mortgages from the last three months, i.e. for February to April, implies an increase to a total of around 92.7 thousand this year, which would be close to the average numbers of around 92 thousand from 2016 to 2018, but still well below the 114 thousand of 2021. But after the CNB's tightening of conditions in April, fewer new mortgages can be expected. These would then, with a 7% correction, close this year at around 79k, up 3.5% on last year.

"The main event of the past two months has been the uncertainty about the development of resource prices, which affects mortgage rates. The cost of resources has risen significantly due to geopolitical risks from March 2026. The rise in interest rates is an unpleasant surprise for clients whose interest rate fixation will end in 2026.Rates 5 years ago were around 2.5%, while now they are hitting the 5% mark," adds Marian Holub, housing finance expert at Česká spořitelna.

Chart 2: New mortgage originations excluding refinancing

The beginning of this year showed strong above-average volumes, even as a percentage of the economy's performance.

Source: Czech Banking Association, CNB, CSO, Flat Zone.

Chart 3: Average mortgage amount by purpose

In April, it rose by 2% to CZK 4.89 million. This means a 20% year-on-year increase of CZK 815 thousand.

Source: CNB, CBA Hypomonitor

The share of refinanced and increased loans continues to grow despite increasingly strong volumes of new mortgages. The volume of refinanced and increased loans (internally or from another institution) rose to CZK 17.2 billion in April. This is 143% higher than the average 7.1 billion refinanced last year and more than triple the 3.9 billion refinanced in 2024. The share of refinanced loans in total mortgage originations then rose further to 28%, above last year's average of 20.7%, but not far off the 29% share from 2020-2021, when households refinanced at a mortgage rate of 2.14%. In April 2026, households refinanced at a rate of 4.42%, still 0.16 percentage points below the 4.58% rate a year ago. The higher refinancing volumes reflect the confluence of expiring longer fixings from the low interest rate period and shorter fixings from the recent period of higher interest rates. For a closer look at the rising wave of refinancing, see CBA Focus: Wave of mortgage refinancing intensifies, but interest rate shock fades. Higher inflation remains a risk.

"The April and May interest rate developments show that mortgage rates today are not only reacting to the actions of the CBR, but increasingly also to movements in market rates and swaps.Expectations of mortgage cheapening are therefore partly shifting and banks remain cautious," notes Soňa Holíková, mBank's mortgage product manager.

The average mortgage rate rose to 4.52% in April, so far only partly reflecting the jump in market rates

The average realised interest rate on new mortgages rose "slightly" to 4.52% in April from 4.43% in March. Its month-on-month increase of 0.09 p.p. thus only partly reflected the previous rise in market rates. Its April level was still 0.13 percentage point lower than the 4.65% rate a year ago, which reduces monthly mortgage payments by around CZK 400, or 0.4% of the applicant's net income. By comparison, the average mortgage rate in 2025 was 4.58% compared to 5.07% in 2024.

At 4.52%, the April mortgage rate was 0.42 percentage points above average market swap rates. This is about 0.63 p.p. below the long-term average since 2014 (1.05 p.p.). While in the previous three months this spread to the long-term average was nearly 1 p.p. in January and February, it narrowed to 0.34 p.p. in March. April's level of mortgage rates, compared to the average swap rates from the first half of May, would narrow this gap to a quarter percentage point. In our study, we pointed to structural factors, particularly the strength of demand in a competitive market, that affect the effect of market interest rates on mortgage rates.

Czech market longer-term interest rates, [1] which are a key influence on mortgage rates, were very volatile during April and March, but they were stable at around 4.1% for three-year swaps and around 4.19% for five-year swaps. This is around 0.6 p.p. above the February value, which, in turn, had priced in a slight fall in the CNB interest rate. This changed significantly with the Iran war, as the shock to energy commodity prices, as well as still high core inflation, eliminated the dovish tone from the central bank's communication (for a closer look, see The CNB's new outlook for higher rates has "only" morphed into hawkish communication). Euro five-year swaps rose to 2.85% in April from 2.74% in March and were 0.51 bps above their average level last year of 2.34%. US five-year interest rate swaps rose to 3.89% in April from 3.8% in March and were 0.03 bps above their average level in 2025.

[1] These are mainly long-dated interest rate swaps (IRS), which reflect the cost of money at longer maturities, around 3 to 5 years in recent years, but the whole 2 to 10 year curve remains relevant, although 10 year maturities are less relevant due to higher central bank rates compared to the previous decade, but also due to the expedient cost of prepaying mortgages.

Chart 4: Average Mortgage Interest Rate - New Business

April mortgage rates began to slightly reflect the rise in market rates ...

Source: CNB, CBA Hypomonitor

Chart 5: US attack on Iran has significantly increased market swap interest rates

... which remain at mid-2024 levels due to the unresolved Hormuz Strait

Source: LSEG, Macrobond (May 14, 2026), CBA

Impact on the average monthly mortgage payment of over CZK 26,000, but with a median of CZK 21,000

The combination of a still lower interest rate and a higher average mortgage amount in April 2026 have increased the current average monthly payment of a newly granted mortgage by CZK 3.5k.The scenarios of the evolution of the monthly payment for different mortgage maturities are shown in Table 2. It suggests that a fall in mortgage rates of almost 0.1 percentage point relative to their average rate of 4.58% in 2025 would, for an average mortgage size with a typical repayment term of around 26.8 years, reduce the monthly repayment by less than CZK 200 to around CZK 26,2 thousand. This represents a reduction of CZK 200,200, i.e. 0.2% of the applicant's net income compared to the average repayment in the previous year.

Thus,compared to the average 2.33% mortgage rate for new mortgages in 2021 , the current refinance mortgage rate of 4.42% for a shortened loan term raises the monthly payments on an average mortgage by more than CZK 3,000, or about 5.8% of the current average gross salary. We discussed the impact and circumstances in Focus CBA: Wave of mortgage refixations intensifies, but interest rate shock fades. Higher inflation remains a risk.

Table 2: Illustration of the average and median monthly mortgage payment by maturity and interest rate

Source: CBA (a table with values is available in the xls file attached to this report)

The average size of a newly granted mortgage has increased with April's 4.89 million. CZK is on a growth trajectory

The average size of an actual newly granted mortgage rose slightly to CZK 4.89 million in April. CZK, i.e. by almost 2% month-on-month. Its size is thus 20% higher than the CZK 4.07 million in the same period last year. CZK a year ago. The higher average mortgage size at the beginning of this year probably reflects the fading effect of frontloading on so-called investment mortgages, where the CNB has tightened requirements since April (LTV to 70% and DTI to 7x). At the same time, the frontloading effect is also likely to be relevant due to the break in market interest rates, i.e. the use of ever lower mortgage rates. The gradual rise in real household wages (5.1% y/y in Q4-2025; charted here) also acts as a backdrop.

Mortgage rates are then also linked to house price developments, which continued to grow strongly at almost 11% y/y in Q4-2025. Offer prices accelerated slightly to 2.7% q-o-q in Q1 2025, still above their long-term average increase of 1.8%. According to data from Flat Zone, the average transaction price of both new and older apartments in the country reached 97.5k in Q4 2025. This reflects a 2% quarter-on-quarter and 11.3% year-on-year increase.

Chart 6: Illustrative comparison of the monthly instalment for the current average newly granted mortgage with a year ago, depending on the interest rate, mortgage size and maturity in years

In a year-on-year comparison, the fall in the mortgage rate resulted in a saving of CZK 360 in the average monthly instalment, but the increase in the average mortgage amount caused an increase of CZK 4 370.

Source. Note: Amounts are rounded to tens of crowns.

Statistical Annex

Chart 7: Seasonality of new mortgage loans

Source: CBA Hypomonitor

Note: These are actually new mortgages (i.e. excluding refinancing and increases). The underlying data is available in the xls file attached on the CBA Hypomonitor website. The outlook to the end of the year (fcst) is a snapshot - based on the current trend, not a model prediction. However, for the rest of the year it assumes a 7% correction to the number of mortgages.

Chart 8: Distribution of new mortgage loans by purpose

Source: CBA

Note: The last figure represents the average for the last 12 months.

Mortgage market to deliver strong volume growth of 41% in 2025 and nearly a quarter in numbers

In the full year 2025, banks and building societies provided new mortgage loans worth CZK 321 billion. This is CZK 93 billion more than the CZK 228 billion created in 2024. This year-on-year jump corresponds to a 41% increase. On top of that, mortgages were refinanced to the extent of CZK 85 billion, bringing the total mortgage market to CZK 406 billion in 2025 from CZK 275 billion in 2024. If we adjust the volumes for the increase in house prices of around 15-16% (according to various statistics), the volume of new mortgages grew slightly less in real terms. This corresponds to a more moderate increase in the number of new mortgages in 2025, by less than a quarter to more than 76.11 thousand, and a nearly 15% increase in the average amount of a new mortgage granted to CZK 4.21 million.

New mortgages were financed at an average rate of 4.58% in 2025, half a percentage point lower than in 2024, with the spread to the market swap rate curve less than one percentage point, slightly below the long-term average. The average monthly mortgage payment in 2025 was just under CZK 22,800, up 8.6% from 2024, and slightly above the likely more than 7% increase in average nominal wages last year. The average year-on-year increase in the monthly mortgage payment of approximately CZK 1,800 in 2025 mainly reflected a higher average mortgage level with an increase in the payment of almost CZK 2.9k. CZK, while the lower mortgage interest rate reduced the average monthly payment by more than CZK 1.2 thousand. CZK.

Chart 9: Annual volume, number and average amount of mortgages granted between 2020 and 2025

Source: CBA Hypomonitor

CBA publishes summary statistics for the entire banking market

The Czech Banking Association, in cooperation with its member banks, publishes new aggregate statistics on the housing market. These are mainly the volumes and numbers of newly granted and refinanced mortgages and the respective interest rate. These statistics are published by the CBA in aggregate form for the entire banking sector on a regular basis around the middle of each month. All domestic banks and building societies providing mortgages in the Czech Republic participate in the survey. The data are available from January 2020 in the attached file on the website www.cbaonline.cz, where the relevant statistics can also be found separately for banks and building societies. The above figures are for the sector as a whole, which can also be viewed in a simple graphical form on the website www.cbamonitor.cz.

Methodology of the CBA Hypomonitor

The CBA Hypomonitor divides mortgage loans granted by banks and building societies to households into several categories in order to distinguish new loans from refinanced or internal refixations. New loans are then reported in categories according to the purpose of the loan:

1. new loans

These are loans whose full volume enters the economy for the first time. This category does not include loan consolidations or loan refinancing. It is divided into three categories:

- Purchase of real estate

- Property construction - including property renovation

- Other new arrangements - only new loans that are in no way related to the purchase or construction of the property, e.g. so-called American mortgages, settlement of a JVM, repayment of the purchase price, settlement of an inheritance share, settlement of a cooperative share, etc.

2. Refinanced loans from another financial institution

These are loans that have been originated by refinancing one or more loans from a financial institution other than the reporting one. Irrespective of the amount refinanced and regardless of the amount of any increase, the total amount of the newly originated loan is reported in this category.

3. Loans increased or internally refinanced

These are loans that were already part of the reporting entity's portfolio in the previous reporting period and have undergone one of the following changes during the reporting period:

- an increase in the agreed amount

- changes such that the original loan has been refinanced/converted into a new loan within the reporting entity. This is a genuinely new contract and not, for example, just a new arrangement in the context of a refixation of an existing contract. Therefore, the volume of such loans in the CBA statistics is lower than 'other new arrangements' in the Czech National Bank statistics.

The following banks and building societies provide data for the CBA Hypomonitor: Air Bank, Banka Creditas, Česká spořitelna, ČSOB, ČSOB Stavební spořitelna, Fio banka, Hypoteční banka, Komerční banka, mBank, Modrá pyramida, MONETA Money Bank, MONETA Stavební spořitelna, Oberbank, Partners Banka, Raiffeisen stavební spořitelna, Raiffeisenbank, Stavební spořitelna České spořitelna, UniCredit Bank.