The Czech economy slowed in Q1. Household purchasing power remains hopeful

GDP growth slowed to below 0.2 percent in the first quarter, a negative surprise. Instead of the expected household consumption, the economy was mainly driven by investment, while foreign trade worked against growth. However, the weaker consumption may be only a temporary correction after the strong end of last year. The same applies to industrial production, and the government's temporary budget provision also had a negative impact on the first quarter. The outlook will be significantly affected by the intensification of the commodity supply crisis due to the Iranian conflict.

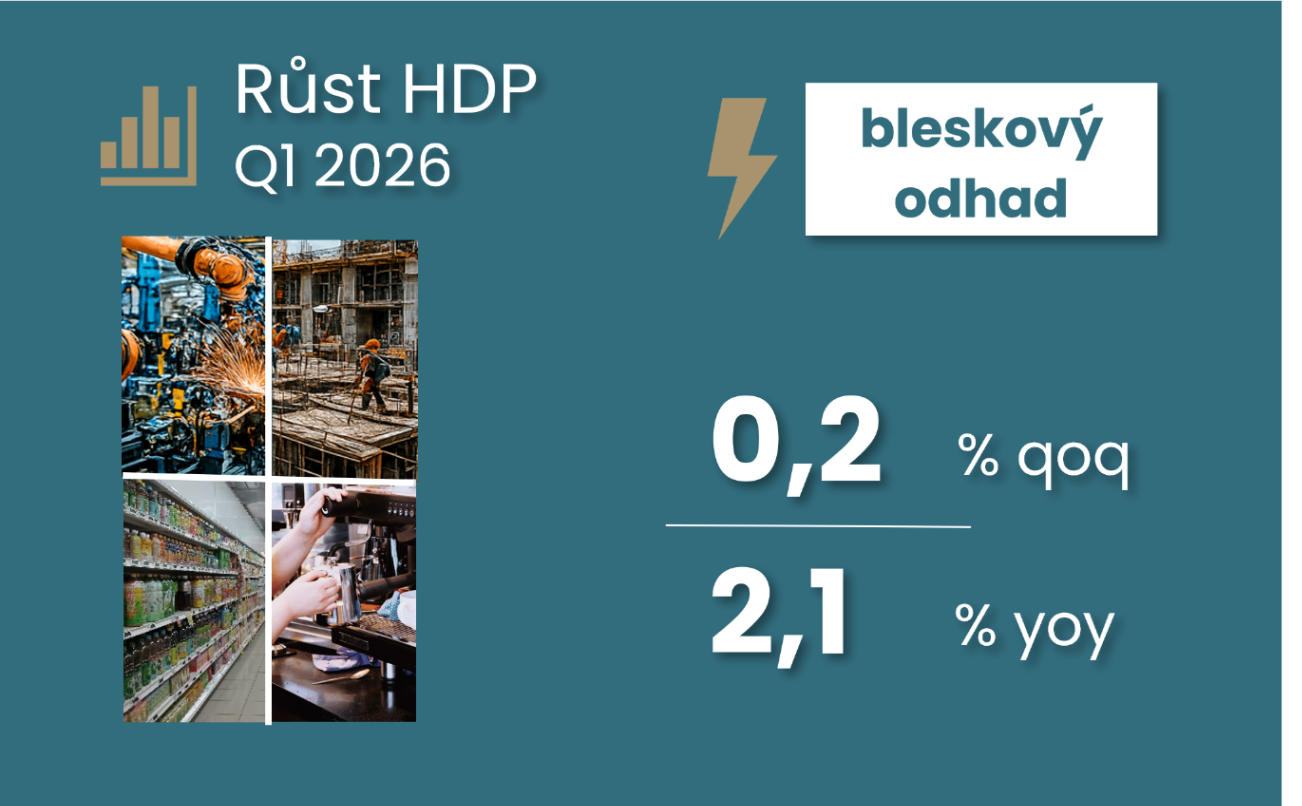

Growth in the Czech economy slowed to below 0.2 per cent in the first quarter compared with the previous quarter. This is a negative surprise after an average growth of 0.7% last year. Year-on-year GDP growth slowed to 2.1% in the first quarter of this year from 2.7% in the final quarter of last year, with the whole of last year showing +2.6%. The slower 0.2% quarter-on-quarter growth in the Czech economy slightly outpaced the slowdown in the eurozone to 0.1%, with German GDP growth accelerating slightly to 0.3%, but Italy and Spain slowing to 0.2% and 0.6% respectively, and France stagnating.

The actual structure of growth was also surprising. The Czech Statistical Office said that growth was mainly driven by investment (we do not yet know the role of inventories), while foreign trade contributed negatively, helped by strong domestic demand. Household consumption was expected to remain the main driver of quarter-on-quarter growth. This did not happen. Weaker signs were already seen in the February retail sales figures. We had expected household consumption to be able to offset the weaker industrial data.

The end of last year was very strong for households, with their consumption growing strongly by 1.2% quarter-on-quarter on a seasonally adjusted basis (up from an average of 0.8% last year). Thus, a partial correction of this strong growth is likely to have come in the first quarter. Meanwhile, consumer sentiment surveys remained solid in the first quarter and in April, even when it comes to large purchases. The purchasing power of Czech households is growing, which should support consumption. Moreover, their disposable income rose significantly at the end of last year. All the more surprising is the current cooling of consumption, where the Iranian conflict may have had a rather limited impact.

On the other hand, the labour market data cannot be ignored. Employment remained unchanged in the first quarter, slowing its year-on-year increase to 0.7%. We also observed a slight rise in unemployment, which reached 4.9% in the case of registered unemployment and 3.3% in the case of sample unemployment in Q1, 0.8 and 0.6 percentage points higher than a year ago, respectively. Households also reported a persistently abnormally high savings rate at the end of last year (19.7%). They have therefore remained cautious, which is unlikely to change significantly in the coming months or quarters given the current uncertainty.

The government's role is twofold. The budget provisionality has temporarily dampened government operating and investment spending, which has reduced the contribution of government consumption to GDP. We are likely to see a positive offset in the second quarter. A planned increase in government wages will also be added, which will again support purchasing power. But at the same time, the government helped contain consumer price increases at the beginning of the year by shifting the payment for renewable energy from household bills to the government budget, thereby partially supporting purchasing power. These two influences worked against each other.

The impact of the conflict in the Middle East will only become more pronounced in next quarter's results. If it is confirmed that weaker consumption was just a correction after a strong finish to last year and strengthens again in the second quarter, the Czech economy could grow by 2.3 per cent this year if the Iranian conflict calms down. However, if the energy shock hits household consumption harder (April consumer price growth is likely to get above 2.5% y/y depending on food prices), economic growth will be more around 2%. For companies, besides the energy shock, the key will be how the lack of energy in Asia will affect global demand and supply chains, and thus the export activity of Czech companies, which poses additional growth risks.

For the central bank, these numbers mean less concern about inflationary pressures from a growing economy. However, they are unlikely to have a direct impact on near-term decisions. The CNB is likely to maintain a cautious stance at its May meeting and wait for detailed June data on wages and unemployment.

GDP growth slowed to 0.2% q-o-q in the first quarter ...

... with unchanged employment

Monthly data for January and February did not suggest further acceleration ...

...because of the weaker industry...

...construction...

... net exports

... which was not compensated by sales in retail and services

Note: Unless otherwise stated, we work with seasonally adjusted figures in the text. Annualized developments show possible year-on-year growth in the annual outlook if current month-on-month momentum is maintained.