CBA Hypomonitor: the volume of new mortgages rose to CZK 321 billion last year. And is the second strongest in history

Table 1: Summary of mortgage origination volumes and average interest rates for December 2025

monthly values | values since the beginning of the year | ||||||

Volume | Number | Rate | Volume | Number | Rate | ||

Total | 37,1 | 8 715 | 4,48 | 406,4 | 100 066 | 4,57 | |

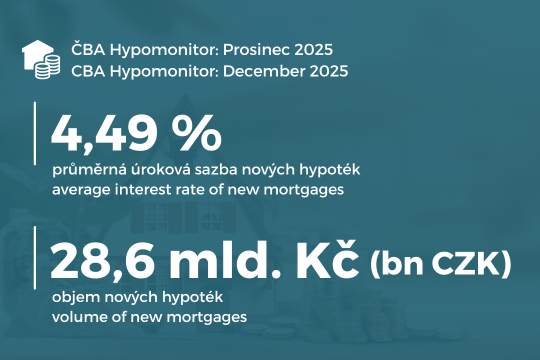

New loans | 28,6 | 6 366 | 4,49 | 321,4 | 76 117 | 4,57 | |

of which: | |||||||

for purchase | 23,0 | 5 088 | 4,49 | 257,4 | 59 888 | 4,57 | |

for construction | 3,3 | 756 | 4,43 | 45,8 | 11 199 | 4,54 | |

Other | 2,3 | 522 | 4,59 | 18,2 | 5 030 | 4,72 | |

Refinanced from another institution | 7,1 | 1 978 | 4,45 | 70,1 | 19 935 | 4,53 | |

Refinanced internally, increased | 1,3 | 371 | 4,44 | 14,9 | 4 014 | 4,54 | |

Source. | |||||||

"The end of December maintained a strong pace of nearly $30 billion in new mortgage originations despite Christmas.And while market interest rates eased the pressure on stable mortgage rates, the continued brisk pace of average mortgage rates is likely to keep the central bank on its toes, both in terms of interest rates and macro prudential measures," believes Jaromír Šindel, chief economist at the Czech Banking Association.

Mortgage market in 2025: further strong volume growth of 41% and almost a quarter in numbers

Chart 1: Annual volume, number and average amount of mortgages granted between 2020 and 2025

"The year 2025 became the second most successful year in terms of mortgage volume in the 30-year history of the mortgage market in the Czech Republic. Given the insufficient supply of flats and houses and their slow construction, the positive environment for economic growth, the unprecedented increase in real wages in recent years and the deferred demand for own housing, we expect this year's mortgage volume to grow by around 13% year-on-year to approximately CZK 432 billion.While the mortgage market is expected to grow in double digits, we expect the annual dynamics of property prices to slow down to higher single digits," says Martin Vašek, CEO and Chairman of the Board of Directors of ČSOB Hypoteční banka and ČSOB Stavební spořitelna.

December confirmed strong mortgage volumes at almost CZK 30 billion in the second half of the year

"Last year, we achieved our second consecutive best result ever in terms of the number and volume of new mortgages. This success confirms not only the gradual recovery in demand but also our strong market position. The stabilisation of interest rates has brought greater certainty to clients and supported their decision-making.Unless there is a significant negative shock in the form of higher market resources on the interbank market, we expect the positive trend to continue in 2026," expects Zdeňka Kovářová, Mortgage Manager, UniCredit Bank.

Chart 2: New mortgages granted without refinancing

InDecember 2025, banks and building societies have kept the volume of new mortgages close to CZK 30 billion

Source: CNB, CBA Hypomonitor (volumes before 2020 are from CNB statistics).

Source: CNB, CBA Hypomonitor (volumes before 2020 are from CNB statistics).

Chart 3: Average mortgage amount by purpose

The average size of a newly granted mortgage rose slightly to CZK 4.49 million in December.

Source: CBA Hypomonitor

Source: CBA Hypomonitor

The average mortgage rate rose marginally to 4.49% in December and market interest rates eased in December

Chart 4: Average mortgage interest rate - new business

Despite a slight increase in December, it remains well below last year's level of 4.8%.

Source: CNB, CBA Hypomonitor

Source: CNB, CBA Hypomonitor

Chart 5: The easing of December inflation and the cooling of the inflation outlook for 2026 have depressed market interest rates and thus upward pressure on mortgage rates

Source: LSEG, Macrobond (9 December 2025), CBA

Source: LSEG, Macrobond (9 December 2025), CBA

The average size of actual new mortgage originations was up from 4.49mn in December. CZK 4.5 million, it remains on an upward trajectory

Impact on the average monthly mortgage payment of around CZK 24.1 thousand in December

Table 2: Illustration of the average monthly mortgage payment by length of repayment and interest rate

Average size of a new mortgage in CZK: | 4 490 660 | ||||||

Average interest rate in %: | 2,0 | 3,0 | 4,0 | 4,49 | 5,0 | 6,0 | |

Monthly instalment: | |||||||

Mortgage maturity in years: | 15 | 28 900 | 31 010 | 33 220 | 34 340 | 35 510 | 37 890 |

20 | 22 720 | 24 910 | 27 210 | 28 390 | 29 640 | 32 170 | |

25 | 19 030 | 21 300 | 23 700 | 24 940 | 26 250 | 28 930 | |

26,8 | 18 080 | 20 360 | 22 810 | 24 060 | 25 400 | 28 130 | |

30 | 16 600 | 18 930 | 21 440 | 22 730 | 24 110 | 26 920 | |

Source: CBA [1] | |||||||

Note: the coloured column corresponds to the interest rate of the latest CBA Hypomonitor, other rates are illustrative; the coloured row corresponds to the average maturity of new mortgages according to CNB data; amounts are rounded to tens of crowns. | |||||||

Chart 5: Illustrative comparison of the average monthly mortgage payment with a year ago, depending on the interest rate, mortgage size and maturity in years

In a year-on-year comparison, the fall in the mortgage rate resulted in a saving of CZK 810 on the average monthly mortgage payment, but the increase in the average mortgage amount caused an increase of CZK 3 360.

Source. Note: Amounts are rounded to tens of crowns.

Chart 6: Seasonality of new mortgage loans

Source: CBA Hypomonitor

Note: These are actually new mortgages (i.e. excluding refinancing and increases). The underlying data is available in the xls file attached on the CBA Hypomonitor website. The outlook to the end of the year (fcst) is a snapshot - based on the current trend, not a model prediction.

Chart 7: Distribution of new mortgage loans by purpose

Source: CBA Hypomonitor

Note: The last figure represents the average for the last 12 months.

CBA publishes summary statistics for the entire banking market

- Purchase of real estate

- Property construction - including property renovation

- Other new arrangements - only new loans that are in no way related to the purchase or construction of the property, e.g. so-called American mortgages, settlement of a JVM, repayment of the purchase price, settlement of an inheritance share, settlement of a cooperative share, etc.

- an increase in the agreed amount

- changes such that the original loan has been refinanced/converted into a new loan within the reporting entity. This is a genuinely new contract and not, for example, just a new arrangement in the context of a refixation of an existing contract. Therefore, the volume of such loans in the CBA statistics is lower than 'other new arrangements' in the Czech National Bank statistics.