High savings, rising property prices and little relief for the CNB

The Czech household savings rate remained at 20% at the beginning of this year. It was thus slightly above last year’s average of 19.6% and still close to the 19.3% recorded during the Covid period. It remains well above the pre-Covid average of 11.9%. Fiscal policy has become less restrictive for disposable income, which in recent quarters had been driven mainly by strong wage growth (see the second and third charts below in the section on the savings rate and household income). The Czech household savings rate also remains high in international comparison, especially relative to Poland and Slovakia.

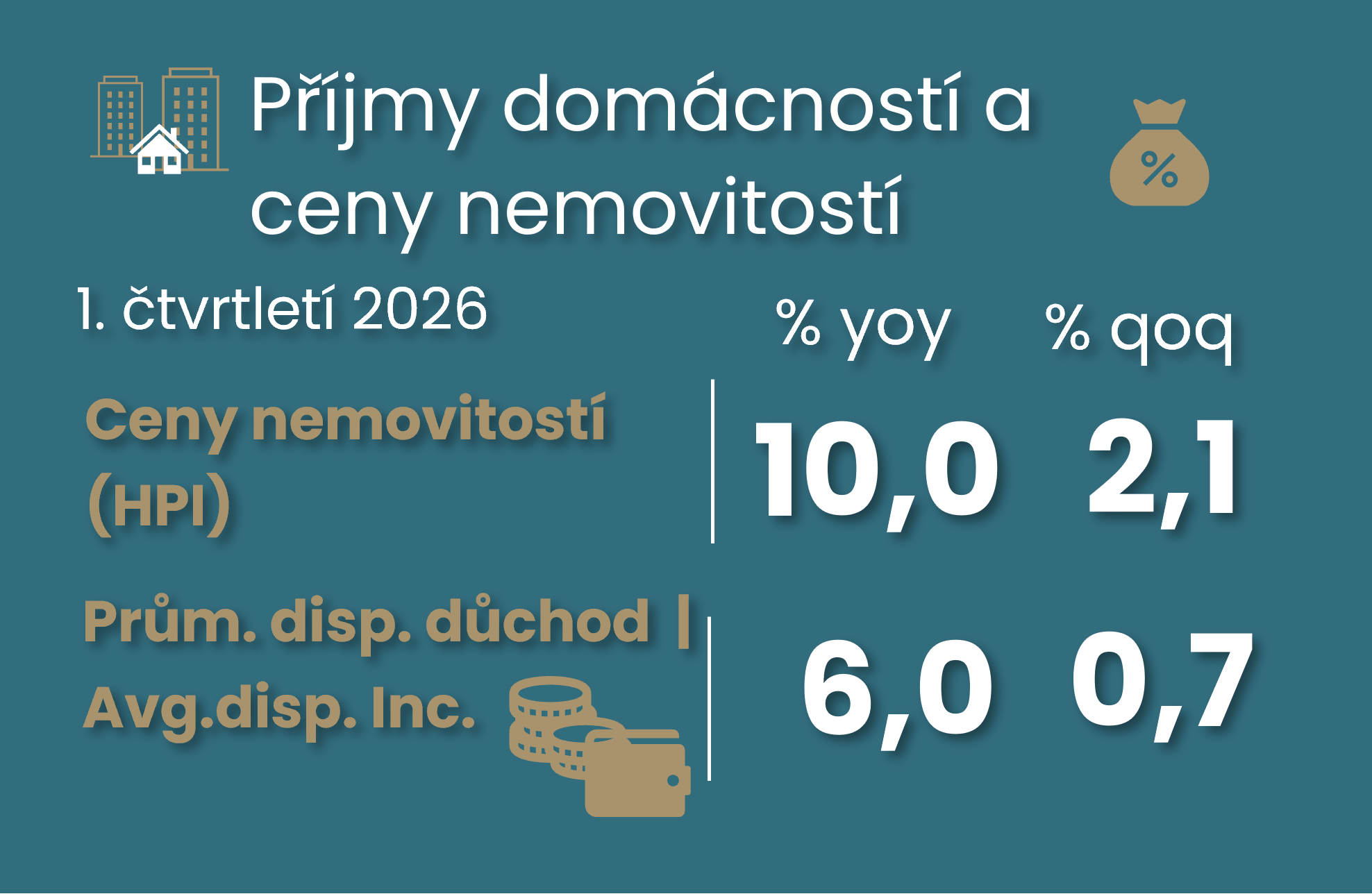

Property prices, including land as measured by the HPI index, continued to rise strongly at the beginning of this year, increasing by 2.1% quarter on quarter. Although this was slightly slower than last year’s average quarterly growth of 2.5%, property prices once again outpaced disposable income, whose growth slowed back to a weaker 0.7% quarter on quarter. By segment, meaning new and existing properties, the property price data did not bring any major surprise.

Annual property price growth is therefore still hovering around 10%, but the quarterly momentum may point to a slowdown towards 8% over a one-year horizon. This reflects slower disposable income growth, stricter CNB criteria for so-called investment mortgages, and higher mortgage interest rates resulting from tighter CNB monetary policy and persistent inflationary pressures. However, the supply side will limit this price slowdown, given higher construction material prices, only a weak recovery in building permits and labour shortages, although the number of housing starts has surprised me positively this year (see Chart 7 here).

The GDP growth revision brought more moderate household consumption growth and again highlighted distortions in employment data. GDP growth slowed to 0.2% quarter on quarter and 2.2% year on year in the first quarter. At first glance, this figure remained unchanged compared with the data released at the end of May.

Behind the unchanged GDP growth figures, however, there is slightly weaker household consumption and a mildly negative revision to the still strong dynamics of foreign trade. By contrast, government consumption and fixed investment are slightly stronger, and the same applies to value added in industry. In more detail:

Household consumption was slightly weaker, by 0.4 percentage points compared with the original estimate, but its annual growth remained solid at 3.3% year on year in the first quarter. Its quarter-on-quarter growth slowed to 0.3% from 1.2% at the end of last year. I would, however, attribute this mainly to the alignment of the new quarterly figures with the annual data for 2025, when average quarter-on-quarter household consumption growth reached 0.8%.

This was offset by a slightly higher level of government consumption, up by 0.2 percentage points, although government consumption has broadly stagnated over the past two quarters and slowed to 1.4% year on year in Q1 2026.

While the level of fixed investment remained unchanged at the beginning of this year, its level in 2025 was revised higher and still showed 6% annual growth.

Exports and imports were revised slightly lower, by 0.7 and 0.9 percentage points, respectively. This does not change the fact that they still recorded strong year-on-year growth of 5.3% and 7.9% in the first quarter.

And what about hourly productivity? The previously reported persistent stagnation, with productivity remaining 1–2% below the pre-Covid level, no longer holds. However, the first quarter of this year was again weaker. The Czech Statistical Office revised value added in industry almost 2 percentage points higher, and in manufacturing by as much as 3.6%, with much of this revision reflecting an improvement already during 2024. Nevertheless, value added in industry still declined by 0.7% quarter on quarter in the first quarter. A similar improvement, by 1.4 percentage points, is also visible in the level of value added in financial services, although the stronger revision there had already taken place in 2025. By contrast, construction and agriculture reported a lower level of value added.

However, my interpretation of the new Czech Statistical Office data, especially for the first quarter, is significantly affected by the alignment of quarterly figures with the new annual data for 2025. The next quarterly release may therefore also revise the story for the first quarter. The CNB will also have to wait for this, namely for the new GDP details to be published on 28 August. The central bank is likely to face persistently stronger core inflation dynamics, but lower oil prices and another decline in Polish inflation, probably linked to weaker food price pressures, should also bring relief to Czech headline consumer inflation.

House prices

The first quarter of 2026 did not bring a closing of the gap between property prices and household income …

… despite, or partly because of, only a mild slowdown in property price growth

… especially from a long-term perspective

Although acquisition costs are still rising more slowly than property prices, their acceleration to 1.5% quarter on quarter limits the scope for a more pronounced slowdown in property price growth

Property prices including land slowed mainly for existing properties, probably due to a smaller jump in land prices

Overview of property prices from the Czech Statistical Office – more detail in CBA Monitor

Households' saving rate and income

The Czech household savings rate remained at 20% at the beginning of this year

The Czech household savings rate remains high also in international comparison, especially relative to Poland and Slovakia

Disposable income has been driven in recent quarters by strong wage growth

Fiscal policy has become less restrictive for disposable income …

… although this does not fully apply to social transfers in kind, i.e. individual services provided to households by the government sector

Higher CNB's interest rate will also contribute to stabilising households’ property income

GDP revision

GDP growth is supported by solid consumption, strong fixed investment and exports, but strong domestic demand is also pulling in stronger imports

The revision showing slower wage growth, stronger value added and higher productivity brought more moderate growth in unit labour costs, but not enough to trigger a dovish turn at the CNB

Hourly productivity strengthened particularly in 2025, but the first quarter brought another decline; we will see whether the second-quarter figures change this picture

The story of more moderate unit labour costs, however, does not change the story of higher prices of core services in CPI

Growth in unit labour costs in services is not only about the real estate sector, but also about professional services, while finance and ICT are dampening these pressures

The wage recovery is apparent across the economy, except for public services …

… which, however, does not hold for labour productivity