October consumer inflation at 2.5% and continued rise in unemployment keep CNB on tenterhooks

Comment by Jaromír Šindel, Chief Economist of the CBA: October consumer inflation not only confirmed a more pronounced shock from higher food prices, but also showed higher prices of transport services and prices of means of transport as part of core inflation. In the longer term, it is worth noting that imputed rental prices have already caught up with the previous inflation shock, and the same has been true for a few months for holiday prices. Thus, the higher October inflation and unemployment data will not help the central bank or the market resolve its dilemma of the next interest rate move.

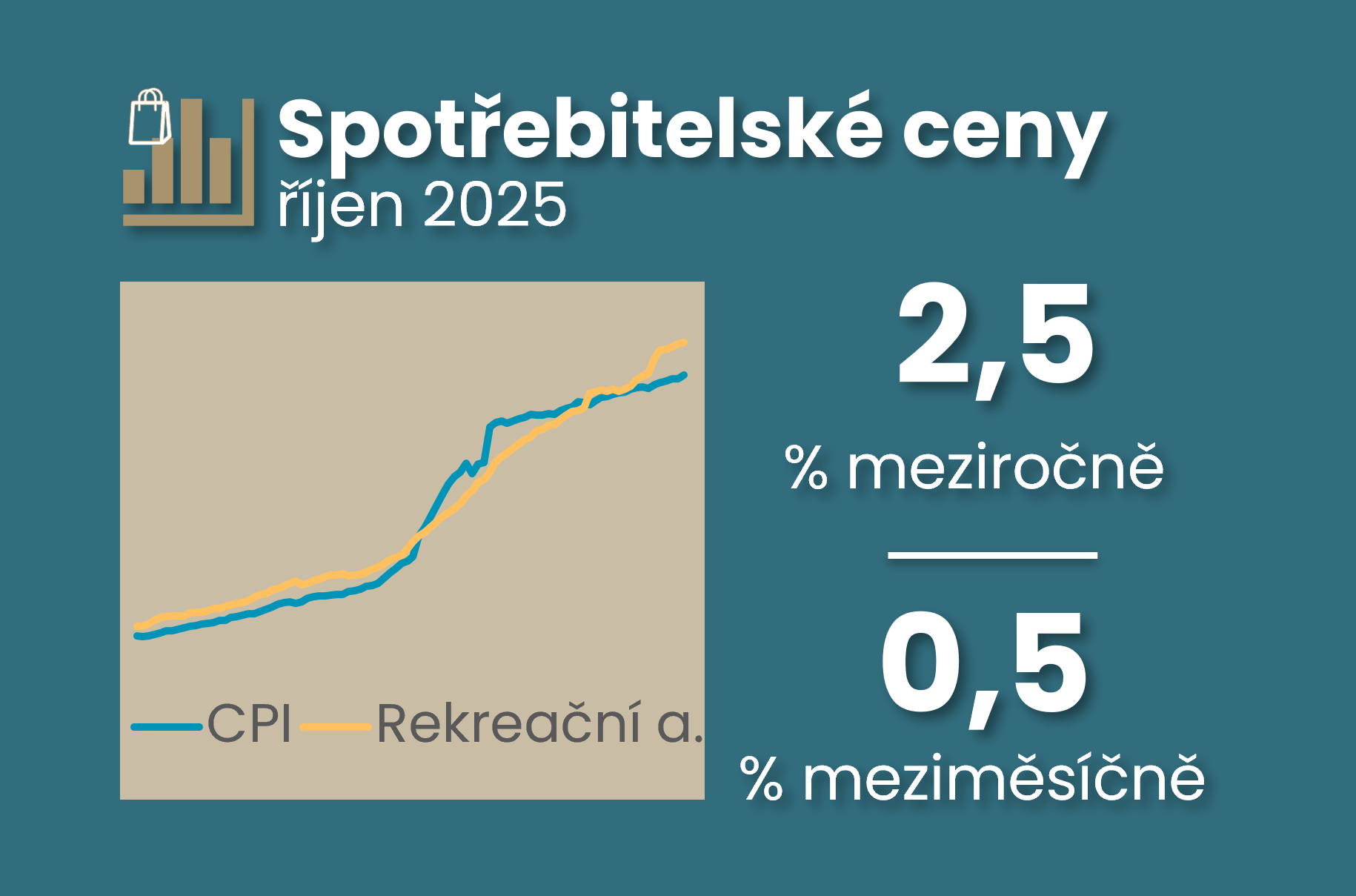

The final estimate of October consumerpriceinflationremained at 2.5% yoy, which was higher than expected (consensus 2.3% and CNB 2.2%). My estimate of core inflation moved slightly above 2.8%, which would imply a month-on-month (seasonally adjusted) growth of just under 0.3%. This is therefore above the CNB's target, although year-on-year growth looks in line with the CNB's Q4 forecast. However, let's wait for the CNB's actual estimate of core inflation growth at 13:00. So for now, I do not change my outlook for core inflation momentum for the coming spring, i.e. slightly above the CNB's target. This should be neutral for the CNB's monetary policy.

Seasonally adjusted headline inflation rose 0.5% m-o-m in October, 0.3% points above the pace in the previous three months. The key drivers of this change came from the food segment, but higher prices for autos and transportation services also added to the mix.

October's registered unemployment rate added to the upward momentum, also due to graduates and the young, to reach 4.7% on a seasonally adjusted basis, something we haven't seen since February 2017. Unemployment was at just under 4.6% last month, above 4% at the start of the year and slightly below 4% a year ago. With employment unchanged in the third quarter, we are seeing a continued structural change, with workers leaving (presumably from industry) not finding employment in a labour market that is looking for other workers (construction and services). Although the higher October unemployment rate is contrary to expectations from the confidence surveys, these were positively influenced by better household expectations in October, which was not shared by employers (see last chart). Thus, rising unemployment is likely already biting into household demand, as seen in recent retail and service sales.

Graphs on inflation (unemployment is below)