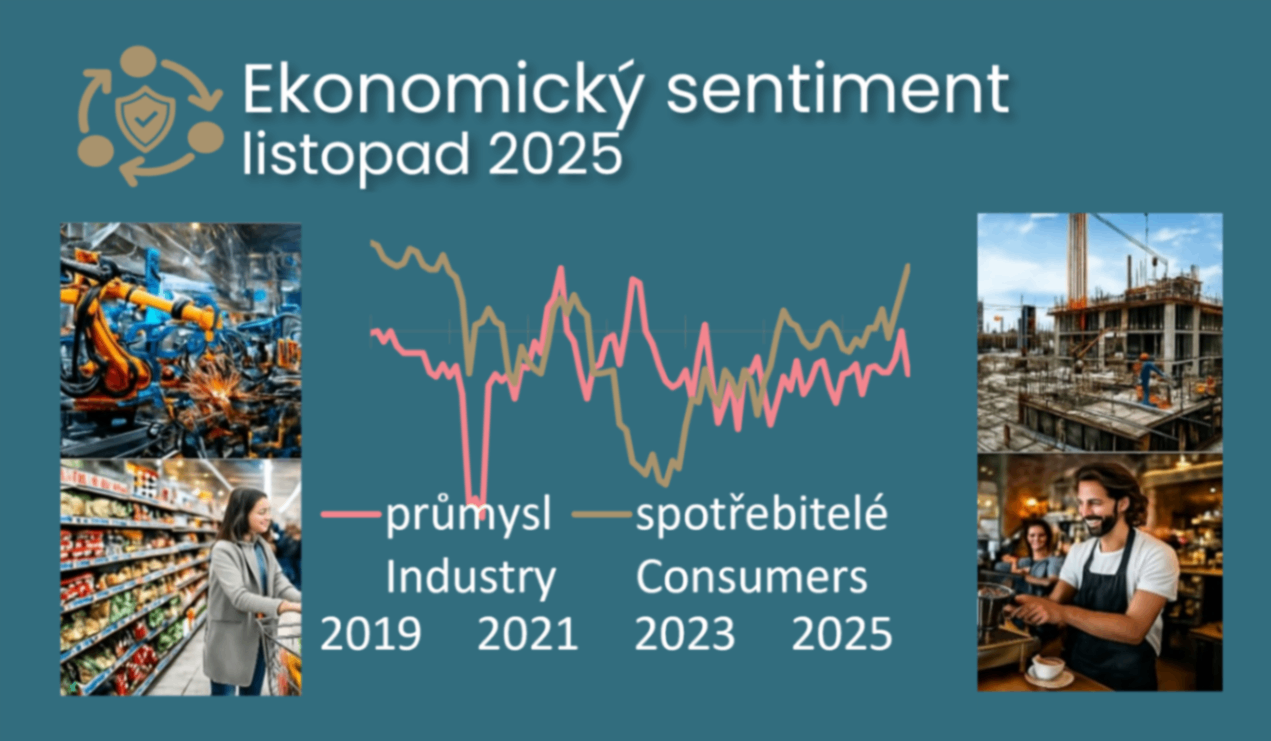

November sentiment slightly worse on average, but with significant movements in detail

Comment by Jaromír Šindel, Chief Economist of the CBA: November's confidence in the Czech economy weakened slightly, but still suggests continued growth. However, there are significant differences across sectors, reflecting the looming change in economic policy after the elections. Households remain visibly more optimistic, thanks to rapidly rising wages and perhaps in response to the new government's plans, while industry is returning to earlier weakness. Services are again reporting rising price expectations, keeping the central bank in hawkish mode.

November's confidence in the economy fell slightly, and although it still maintains the outlook for continued solid growth, there are significant movements in individual segments. These partly reflect the looming change in post-election economic policy, which, together with stronger wage growth, has contributed to more robust household confidence. This is reflected in more optimistic plans for larger purchases, which have so far only partly translated into improved trader sentiment.

The new "government" plans for administered prices and ETS2 are likely to have contributed to lower price expectations among households and in industry. However, rising price expectations in services, for the third month in a row, will leave the central bank in a hawkish frame of mind.

At the same time, the confidence survey is a reminder of the need for structural reforms as industrial confidence has returned to earlier weaker levels, although expectations for output and exports - with a dim view - remain on a weak uptrend along with slowly improving expectations for industrial employment.

The drop in construction employment expectations comes as a surprise, which likely reflects the impact of weak building permits and may be amplified by the currently uncertain funding of government infrastructure projects for next year.

Only a slight deterioration in November confidence ...

... but with significant movements across sectors - with, for example, stronger consumer plans...

... but with the downturn in the industry...

... which is not yet reflected in improving employment expectations in industry, but we are seeing a fall in expectations in construction

Price expectations in services have risen for three months in a row ...

... which contrasts with the decline in industry and households